Download presentation

Presentation is loading. Please wait.

1

Policy Imbalances and the Uneven Recovery John B. Taylor Conference on The Uneven Recovery: Emerging Markets versus Developed Economies Oct 14, 2011

2

Two Global Imbalances (1)Current account imbalances (2)Monetary imbalances Both relevant for emerging markets versus developed economies We hear much about the first But the second may be more important

Current account imbalances (2)Monetary imbalances Both relevant for emerging markets versus developed economies We hear much about the first But the second may be more important")

3

Current Account Imbalances A frequent topic for international coordination A perennial topic for G-20, IMF, OECD (WP3) Sometimes used for calls by US and Europe for exchange rate changes by EME Frequently blamed for the financial crisis – Saving glut flows into US, lowers interest rates – Alternative to the “too low for two long” view Now “rebalancing” is a major focus of the G-7, G-20, IMF

Sometimes used for calls by US and Europe for exchange rate changes by EME Frequently blamed for the financial crisis – Saving glut flows into US, lowers interest rates – Alternative to the too low for two long view Now rebalancing is a major focus of the G-7, G-20, IMF")

4

Link to Saving-Investment Gap Saving – Investment =Net Exports Y=C+I+G+X Y-C-G= I+X S=I+X S-I=X Look at recent history

5

United States C/Y and G/Y

8

Source: Borio and Disyatat (2011)

")

9

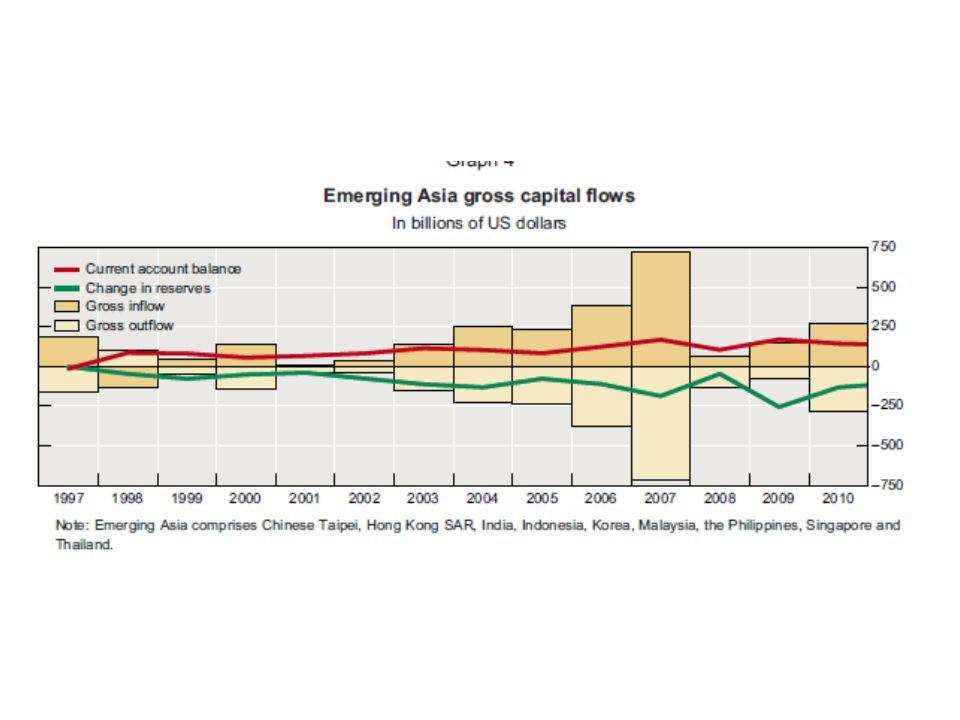

Capital Flows and the Current Account Consider 2004 (Billions of dollars) Exports of goods and services and income receipts 1531 Imports of goods and services and income payments -2118 Unilateral current transfers -81 Current Account Deficit -668 U.S. Owned Assets Abroad -856 Foreign Owned Assets in the United States 1440 Statistical discrepancy & other reconciliations 84 http://www.bea.gov/bea/newsrelarchive/2005/trans305.pdf Source: Note that these are capital flows Not capital stocks U.S.GDP was $11734 billion in 2004, so CA was 5.7 percent as a share of GDP

10

The connection between current account and change in official reserves can be particularly weak Current account = Change in official reserves + other gross outflows - other gross inflows

12

United States

13

Mainly Europe rather than emerging markets

14

If not the current account, then what is driving these flows? Monetary policy Exchange rate policy

15

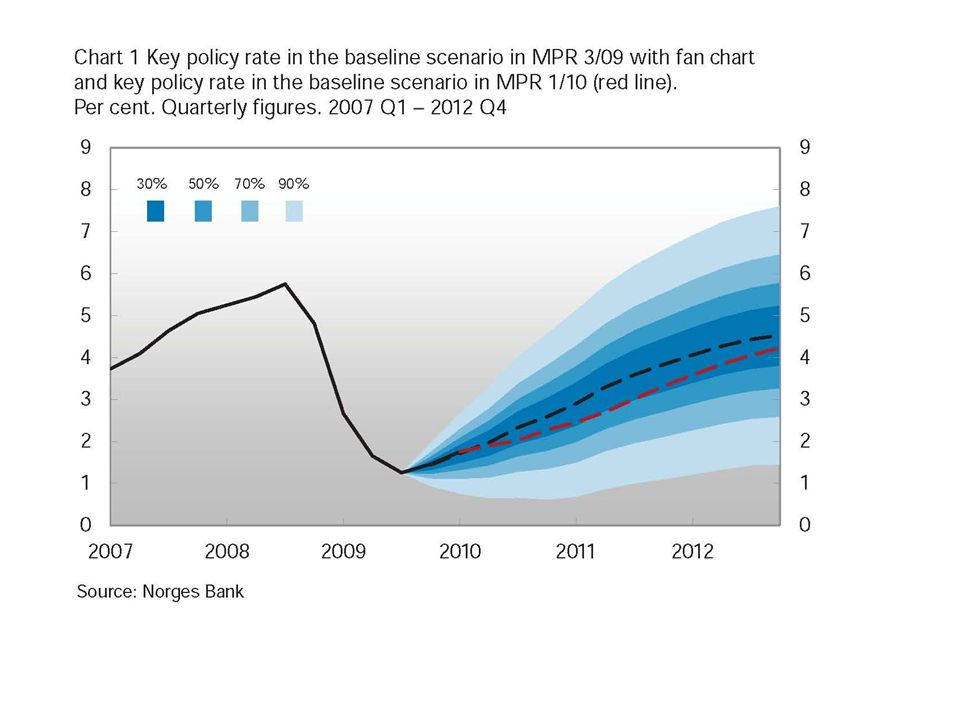

Clear Evidence from a Very Transparent Central Bank Norges Bank very explicit and transparent in accounting for how external variables affect interest rate path Useful to consider several episodes in past few years Reveals foreign interest rate as the most significant reason for deviating from basic rule

16

Policy rate in 1/2008 (with fan chart) and the increase in the policy rate in 2/2008 (red line) Source: Norges Bank 90%70%50%30%

and the increase in the policy rate in 2/2008 (red line) Source: Norges Bank 90%70%50%30%")

17

Factors behind changes in the interest rate path from 1/2008 to 2/2008 Higher demand in Norway Higher inflation in Norway Higher interest rates abroad and developments in the foreign exchange market Lower growth abroad Higher risk premium in the money market

19

From 1-10

20

From Øistein Røisland “Monetary Policy in Norway”

21

From MPR 1/10

22

From OECD Survey Norway, 2010

23

Example from Sebastian Edwards (2005) “The Relationship Between Exchange Rates and Inflation Targeting Revisited” Empirical evidence that target interest rate in EM central banks responds to exchange rates

The Relationship Between Exchange Rates and Inflation Targeting Revisited Empirical evidence that target interest rate in EM central banks responds to exchange rates")

24

Continued from Sebastian Edwards (2005)

")

25

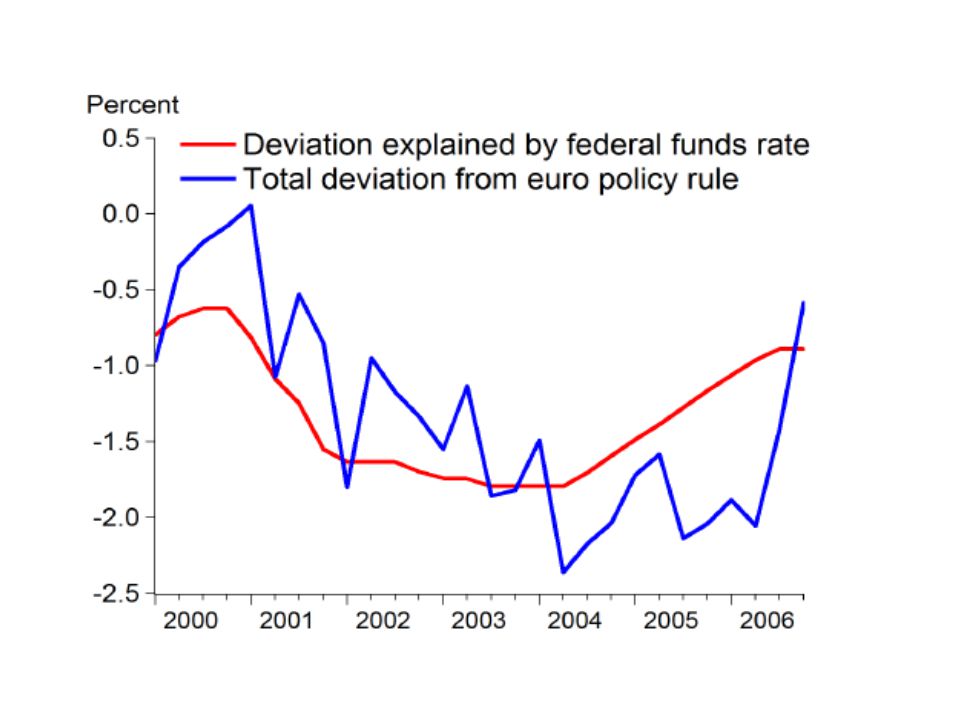

Example from ECB during 2000-2006 Sample 2000.1 - 2006.4. Inflation = 4-quarter rate of change in the harmonized index of consumer prices GDP gap = % deviation of real GDP from trend. Regress deviation of ECB rate from Taylor rule on federal funds rate. Estimated coefficient =.21 – standard error of.06. – Plot of the actual and fitted values from this regression:

27

Illustrative Chart from the OECD, March 2008

28

The Case of the Uneven Recovery Very low policy rate in US Creates pressures on EM central banks to hold rates lower than they would be for domestic price and output stability – Also creates pressures to intervene in currency markets and impose capital controls Leads to higher inflation, and perhaps more crises So need to have “monetary rebalancing” But little interest from developing countries

29

General Sources of Instability Consider two country model with i affecting i* Interest rates are set according to: Solving for the interest rates results in the following

30

Conclusion Need to focus more on “monetary rebalancing” – Side by side discussion with “current account rebalancing” May be more important than current account rebalancing But how? – More global leadership – Global inflation target

Similar presentations

Conference.>")