Download presentation

Presentation is loading. Please wait.

1

Dr. L. H. Li Associate Professor Dept. of Real Estate &Construction,HKU Real Estate Economics(RECO6011) e-mail : lhli@hkucc.hku.hklhli@hkucc.hku.hk Web site : www.lilinghin.com Tel : 2859-2128 (Dept. of Real Estate & Construction)

Web site : Tel : (Dept. of Real Estate & Construction).")

2

Please Switch Off Your Mobile Phone, I Have Had Enough Brain Damage From the of My Own Cell Phone !

3

Real Estate Economics The purpose of this course is to provide students with a basic understanding of the economics of real estate and urban land development. This module is NOT ABOUT MICRO/MACRO economics. The programme is conducted over different sections of lectures and tutorials. The following gives a general outline of the course for reference only and is not designed to be a definitive course guide. The key reading list is also by no means exhaustive and students are expected and strongly encouraged to browse through the library before lecture.

4

To save a few trees for the monkeys, students are required to download supplementary (to required readings) lectures notes (from www.lilinghin.com click on various REE notes under “Information on MSc lectures” to download. If you have problems in doing so, please let me know.

5

PROGRAM OUTLINE Section 1 : Real Estate Market and Cycles It will start with introductory discussion on the market structure for real estate economy, followed by an examination of the formation of real estate cycles in general and in Hong Kong.

6

Section 2 : Real Estate Appraisal This section intends to cover the basic techniques of real estate investment and development appraisal. It will therefore start with introductory AND VERY BRIEF discussion on various types of simple traditional appraisal models and theory of land value (some of which have been covered in the Real Estate and Investment module).

..")

7

Section 4 : Risk Analysis in Real Estate Investment Having covered the applicability of various appraisal theories, the next question is naturally - So What ? If we assess the value for a particular asset, does that mean we will go ahead with the investment ? How do we know our decision is right ? How would the variables in the appraisal change ? How can computer help ?

8

Section 5 : The Economics of Urban Land Policy This will examine the impact of urban land policy in different environments. The lecture discusses the role of urban land policy. Moreover, socio-economic impact of urban land (political) decisions will be examined in the context of Hong Kong such as the role of government in the market.

decisions will be examined in the context of Hong Kong such as the role of government in the market..")

9

Real Estate Market Structure Market Structures in Real Estate and Construction Perfect competition or monopoly ? Characteristics of perfect competition Large numbers of players ? Homogenous products ? Free entry and exit ? Perfect information ? Number of Customers Identical factor prices ?

10

Real Estate Cycle – A theoretical Framework Property cycle can be defined as “… current but irregular fluctuations on the rate of all-property total return, which are also apparent in many other indicators of property activity, but with varying leads and lags against the all- property cycle” (Key, et al, 1994)

")

11

Real Estate Cycle – A theoretical Framework Do real estate cycles really exist ? degree of volatility of return Wheaton (1987) applies econometric model using real rents, level of office employment, expectations about future space needs(proxied by the ratio of current and previous period’s office employment), and area of occupied office space as determinants of demand. He finds that rents do not move quickly to clear market leading to extended length of cycles, and Supply reacts more to vacancies and rents than does demand, thus causing instabilities. What other causes ?

applies econometric model using real rents, level of office employment, expectations about future space needs(proxied by the ratio of current and previous period’s office employment), and area of occupied office space as determinants of demand. He finds that rents do not move quickly to clear market leading to extended length of cycles, and Supply reacts more to vacancies and rents than does demand, thus causing instabilities. What other causes .")

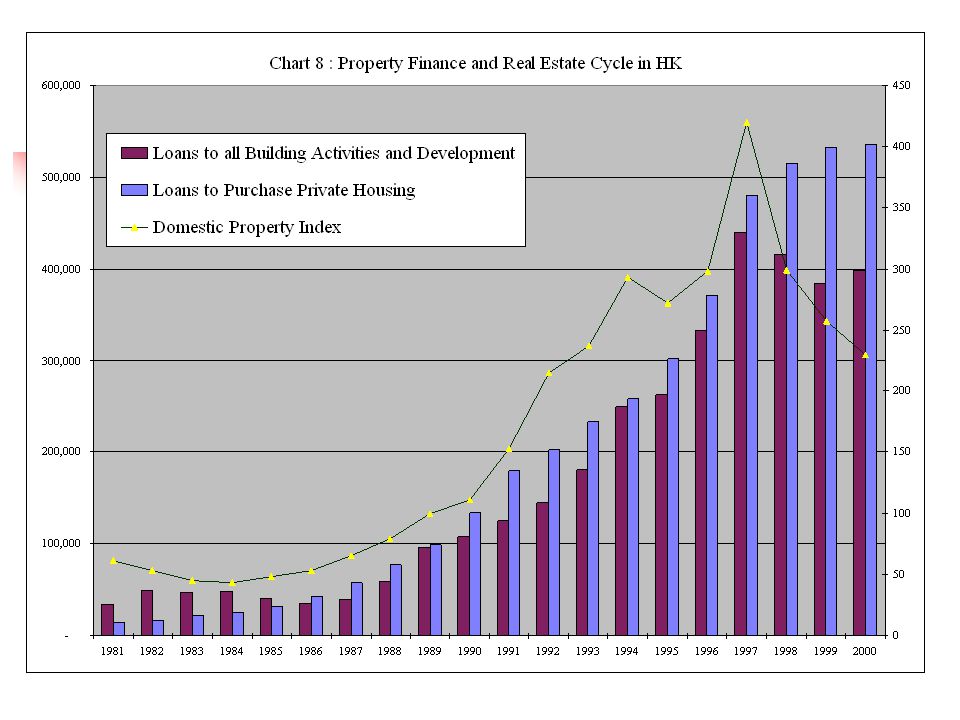

12

Factors causing fluctuations : mis-match between the demand and supply factors, the lags between the planning and production of space – Role of market data in minimizing these gaps Monetary and taxation deregulation led to price inflation intensified competition in the financial sector led to excessive loans on sometimes unjustified projects Easier capital flows and property finance offers a wide range of debt and equity finance opportunities, for good and bad projects internationalization of the world’s financial sector leading to new specification for commercial real estate and obsolescence of traditional supply

13

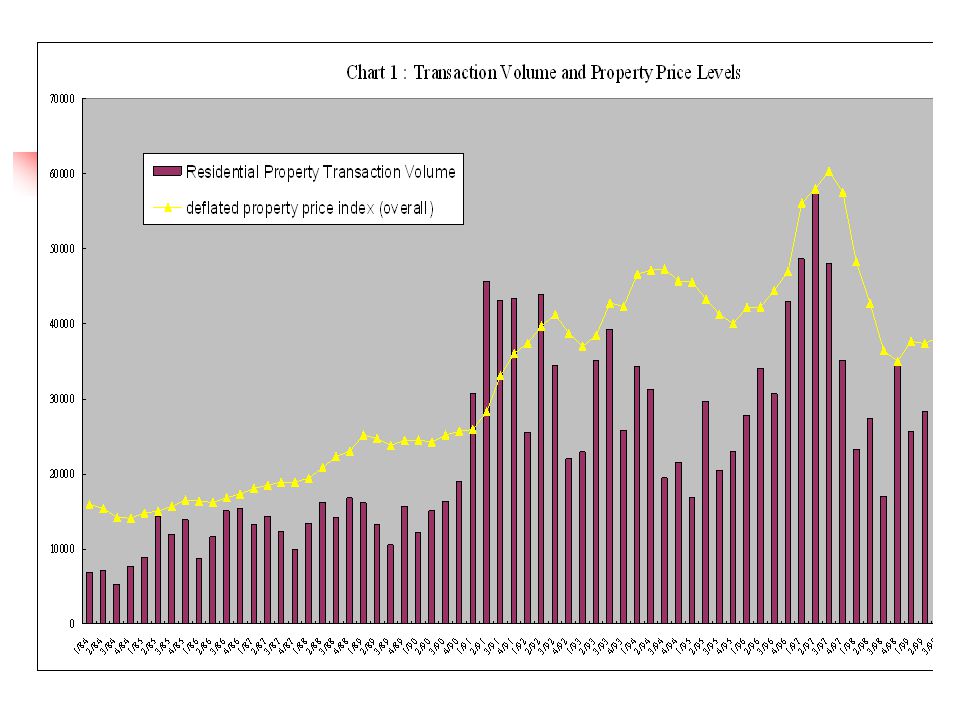

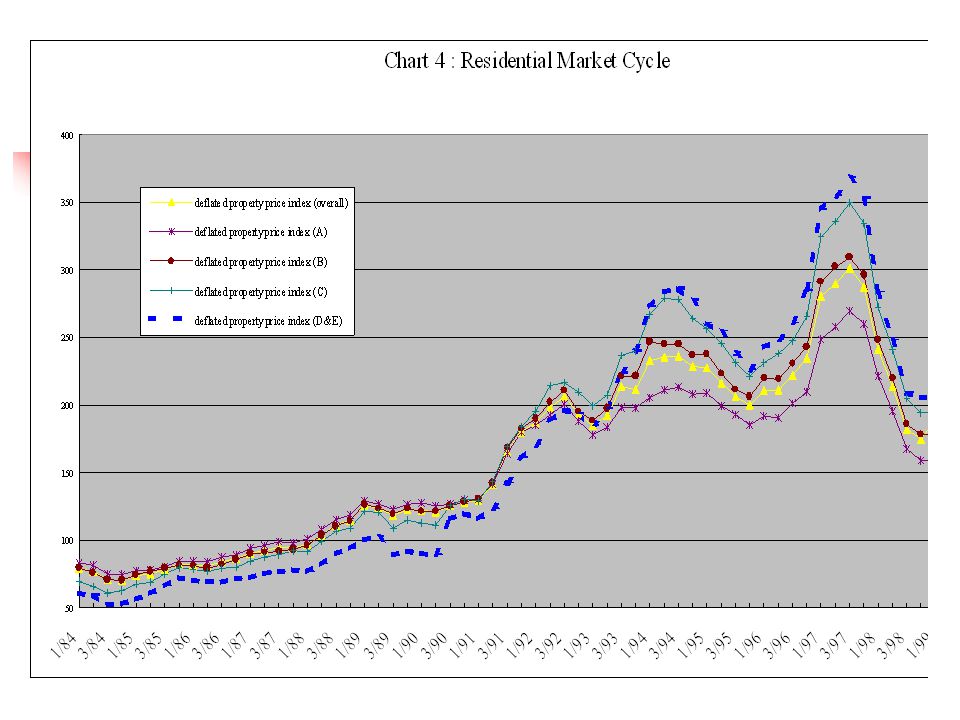

Real Estate Cycles in Hong Kong Long upward trend since 1984 with only minor adjustments in 1989 and in 1992, until 1997. Since 1992, relative cyclical movements were becoming more obvious, but new peaks normally climbed to higher levels as compared to the last peak. This pattern continued until after the Asian financial crisis in 1997 when prices bottomed down to the 1992 level

15

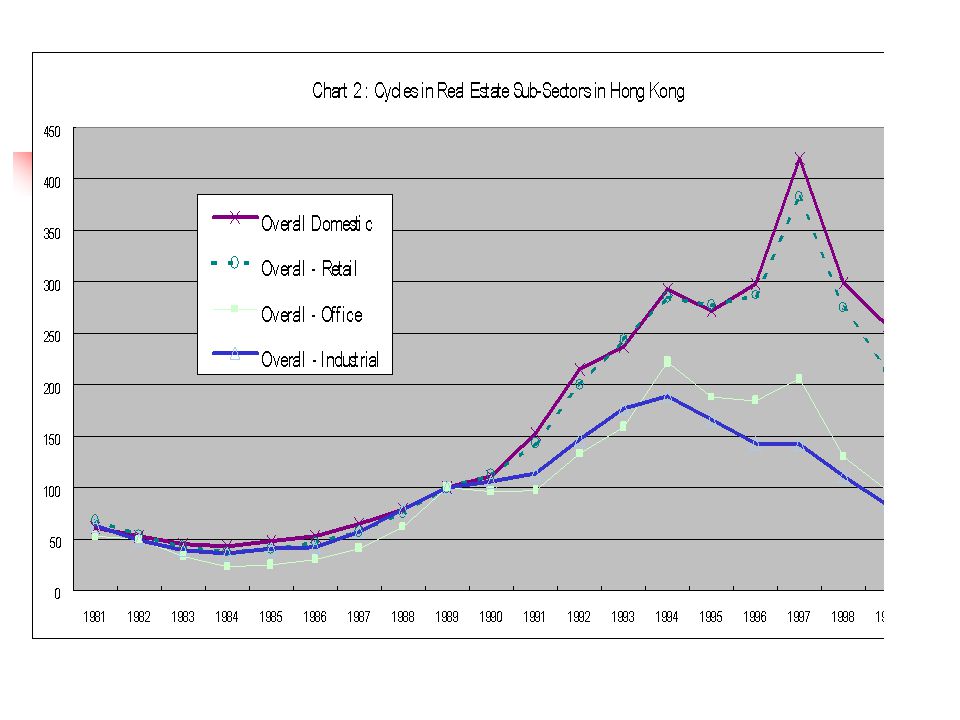

Real Estate Cycles in different sectors in Hong Kong Demand for residential units had remained fairly steady before 1997 due to various reasons. On the other hand, different sectors performed differently

17

Real Estate Cycles in Hong Kong – political influences the smaller residential flats out- performed the luxurious class from 1984 to 1992, then the reverse happened. Due to some political reasons, supply in various domestic sub-sectors has been distorted.

19

Real Estate Cycles in Hong Kong The fact that more sites available for small unit projects were put to the market was not a strategy, but incidental to some political developments after the Sino-British Joint Declaration in 1984 Hence, supply of properties from the government land market had been highly unstable

20

Table 2 - Major Land Disposal Pattern (Urban Area) 1985-1997 YearUrban Area CC/RR1R2R3R4ICP 1985-86 3231 2 1986-78 11 4 4 1987-8812 31 2 1988-894112 3 1989-9041 1 1 1990-91311 1 1991-9212162 1 1992-931312 1 1993-942 2 1994-952 42 1 1995-9623111 1996-97221 21 Total2229122671142 Source : Data compiled from Government Land Sales Record, Lands Department, Hong Kong Government. Note : R1 to R4 residenti al land for different degrees of development intensity. R1 is the most intensive type and so on. C -commercial land C/R - residential land with commercial elements allowed I - industrial land CP - land for car- parking use

21

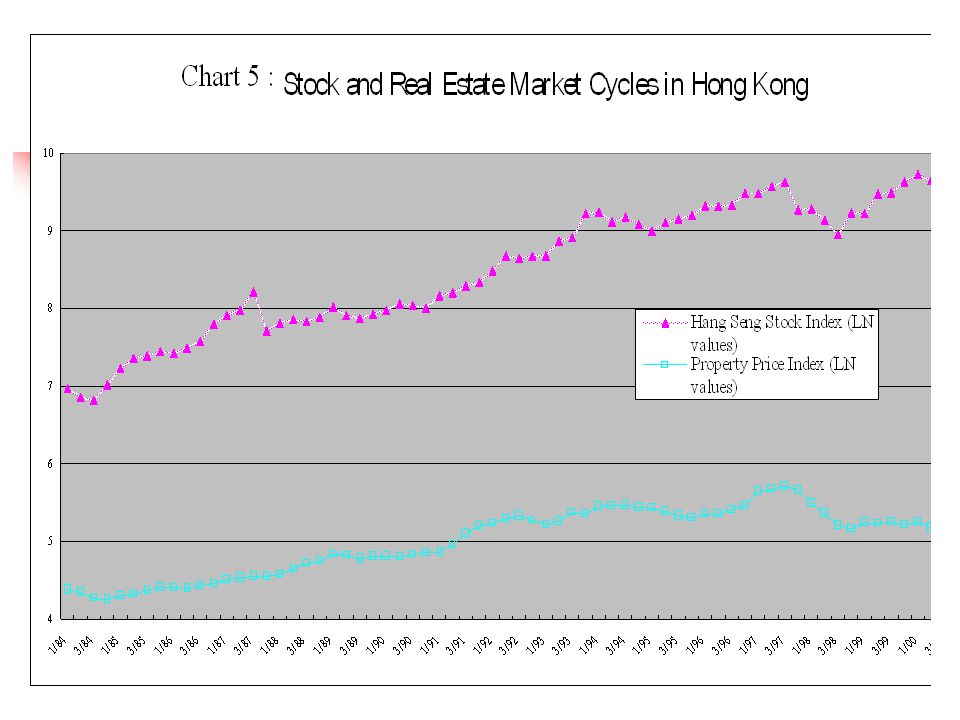

Real Estate Cycles in Hong Kong – correlation with stock market Real estate market had been highly correlated to that of the stock market only before the burst in 1997. limited and inactive bond market and there is a lack of other investment vehicles. Most of the blue-chip companies listed in the Hong Kong Stock Exchange are either property developers or property-related conglomerates.

23

Real Estate Cycles in Hong Kong – interest rate Interest rate in Hong Kong has been set to follow the tend of the US pattern, leading to the role of interest rate in the monetary policy in Hong Kong being relatively inactive. The HK interest rate, on which the mortgage rate bases, cannot always reflect the actual macro economic situation. As a good inflation-hedge tool, demand for real estate will soar under an artificially-low interest rate period leading to rising prices

24

Real Estate Cycles in Hong Kong – government policy New Government New Policy: In October 1997, the Chief Executive mentioned nothing except a promise to achieve a supply of 85,000 units of housing flats and a target of home ownership increased to 70% in the long run. This promise represents a substantial increase in housing supply in Hong Kong given the previous total supply of housing flats from 1992-1997

25

Housing Supply Pattern 1985-2000 in Hong Kong (*Note : Figure for year 2000 accounts for statistics up to the third quarter of the year ) Public RentalPublic SalePrivate TOTAL 198529598202063461384417 19862843264803301367925 19872497689743362967579 19883170188023012270625 198946393187763062195790 199032885175183148381886 199125486167264072882940 19921103957402568342462 199334295331092685494258 19941709845943435056042 199517349166722075354774 199618358107251718346266 199716046215351588653467 199814123210931948954705 199929382224933150483379 2000*18784160641659751445

Public RentalPublic SalePrivate TOTAL *")

26

Can the Gov’t dictate supply ? The new “socialist” style of land management system in Hong Kong after 1997 with production indication might not be effectiveness as the government cannot control all supply channels of housing

27

Table 5 : Contribution of Housing Supply Via Government Land Auction Channel YearAnnual new completion of housing floor space (1,000 sq.m.) Floor area available for housing development via government land auctions (1,000 sq.m.) % of supply from auctioned land on total supply 19911831365.6420% 1992947316.6433.4% 19931514400.4726.5% 19941255222.1817.7% 19951089370.1634% 199676921928.5% Average :26.68% Source : L.H. Li, (1996), Development Appraisal of Land in Hong Kong, Hong Kong : Chinese University Press

, Development Appraisal of Land in Hong Kong, Hong Kong : Chinese University Press.")

28

Real Estate Cycles in Hong Kong This market expectation, when faced with a market failure, started to search for explanations in the government policies for the burst of the bubble. One of these being the over-production of government-subsidized housing, or the HOS, for sale in the market. Is it true ?

29

Real Estate Cycles in Hong Kong The Bank Sector – Eager to lend you an umbrella on a sunny day and ask for it back when it rains. Bank sector in Hong Kong has been under rather strict scrutiny by the quasi-central bank, the Hong Kong Monetary Authority(HKMA). There has never been a major deregulation as such.

. There has never been a major deregulation as such..")

30

Real Estate Cycles in Hong Kong Proportion of loans to property investment outweighed that to individual for purchasing private housing flats in the mid-80’s, but the situation got reversed since late 80’s until after the burst of bubble in 1997. Banks have been keen on trying channel their funds into mortgage loans, eg. Pushing down mortgage rates.

32

Real Estate Cycles in Hong Kong Banks are pushing too much finance opportunities in good market, and Setting too many barriers for bridging loans in bad times

Similar presentations

Dept. of Real Estate &Construction,HKU Real Estate Economics(RECO6011) e-mail :>")