Download presentation

Presentation is loading. Please wait.

1

Performance Pay and Top-Management Incentives By: Michael Jensen, and Kevin Murphy

2

Purpose To estimate the magnitude of the incentives provided by each of the following mechanisms.

3

Incentive Generating Mechanisms Performance- based bonuses Performance- based salary revisions Stock Options Performance- based dismissal decisions

4

Agency Theory Suggests: Compensation policy should be designed to give the manager the incentives to select and implement actions that increase the shareholders wealth. *Paying CEO’s on basis of increased shareholder wealth is the objective of the owners.

5

CEO Compensation Deferred Compensation Stock Options Profit- Sharing Arrangements Stock Grants Savings plans Long-term performance plans Other fringe benefits

6

CEO cash compensation and firm performance as measured by a change in shareholder wealth. Δ(CEO salary+ bonus) t = a + b(Δshareholder wealth) t This equation assumes that current stock price performance affects current compensation. But that decision could be made before final earnings data is in. Equation (1)

t = a + b(Δshareholder wealth) t This equation assumes that current stock price performance affects current compensation. But that decision could be made before final earnings data is in. Equation (1).")

7

This equation assumes that current stock price performance affects current compensation. But that decision could be made before final earnings data is in.

8

Equation (2) Allows current pay revisions to be based on past as well as current performance. Δ(CEO salary+ bonus) t = a + b(Δshareholders wealth) t + b 2 (Δshareholders wealth) t-1 This regression may have better results than equation (1) but you can’t tell if it represents a real lag of rewards on performance and how much represents simple measuring errors caused by lags in reporting.

t = a + b(Δshareholders wealth) t + b 2 (Δshareholders wealth) t-1 This regression may have better results than equation (1) but you can’t tell if it represents a real lag of rewards on performance and how much represents simple measuring errors caused by lags in reporting..")

9

Equation (3) The relation between total compensation and firm performance based on the Forbes total compensation data, excluding both stock option grants and the gains from exercising stock options. The dependent variable in equation (3) represents the change in the current cash flows accruing to the CEO, the independent variables represent the discounted present value of the change in all future cash flows accruing to the shareholders.

represents the change in the current cash flows accruing to the CEO, the independent variables represent the discounted present value of the change in all future cash flows accruing to the shareholders..")

10

Equation (4) Assumptions Real interest rate = 3% CEO receives this increment until the age of 70. Changes in salary and bonuses are permanent Δ(CEO wealth) t = total pay + PV(Δsalary+bonus) t

t = total pay + PV(Δsalary+bonus) t.")

12

The Forbes definition of total pay excludes stock options although they clearly provide value increasing incentives for CEO’s The value of options held at the end of year Τ is calculated as… Black-Scholes 1973 Valuation Formula ΣNt * [S t e -dT Φ(Z t ) – P t e -rt Φ(Z t -δT ½ )] We assume that options are exercised at the highest stock price observed during the year. Incentives Generated by Stock Options

![The Forbes definition of total pay excludes stock options although they clearly provide value increasing incentives for CEO’s The value of options held at the end of year Τ is calculated as… Black-Scholes 1973 Valuation Formula ΣNt * [S t e -dT Φ(Z t ) – P t e -rt Φ(Z t -δT ½ )] We assume that options are exercised at the highest stock price observed during the year.](http://images.slideplayer.com/16/5117056/slides/slide_12.jpg "Incentives Generated by Stock Options.")

13

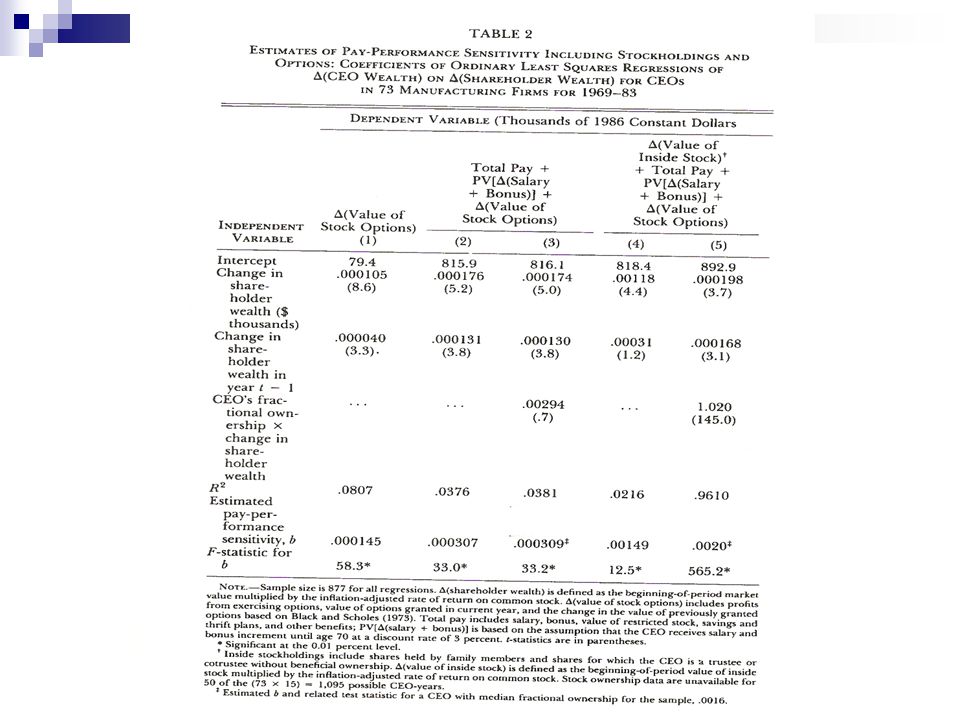

For a more complete measure of CEO wealth changes they used a proxy from Murphy’s 1985 sample of 73 Fortune 500 manufacturing firms during a 15 year period 1969-1983. Sample of 154 CEO’s

15

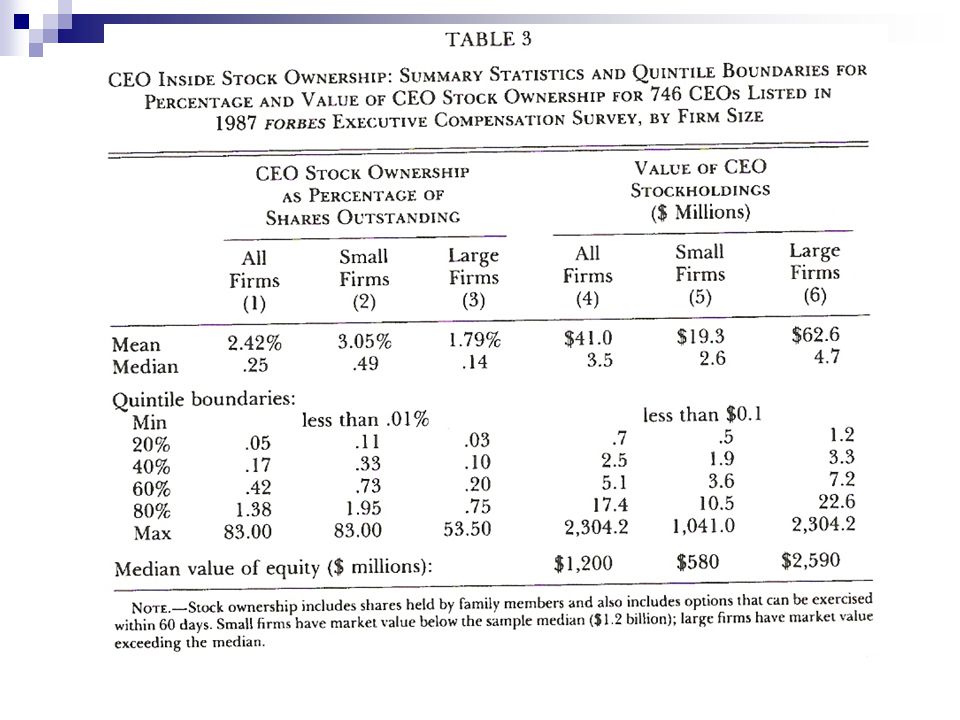

Table 3 Summarizes fractional stock ownership data for a much larger sample of CEOs. 746 CEOs in the Forbes 1987 Executive Compensation Survey held an average of 2.4% of firms common stock.

17

Incentives generated by threat of dismissal. The threat of dismissal for poor performance produces value-increasing incentives to the extent that managers are earning more than their opportunity cost.

18

ln(prob of TO/ 1-prob TO) = a+ b1(net market return)+b2 (lagged net market return) Net market return = fiscal year shareholders return- value weighted return of all NYSE firms Table 4

= a+ b1(net market return)+b2 (lagged net market return) Net market return = fiscal year shareholders return- value weighted return of all NYSE firms Table 4")

20

TABLE 5 Dismissal Probability is P= e x /(1=e x ) x= -2.08-.6363-.4181 CEOs are more likely to be fired at a younger age.

x= CEOs are more likely to be fired at a younger age.")

22

Conclusions The empirical relation between pay of top management & firm performance is positive and statistically significant, but is small for an occupation where incentive pay is expected to play an important role. The results are inconsistent with the implications of the formal agency models of optimal contracting.

23

Alternative Hypotheses 1. CEO may be an unimportant input in the production process. 2. CEO actions may be easily monitored and evaluated by the board of directors. 3. Political forces that implicitly regulate executive compensation by constraining the types of contracts that can be written between managers and shareholders 4. Equilibrium in the managerial labor market prohibits large penalties for poor performance and as result the dependence of pay on performance is decreased.

Similar presentations

Are CEOs Really Paid like Bureaucrats? n n To align the incentives of the CEO perfectly with that of the shareholders, pay the CEO.>")

F Hidden action (moral hazard)>")

, Shaun Bond (University of Cincinnati), & Joseph Ooi (National University of Singapore)>")

FIN 200: Personal Finance Topic 17–Stock Analysis and Valuation Lawrence Schrenk, Instructor.>")