Download presentation

Presentation is loading. Please wait.

1

Corporate Governance and Financial Distress: Evidence from Taiwan Tsun-Siou Lee and Yin-Hua Yeh 2002 NTU International Conference On Finance

2

Introduction Why do companies fall into financial distress or even bankruptcy? Can we develop an early warning system that is powerful in predicting corporate financial distress? Corporate governance has been regarded as one of the key factors that caused Asia financial crisis in 1997. Johnson, et al. (2000) further documented that corporate governance variables provide better explanatory power for the Crisis than macroeconomic variables.

further documented that corporate governance variables provide better explanatory power for the Crisis than macroeconomic variables..")

3

Ownership Structure around the World On the average, more than 60% of public traded companies around the world have an ultimate owner except in the US, UK and Japan. Taiwanese listed companies are characterized as mostly family controlled with a high degree of ownership concentration that is similar to the findings in the prior studies.

4

Incentive Effect Under Concentrated Ownership Under concentrated ownership environment, it is important to provide enough financial incentives for the controlling shareholder in order to reduce expropriation. Cash flow ownership of the controlling shareholder is an important source of such incentives. La Porta et al. (2002) also provided evidence supporting the positive incentive effect of cash flow ownership by a controlling shareholder on the valuation of firm

also provided evidence supporting the positive incentive effect of cash flow ownership by a controlling shareholder on the valuation of firm.")

5

Agency Problem Under Concentrated Ownership Under concentrated ownership, conflicts of interests arise between minority shareholders and the controlling shareholder. The larger the deviation between voting and cash flow rights, the stronger the ultimate owners’ motivation to expropriate minority interests.

6

Research Issue Although empirical results support that the threats of expropriation by the controlling shareholder tend to reduce corporate value, whether it will lead to a higher probability of financial distress remains an open question. Financial distress may lead to bankruptcy, liquidation or significant changes in control that may truncate the stream of expected rents from expropriation.

7

Research Issue Misconduct worsens the firms’ financial performance and hurt the firms’ competitiveness. In the wake of an economic recession or severe competition, these firms tend to become the victims of financial distress. Furthermore, the ultimate owner may use corporate funds for stock churning and fail to recover the funds after the stock market turns bearish. The firm in turn falls into liquidity difficulty followed by financial distress.

8

However, a controlling insider may desire to go on expropriating wealth for a very long time. For example, Claessens, et al. (1999) found that East Asian firms controlled by management/family groups were less likely to file for bankruptcy during the crisis. If so, expropriating insiders and weak governance should be associated with a smaller probability of financial distress. Therefore, we need to consider both the cost and benefit for the controlling shareholder to file financial distress in developing our empirical model.

found that East Asian firms controlled by management/family groups were less likely to file for bankruptcy during the crisis. If so, expropriating insiders and weak governance should be associated with a smaller probability of financial distress. Therefore, we need to consider both the cost and benefit for the controlling shareholder to file financial distress in developing our empirical model..")

9

The Measurement of Corporate Governance Following Claessens et al. (2002): the smaller the ratio of cash flow rights to control rights, the higher the tendency of the controlling shareholder to expropriate minority wealth. Following Yeh, Lee and Woidtke (2001) The higher the percentage of board seats occupied by controlling shareholder, the higher the tendency of the controlling shareholder to expropriate minority wealth.

: the smaller the ratio of cash flow rights to control rights, the higher the tendency of the controlling shareholder to expropriate minority wealth. Following Yeh, Lee and Woidtke (2001) The higher the percentage of board seats occupied by controlling shareholder, the higher the tendency of the controlling shareholder to expropriate minority wealth..")

10

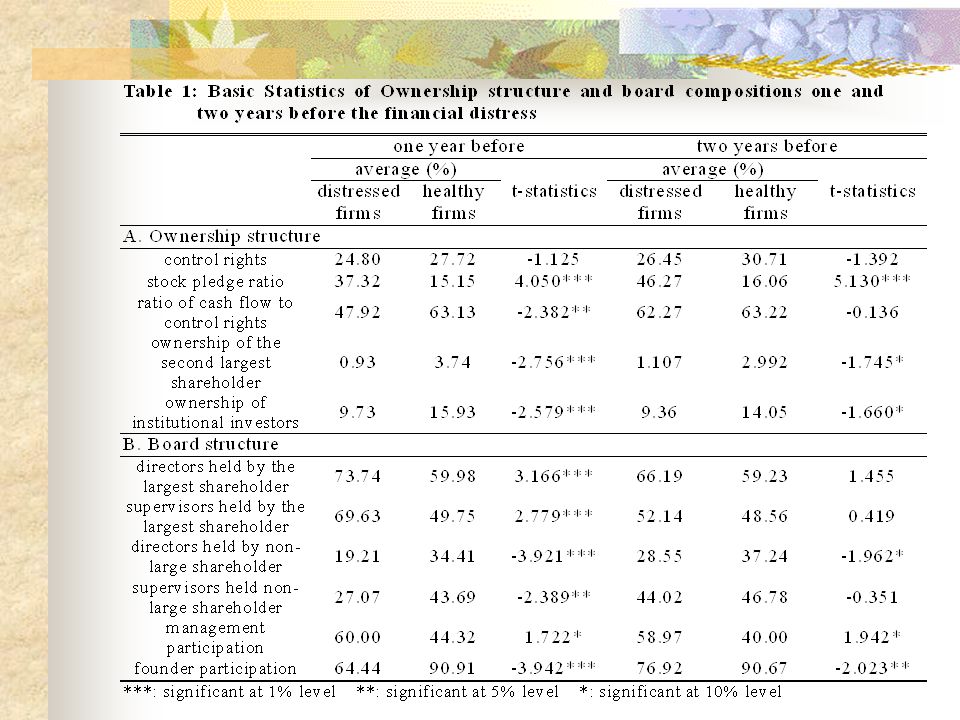

The Measurement of Corporate Governance We have seen more than thirty Taiwanese listed companies that experienced financial distress in 1998 and 1999. The controlling shareholders of these companies were accused of over-leveraging and over- investment in the stock market. It is reasonable to suspect more serious wealth expropriation to be associated with higher percentage of shares pledged for funds from financial institutions by the controlling shareholders.

11

Research Purposes We add to this literature by examining: the possible connection between prior corporate governance and financial distress through additional variables in previous studies, the board structure and stock pledge ratio of the controlling shareholder. the predictability of corporate governance models toward financial distress. the prediction power of corporate governance models among various sub-samples classified with financial performances.

12

Empirical Methodology We collect the data of Taiwan listed companies that encountered financial distress between January 1996 and December 1999, together with a matching sample consisting of non-distress companies. Definitions of financial distress samples Defaults on loan principal / interest payments, renegotiated loan terms Companies are traded at 100% margin We have 45 companies in our financial distress sample and 88 non-distress companies.

13

Logistic Regression The dependent variable takes the value of one if the company encountered financial distress, and zero otherwise. The controlling shareholders We traced the voting rights, cash flow rights and board seats occupied by the largest shareholder for each sample company according to the concept of ultimate control proposed by La Porta et al. (1999).

..")

14

The controlling shareholders In the majority of cases, the immediate shareholders of a corporation are themselves corporate entities, or investment companies and other legal entities. We then identify their owners, the owners of their owners, etc. We use the total ownership by each family group, defined as a group of people related through blood or marriage, as the unit of analysis.

15

X Family Firm A Firm B Firm C 30% 20% 12% 25% Voting B = 32% Cash flow B = 9%

16

Board Composition The ratio of board seats (directors and supervisors) held by the largest shareholders. Management participation: a dummy variable that takes the value of one if the controlling shareholder (including its members) also serves as the chairman and president of the company, and takes the value of zero, otherwise.

also serves as the chairman and president of the company, and takes the value of zero, otherwise..")

19

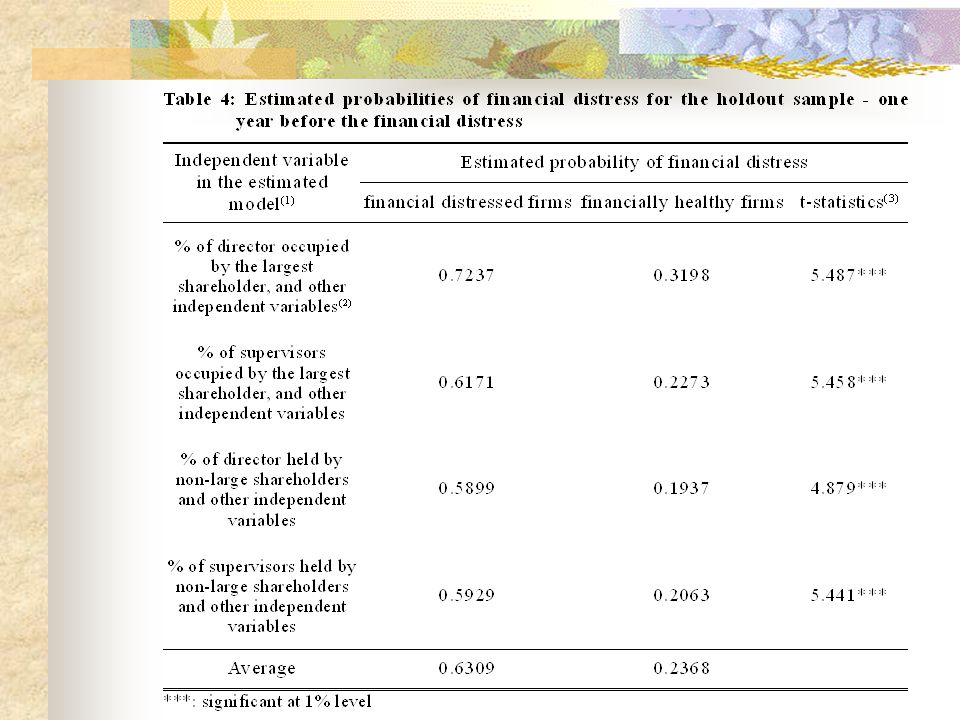

The Estimated and Holdout Samples The first two thirds of our sample is grouped into an estimated sample. Similar logistic regressions are run on the estimated sample using the data one-year before the distress to generate parameter estimates. The data of the holdout sample one-year before the crisis are then plugged into the estimated model. A simple transformation of the following form gives us the estimated probability of financial distress,

20

where P i = the estimated probability of financial distress for firm i of holdout sample = the vector of estimated regression coefficients by using the estimate sample x i = the vector of the values of independent variables for firm i by using the data of holdout sample

23

Control Financial Performance For the good performance sample, board structure variables are more capable of explaining the occurrence of financial distress. Specifically, when the controlling shareholder holds more seats on the board, even good performance companies receive a higher probability for distress next year. As to the bad performance sample, the ownership and debt ratio represent the more powerful explanatory.

24

Conclusion The argument that the controlling shareholder may desire to prolong the expropriation honeymoon suggests that poor governance may not lead to higher probability of financial failure. However, since our sampling period essentially covers the Taiwan serious economic recession, poor macroeconomic factors might have speeded up the occurrence of financial distress even if the controlling shareholders tried to prevent it from happening.

25

Conclusion An early warning system cannot be complete without incorporating the characteristics of corporate governance. Strengthening the mechanism of corporate governance would help to reduce the likelihood of financial failures, especially in an environment of weak corporate governance.

Similar presentations

>")

Chung Yuan Christian University.>")

>")

Qiao Liu, HKU Corporate Governance.>")