Download presentation

Presentation is loading. Please wait.

1

Connecting Two Views on Financial Globalization: Can We Make Further Progress? Shang-Jin Wei IMF, NBER & CEPR Personal Views Only

3

What does Financial Globalization do? The gap between theories and empirics –In theory, benefits through many channels Direct: savings, cost of capital, and transfer of technology, Indirect: development of domestic financial market, more specialization, and better policies –In the data, evidence not strong (Eichengreen, 2000; Prasad, Rogoff, Wei, and Kose, 2003; Kose, Prasad, Rogoff, and Wei, 2006)

.")

4

Reconciling theories with empirical patterns: Two independent proposals –The composition effect: Some capital flows are more beneficial than others –The threshold effect: Benefits of FG can be realized only if the recipient countries meet some conditions Eichengreen (2000), Prasad, Rogoff, Wei, and Kose (2003)

, Prasad, Rogoff, Wei, and Kose (2003)")

5

Roadmap for discussion How do the two effects work? My take on the two effects –The composition is a reflection of the threshold effect Challenges to this interpretation Response to the challenge

6

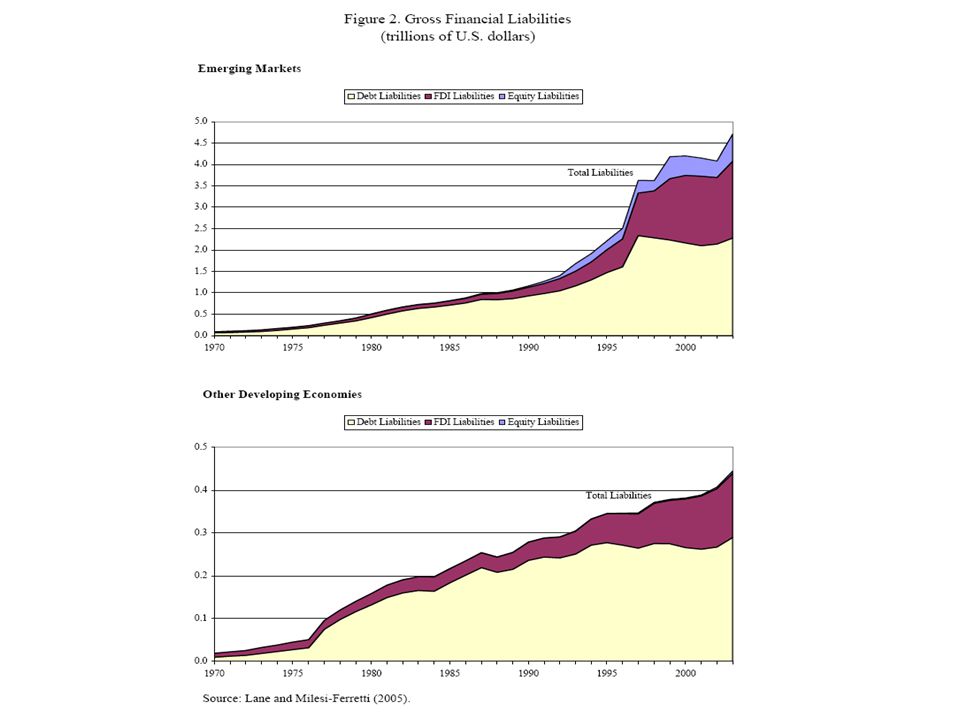

The composition hypothesis Not all capital flows are equal FDI and maybe portfolio inflow are more beneficial to growth than debt –Desoto and Reisen 2001; Bekaert, Harvey, and Lundblad, 2005, JFE FDI is also less volatile than international bank loans -> More reliance on bank loans increases vulnerability to currency crashes –Frankel and Rose, 1996; Frankel and Wei, 2005

7

Volatility of (FDI/GDP) and (Loan/GDP) (1980-2003, Measured by Standard Deviation) FDI/GDP Loan/GDP

and (Loan/GDP) ( , Measured by Standard Deviation) FDI/GDP Loan/GDP")

8

The Threshold Effect Certain minimum conditions have to be met before a country can benefit from FG Institutions –Low corruption / decent rule of law Otherwise, FG may exacerbate distortions –Reasonable level of financial development So international capital can be channeled into investment –Human capital

9

Are the Two Effects Connected? Yes! –Earlier: Wei (2000, 2001), Wei and Wu (2002) –Recently: Faria and Mauro (2005) Why? –Insight from the literature from corporate finance –A built-in bias in the international financial architecture

, Wei and Wu (2002) –Recently: Faria and Mauro (2005) Why. –Insight from the literature from corporate finance –A built-in bias in the international financial architecture.")

10

Challenges Countries with worse financial institutions appear to attract more (not less) FDI Albuquerque (JIE 2003) Also see Hausmann and Fernandez-Aris (2000) Even if public governance and composition of capital inflows are related as hypothesized, how do we know the relationship is causal?

FDI Albuquerque (JIE 2003) Also see Hausmann and Fernandez-Aris (2000) Even if public governance and composition of capital inflows are related as hypothesized, how do we know the relationship is causal")

11

Answers to the Challenges Separate the effects of financial development and weak governance Find instrumental variables for government corruption and financial development

12

Why would weaker financial development be associated with more FDIs? Caballero, Farhi and Gourinchas, 2005, “An eqbm model of ‘global imbalances’ and low interest rates.” Ju and Wei, 2005, “A solution to two paradoxes on international capital flows”

13

Instrumental variable for government corruption: Initial cost to colonizers –mortality rate of European settlers before 1850 Acemoglu, Johnson, and Robinson (AER 2001) Alternative: initial population density in 1500

Alternative: initial population density in 1500")

14

Instrumental variables for financial development: Legal origins: La Porta, Lopez-de-silanes, Shleifer, and Vishny (JPE 1998) Settler mortality

Settler mortality")

15

(History-based) instrumental variables Corruption is mostly affected by settler mortality but not by legal origin Financial development is affected by both legal origins and settler mortality.

instrumental variables Corruption is mostly affected by settler mortality but not by legal origin Financial development is affected by both legal origins and settler mortality.")

16

The basic specification: (1)Composition(j) = β1 Corruption(j) + β2 FinDev(j) + Z(j)Γ + e(j) Zj is a vector of control variables, β1, β2, and Γ are parameters ej is a random error.

Composition(j) = β1 Corruption(j) + β2 FinDev(j) + Z(j)Γ + e(j) Zj is a vector of control variables, β1, β2, and Γ are parameters ej is a random error.")

17

First Stage Regressions: Using Histories to Instrument Modern-day Institutions

18

Explaining the Ratio of FDI/ Total Foreign Liabilities in 2003

19

Explaining Portfolio Equity/Total Foreign Liabilities in 2003

20

Explaining Portfolio Debt/ Total Foreign Liabilities in 2003

21

Explaining Outstanding Foreign Loans/ Total Foreign Liabilities in 2003

22

Total Capital Inflows Per Capita in Logarithm (2003)

")

23

Table 6: Alternative Measure of Institutions – Average of Six World Bank Indicators

24

Table 7: Adding more control variables (IV Regressions)

")

25

Summary (1) Corruption does not appear to have a strong effect on a country’s total foreign liabilities. It affects the composition significantly. As FDI and portfolio debt are strongly discouraged, foreign loans take their places. Corruption increases a country’s vulnerability to a balance-of-payments crisis by altering its composition of capital inflows in an unfavorable direction.

26

Summary (2) Financial development does not appear to have a strong effect on total foreign liabilities. However, a weaker financial system appears to induce more FDIs. A weaker financial system is likely to discourage inflows of portfolio equity and portfolio debt.

Similar presentations

; Kaminsky,>")

>")

Two theories of the state 1. Contract theory: the state provides the legal.>")