Download presentation

Presentation is loading. Please wait.

1

A Review of: Global Soft Magnetic Core Shipments & Nickel Commodity Prices Spring-2009 TTA Meetings May 14, 2009 Spring-2009 TTA Meetings May 14, 2009 Presented by the Staff of the International Magnetics Association

2

Topics Topics Overview of Soft Magnetics IndustryOverview of Soft Magnetics Industry Ferrite PerformanceFerrite Performance Powder Core PerformancePowder Core Performance Nickel Commodity Price ImpactNickel Commodity Price Impact Challenges for 2009Challenges for 2009 Overview of Soft Magnetics IndustryOverview of Soft Magnetics Industry Ferrite PerformanceFerrite Performance Powder Core PerformancePowder Core Performance Nickel Commodity Price ImpactNickel Commodity Price Impact Challenges for 2009Challenges for 2009

3

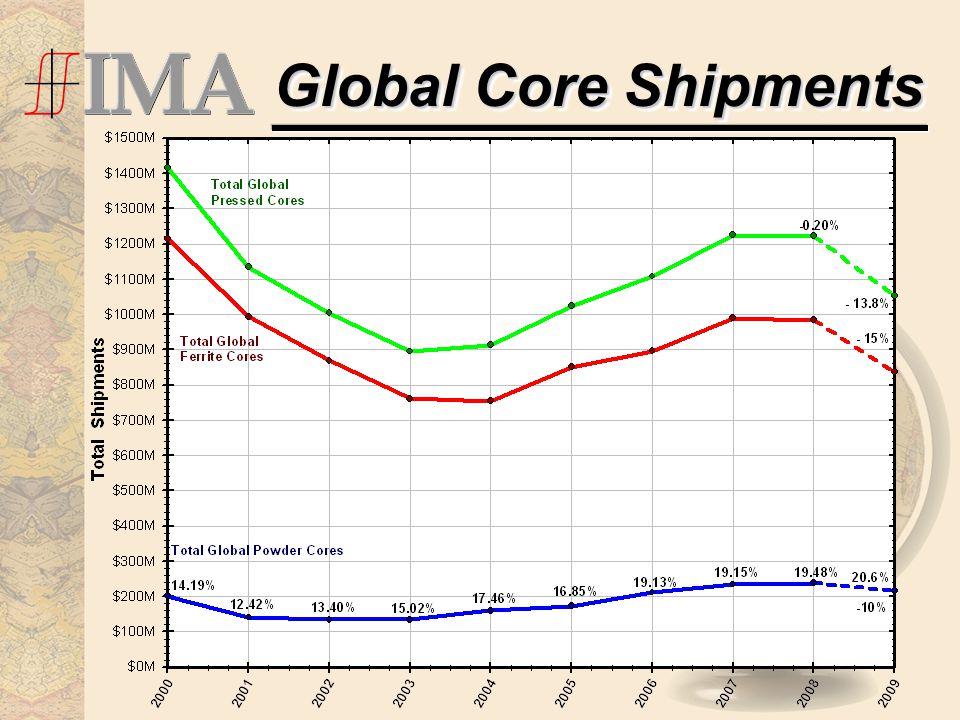

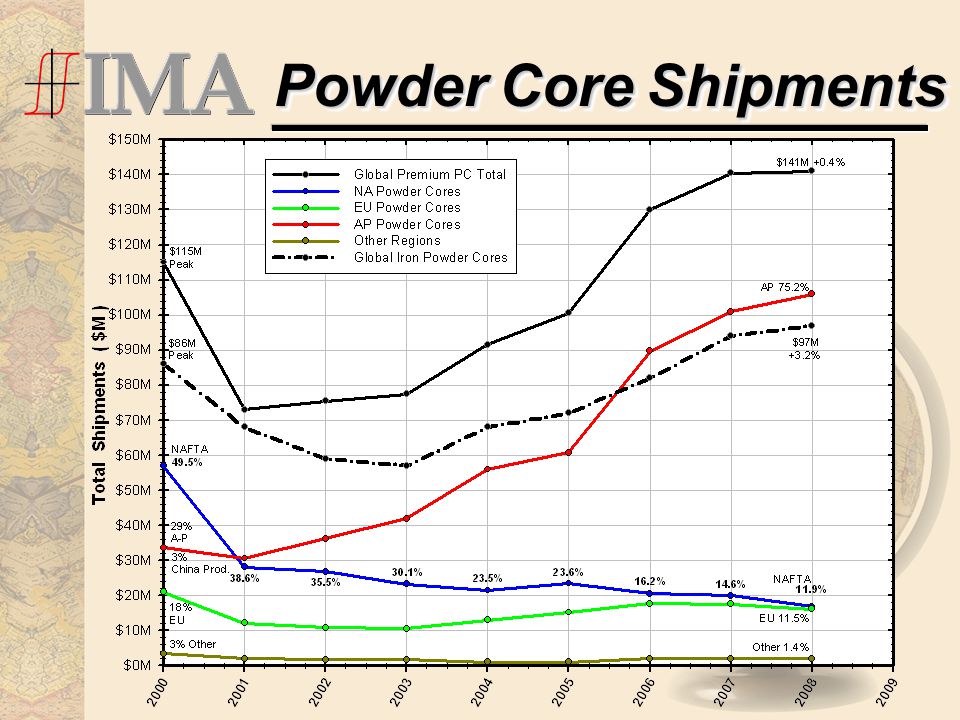

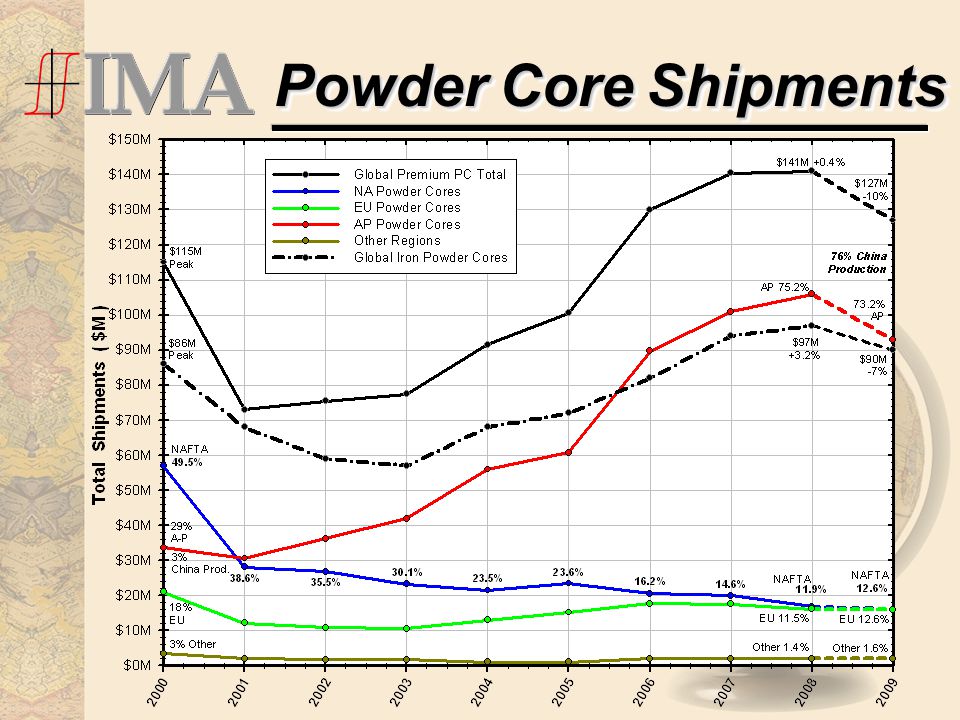

Soft Magnetic Cores Ferrites include MnZn and NiZn cores:Ferrites include MnZn and NiZn cores: –2008 at -0.6% under 2007 (forecast was +5.5%). ◦08Q1 & Q2 +15% to +30%; 08Q3 & Q4 -20% to -30%. –2009 forecast is for -15% to -30% (09Q1 -30 to -40%). Powder Cores have two segments:Powder Cores have two segments: –2008 Premium Cores at +0.4% over 2007 (fcst. +8%). ◦2009 forecasts are for a decline of -10%. –2008 Iron Powder at +3.2% over 2007 (fcst. +7%). ◦2009 forecast not certain, typically not as volatile as Prem. PC. Powder core industry still adding capacity.Powder core industry still adding capacity. –Will pose bottom line challenges in 2009. Ferrites include MnZn and NiZn cores:Ferrites include MnZn and NiZn cores: –2008 at -0.6% under 2007 (forecast was +5.5%). ◦08Q1 & Q2 +15% to +30%; 08Q3 & Q4 -20% to -30%. –2009 forecast is for -15% to -30% (09Q1 -30 to -40%). Powder Cores have two segments:Powder Cores have two segments: –2008 Premium Cores at +0.4% over 2007 (fcst. +8%). ◦2009 forecasts are for a decline of -10%. –2008 Iron Powder at +3.2% over 2007 (fcst. +7%). ◦2009 forecast not certain, typically not as volatile as Prem. PC. Powder core industry still adding capacity.Powder core industry still adding capacity. –Will pose bottom line challenges in 2009.

. Powder Cores have two segments:Powder Cores have two segments: –2008 Premium Cores at +0.4% over 2007 (fcst. +8%). ◦2009 forecasts are for a decline of -10%. –2008 Iron Powder at +3.2% over 2007 (fcst. +7%). ◦2009 forecast not certain, typically not as volatile as Prem. PC. Powder core industry still adding capacity.Powder core industry still adding capacity. –Will pose bottom line challenges in Ferrites include MnZn and NiZn cores:Ferrites include MnZn and NiZn cores: –2008 at -0.6% under 2007 (forecast was +5.5%). ◦08Q1 & Q2 +15% to +30%; 08Q3 & Q4 -20% to -30%. –2009 forecast is for -15% to -30% (09Q1 -30 to -40%). Powder Cores have two segments:Powder Cores have two segments: –2008 Premium Cores at +0.4% over 2007 (fcst. +8%). ◦2009 forecasts are for a decline of -10%. –2008 Iron Powder at +3.2% over 2007 (fcst. +7%). ◦2009 forecast not certain, typically not as volatile as Prem. PC. Powder core industry still adding capacity.Powder core industry still adding capacity. –Will pose bottom line challenges in")

4

Global Core Shipments

6

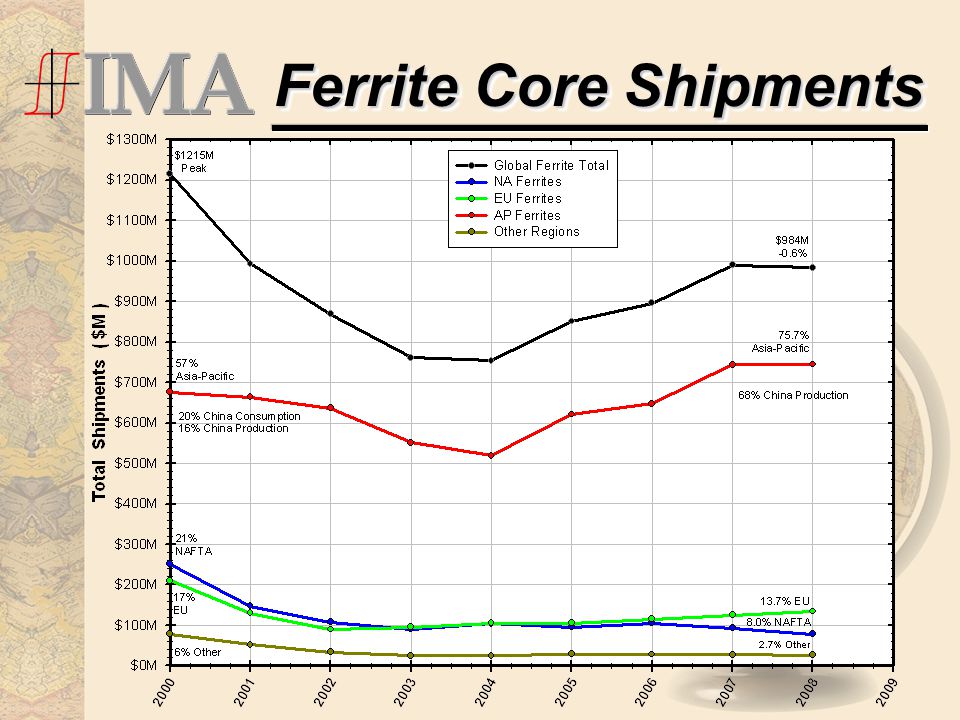

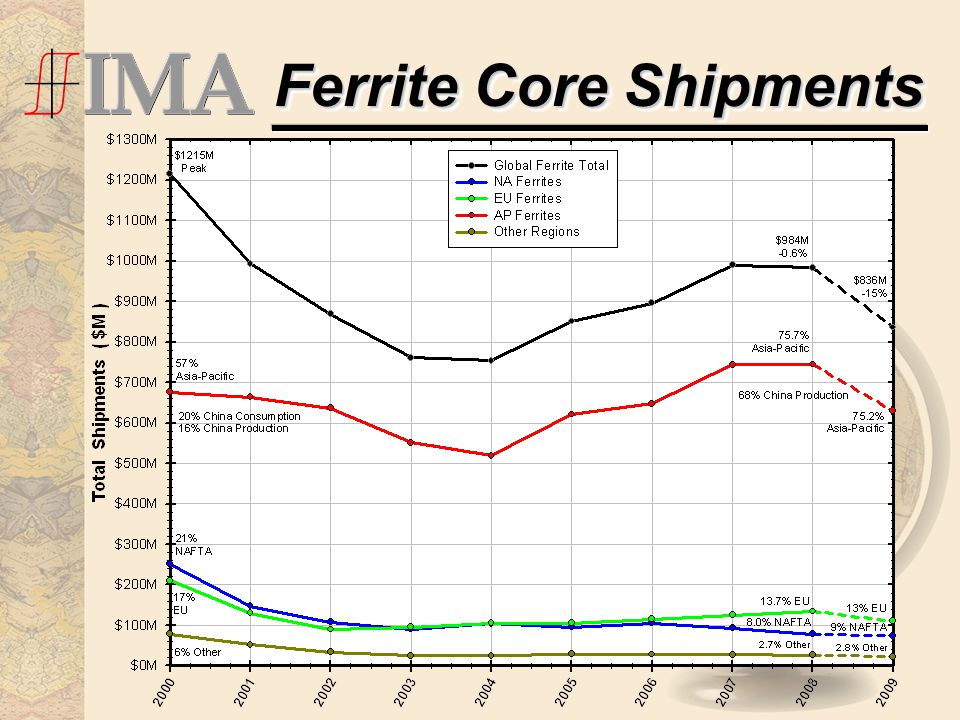

Ferrite Core Shipments

9

Powder Core Shipments

12

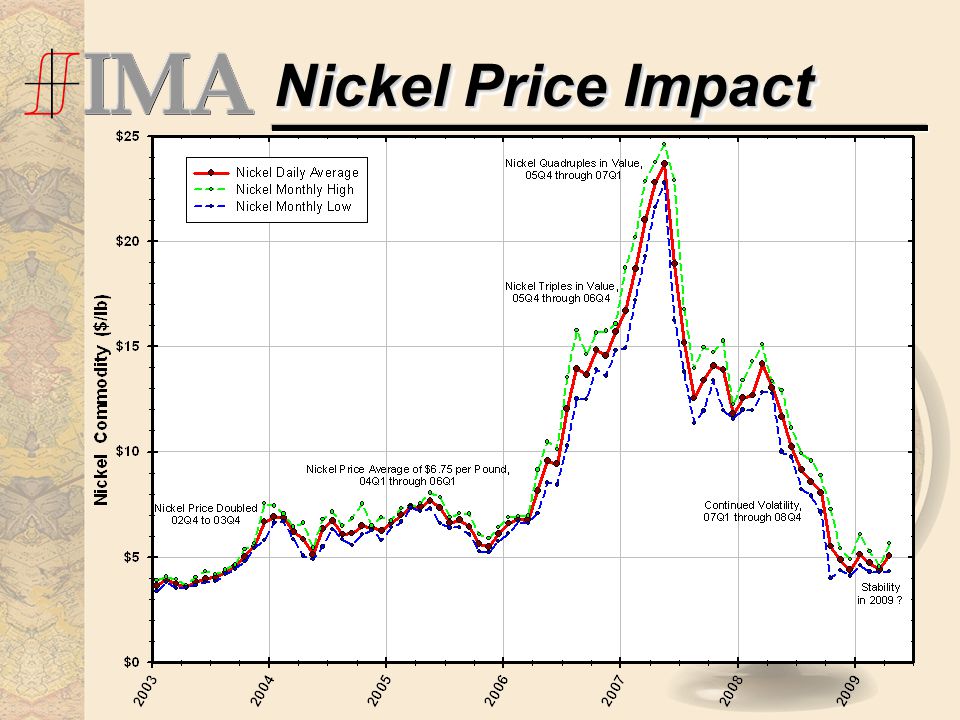

Nickel Price Impact

14

Challenges for 2009 The past 6-8 months have been difficult for most core manufacturers.The past 6-8 months have been difficult for most core manufacturers. –Bookings declines in 08Q4 and shipment declines for current months of 2009 are off 30% to 40% YTY. Excess production capacity in ferrites and powder cores (most located in China).Excess production capacity in ferrites and powder cores (most located in China). –Chinese do not have a correct global view of the markets and Western competitors sizes. What will happen in the raw material markets: iron, nickel, manganese, etc.?What will happen in the raw material markets: iron, nickel, manganese, etc.? The past 6-8 months have been difficult for most core manufacturers.The past 6-8 months have been difficult for most core manufacturers. –Bookings declines in 08Q4 and shipment declines for current months of 2009 are off 30% to 40% YTY. Excess production capacity in ferrites and powder cores (most located in China).Excess production capacity in ferrites and powder cores (most located in China). –Chinese do not have a correct global view of the markets and Western competitors sizes. What will happen in the raw material markets: iron, nickel, manganese, etc.?What will happen in the raw material markets: iron, nickel, manganese, etc.?

.Excess production capacity in ferrites and powder cores (most located in China). –Chinese do not have a correct global view of the markets and Western competitors sizes. What will happen in the raw material markets: iron, nickel, manganese, etc. What will happen in the raw material markets: iron, nickel, manganese, etc.. The past 6-8 months have been difficult for most core manufacturers.The past 6-8 months have been difficult for most core manufacturers. –Bookings declines in 08Q4 and shipment declines for current months of 2009 are off 30% to 40% YTY. Excess production capacity in ferrites and powder cores (most located in China).Excess production capacity in ferrites and powder cores (most located in China). –Chinese do not have a correct global view of the markets and Western competitors sizes. What will happen in the raw material markets: iron, nickel, manganese, etc. What will happen in the raw material markets: iron, nickel, manganese, etc. .")

15

Questions Questions ??

Similar presentations

910-6452 Direct:+1 (503) 894-6022>")

910-6452 Direct:+1 (503) 894-6022>")