Download presentation

Presentation is loading. Please wait.

1

Divestment, Remuneration and Corporate Governance in Mature Firms Michelle Haynes University of Warwick Steve Thompson University of Nottingham Mike Wright University of Nottingham

2

Previous Research on Determinants of Divestment Haynes et al (2000) –managerial equity ownership positively correlated with divestment Hoskisson et al (1994) –insider ownership negatively related to diversification & anticipate higher ownership will be associated with lower restructuring If downsizing is reversal of prior diversification, opportunities for divestment likely to be negatively correlated with prior insider ownership

–managerial equity ownership positively correlated with divestment Hoskisson et al (1994) –insider ownership negatively related to diversification & anticipate higher ownership will be associated with lower restructuring If downsizing is reversal of prior diversification, opportunities for divestment likely to be negatively correlated with prior insider ownership")

3

Managerial/Board Equity Ownership Empire building associated with low prior insider ownership Higher insider ownership, lower diversification Higher insider ownership and exogenous changes increase response H1a: divestment is positively related to the board’s equity holding

4

Executive remuneration Extensive literature shows link between size and remuneration –Suggests reluctance to downsize Reinforced by: –loss of prestige for reduced size –personal disutility from unpopular downsizing decisions –bonuses based on accounting profits that may fall following divestments Intervention by remuneration committee difficult

5

Executive Remuneration II Link remuneration directly to performance through stock options (Murphy, 1997) –Depending on parameters of options pricing model, value of stock options may be very sensitive to share price changes –Agency theory suggests stock options may be especially effective where direct equity holdings are low H1b: Downsizing positively related to extent of sensitivity of executive remuneration to share price

–Depending on parameters of options pricing model, value of stock options may be very sensitive to share price changes –Agency theory suggests stock options may be especially effective where direct equity holdings are low H1b: Downsizing positively related to extent of sensitivity of executive remuneration to share price")

6

Corporate Governance H2a: Divestment will be positively related to the presence of a non-managerial blockholder H2b: Divestment will be positively related to a greater presence of non-executive outside directors on the board. H2c: Divestment is positively related to a change in top management. H2d: Divestment will be positively associated with high leverage

7

Finance & Strategy H3: divestment will be negatively related to firm performance. H4a: divestment will be positively associated with relatively high levels of diversification H4b: divestment will be positively associated with firm size.

8

Finance & Strategy II H4c: divestment will be positively related to core concentration. H4d: divestment will be positively related to core market share. H4e: divestment will be positively related to the degree of vertical integration. H4f: divestment will be positively related to acquisition activity

9

Data I 158 UK firms randomly selected from 1985 FT500 excluding financials, foreign & trading companies –Final sample 118 1985 - 1993 Divestments –Parent-to-parent from Acquisitions Monthly & Financial Times –Divestment MBOs from Centre for MBO Research

10

Data II Proportion & Count data –Proportion = sales price of divested assets/market value of firm for previous year, summed over period –0.1% market value assumed for missing Firm performance, leverage, size, market share, concentration from Datastream Governance, management changes, vert integ, diversification from annual reports

11

Data III Executive Remuneration –Executive ordinary share holdings and stock options from Hemmington-Scott Corporate Register –proxy relative importance of share based compensation to executive –ratio of executive wealth measure to cash compensation –based on marginal increase in executive wealth arising from increase in stock options and share ownership –each tranche of options weighted by marginal sensitivity to changes in value of underlying ordinary shares –use cross-section data due to data limitations –CEO and All Executives separately

12

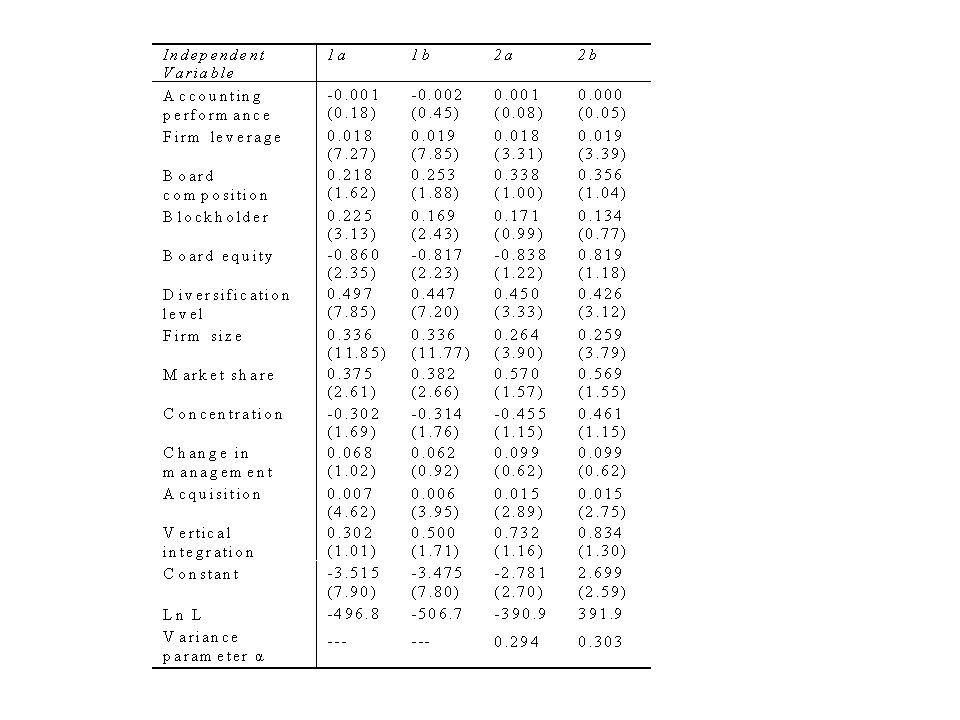

Table 1: Determinants of Divestment - Count Variable - Executive Remuneration (H1b)

")

14

Table 1: Determinants of Divestment - Count Variable - Other variables Start period variables –Strongly positive leverage (2d), diversification (4a), size (4b) –Less positive blockholder (2a), market share (4d) Intraperiod variables –Positive Acquisitions (4f) –Not robust/insignificant board equity (now negative) (H1a)

, diversification (4a), size (4b) –Less positive blockholder (2a), market share (4d) Intraperiod variables –Positive Acquisitions (4f) –Not robust/insignificant board equity (now negative) (H1a)")

16

Conclusions First test of importance of share-based incentives in motivating managers to divest Constructed share-based measures combining ownership & wealth effects of appreciation in executive options Data limitations means only approximation: –well-known valuation problems for ESOs –assume holds across period, may fluctuate Supports Murphy (1997) that share-based incentives needed to encourage such actions

that share-based incentives needed to encourage such actions")

Similar presentations

>")

FIN 200: Personal Finance Topic 17–Stock Analysis and Valuation Lawrence Schrenk, Instructor.>")