Download presentation

Presentation is loading. Please wait.

1

Dennis J. Powers Jr. AIC, ARM, CPCU Lamb, Little & Co.

2

Hard Market Soft Market

3

Hard Market Focus on Profitability Premiums Increase Don’t Like Risk

4

Soft Market Focus on Growth Premiums Decrease Underwriters Appetite Is More Aggressive

5

Insurance Programs Guaranteed Cost Loss Sensitive

6

A classic method of risk transfer: You pay the carrier premium to cover your claims.

7

Pro: Your cost is fixed, regardless of claims experience. Con: You flex with the marketplace and the status of your industry’s loss history. Pro: Your cost is fixed, regardless of claims experience. Con: You flex with the marketplace and the status of your industry’s loss history.

8

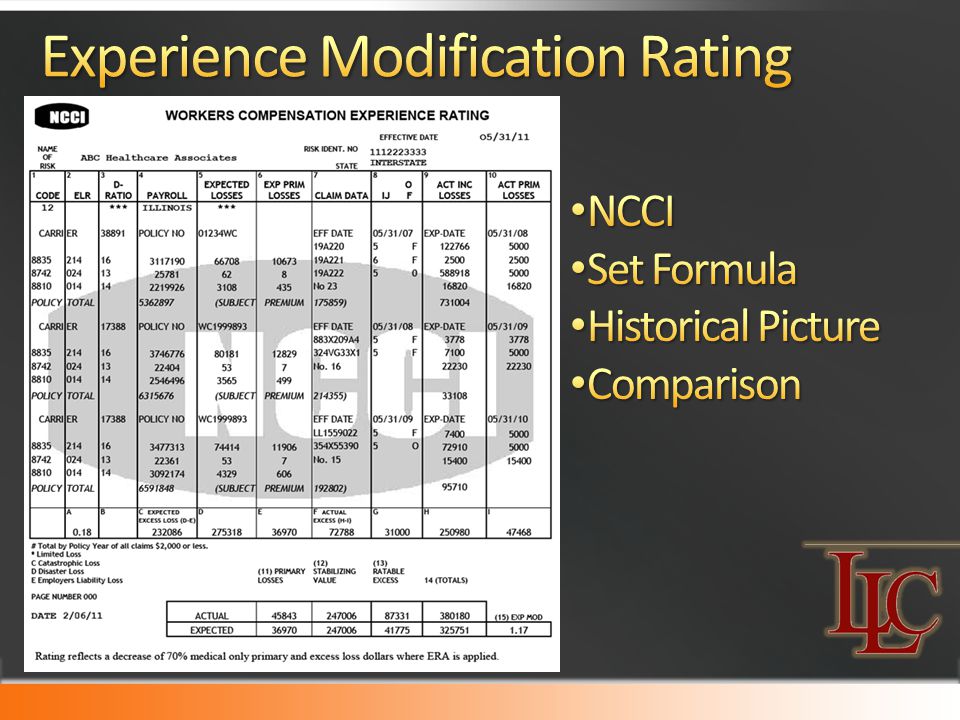

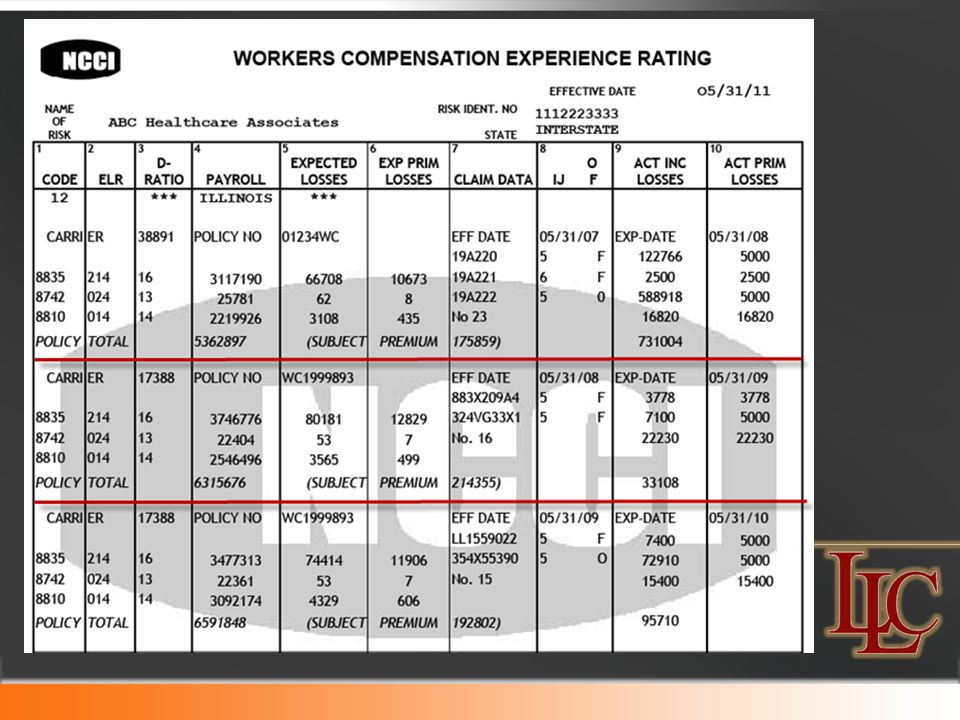

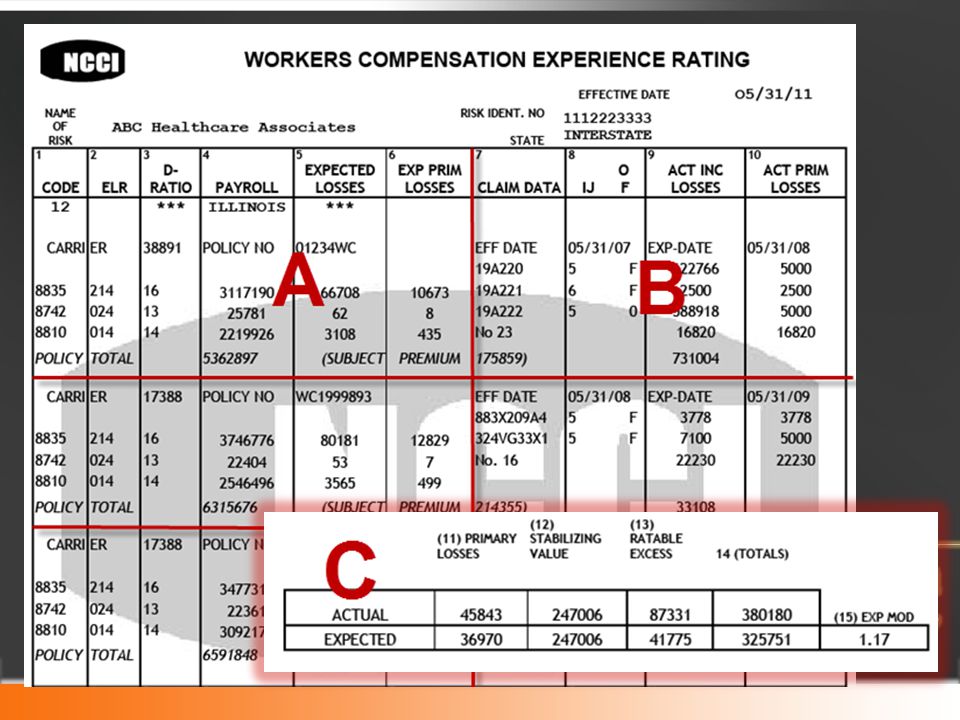

1.Classifications 2.Experience Modification 3.Schedule Credit

10

Exposure/100 x Rate = Manual Premium 10,000 x 5.02= $50,200

25

Your Information

27

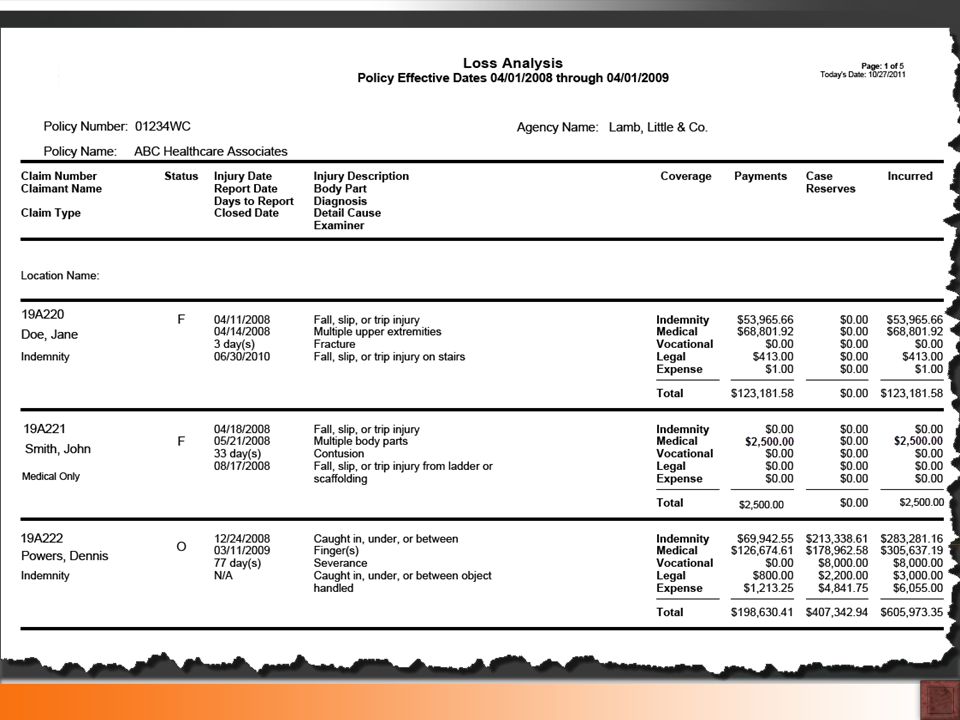

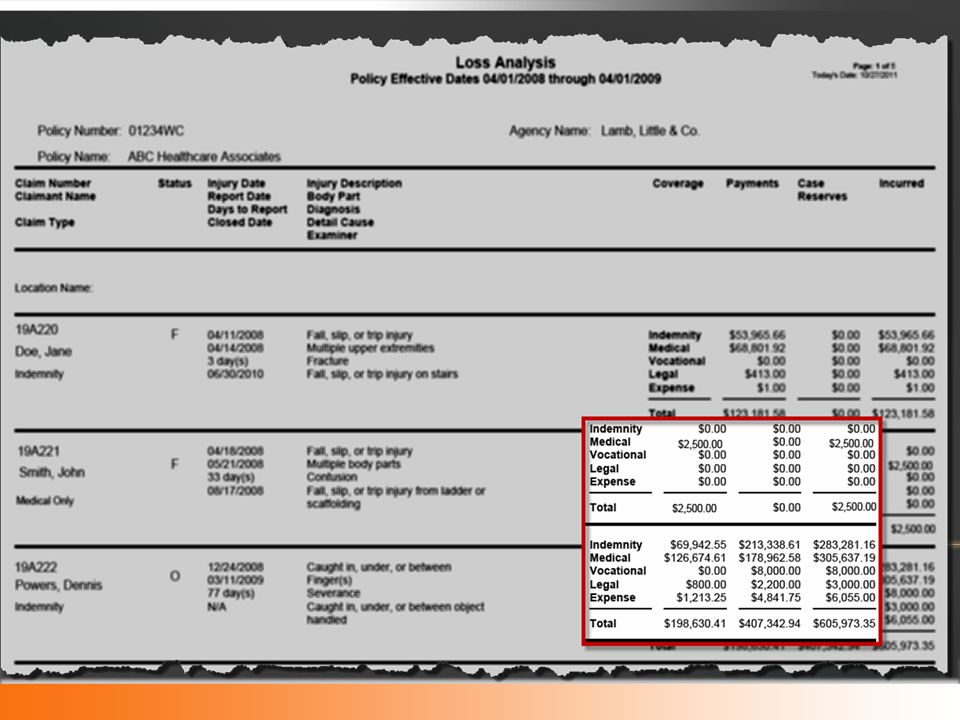

Review Your Claims for Accuracy Utilize Loss Control

29

This is where all the companies are going to be different. The more you bring to the table, the more aggressive you can be. This is where all the companies are going to be different. The more you bring to the table, the more aggressive you can be.

30

Claims Mgmt: Early Reporting Accident Investigation Return to Work Loss Control: Documented Safety Program Documented Training Program Loss Assessment Report

31

George M. Canavan, AIC Lamb, Little & Co.

33

Medical Benefits Temporary Total Disability Permanent Partial Disability Penalties

34

Source: Liberty Mutual Data Warehouse

35

Don’t Underestimate Anything

37

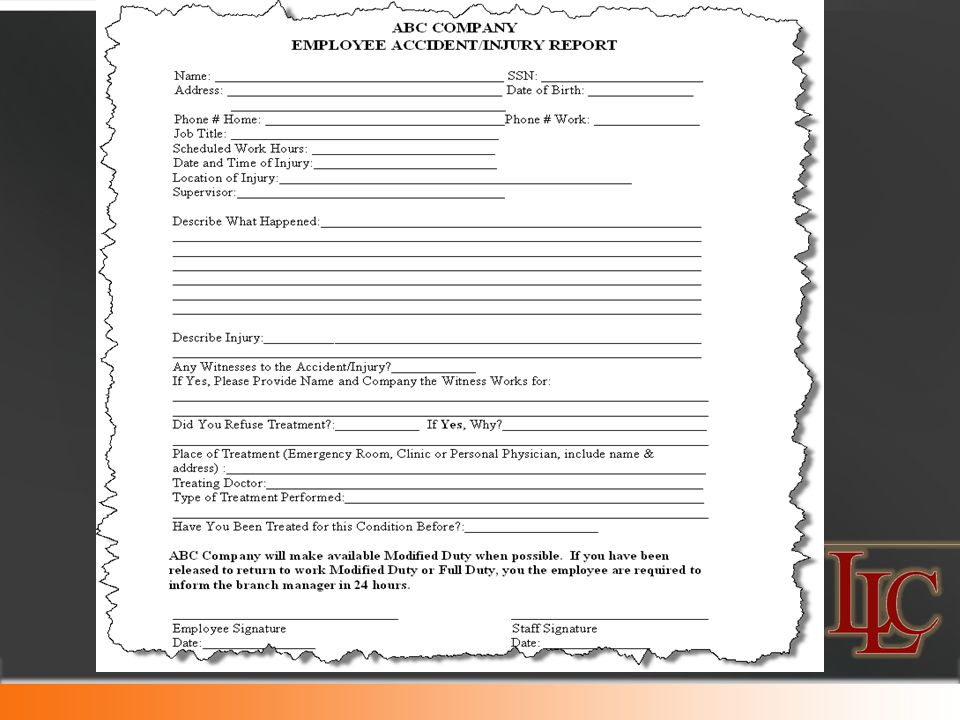

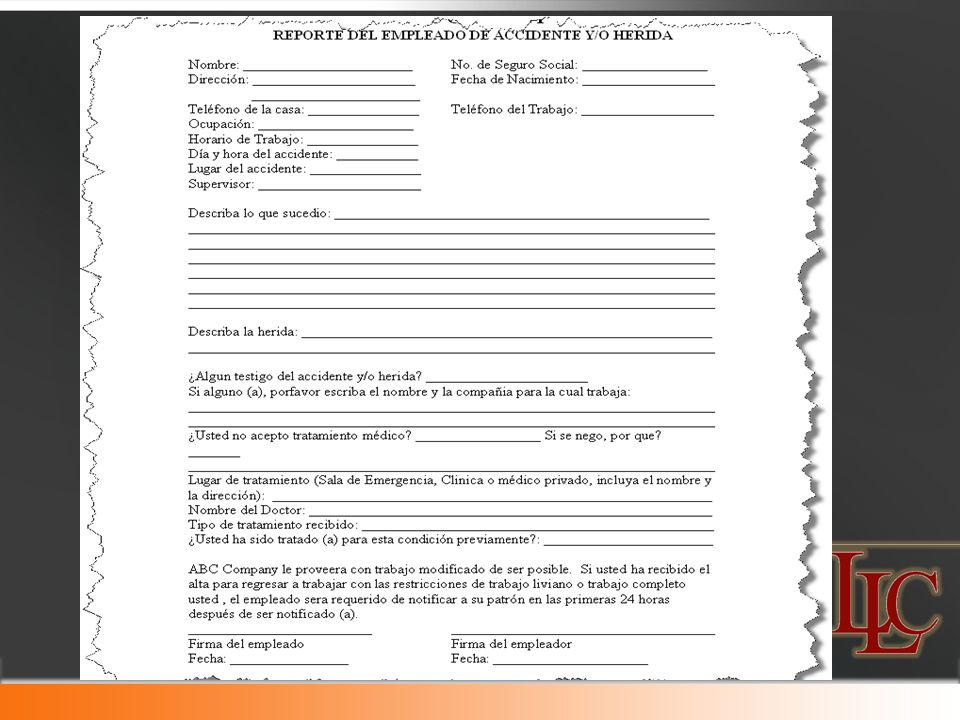

Employee Incident Report Employee Incident Report-Spanish Supervisors WC Investigation Report Witness Form

42

Delay in Reporting Can Be Expensive Threat of Litigation Slows Down Claims Investigation

43

Provides You Control Provides Significant Savings Conveys the Right Message to Workforce

44

Per NCCI, the median incurred cost of a WC claims exceeding more than 7 days of lost time from work is $31,600. Claims under 7 days of lost time, the average claim is <$10,000.

45

Why Conduct A Claim Review?Who Participates In a Claim Review?When Are Claim Reviews Done?

49

Designated Claim Handler How Do Employees Report New Claims? Accident Investigation Subrogation Investigation Time Sheet Initial Explanation of Claims Process/Benefits to Emlployee Claim Reporting to Insurance Carrier Initial Medical Care Internal Claims Management Procedures Supervisor/Management Training Return To Work Programs Establish Special Claim Handling Instructions

50

Bill Crimmins, CSP Titan Risk Management, LLC

52

1.Safe Behavior 2.Technically Proficient 3.Compliant

53

Loss Control Representative Survey Risk Selection Research Your website OSHA (OSHA.gov) DOT (safersys.org) BLS Statistics Report to Underwriter

DOT (safersys.org) BLS Statistics Report to Underwriter")

54

Periodic Risk Assessments Safety And Health Program Document Inspections / Efforts Document Employee Training Enforce Your Program Accountability

55

What are my areas of concern Do I have the expertise to address it If not, get help

56

Use Loss Control & Manage Claims Reduce Experience Modification Factor Allows Your Agent To Present You As Best In Class to Negotiate Your Schedule Credit

57

Financial (CFO, Comptroller, Etc.) Coverage Placement Human Resources Claims Administration Return To Work Production OSHA, Return to Work, Accident Investigation

Coverage Placement Human Resources Claims Administration Return To Work Production OSHA, Return to Work, Accident Investigation")

58

Create Accountability Analyze Incurred Losses for Prevention By Location, Season, Cause, etc. Incent Departments to Improve Safety.

59

By Department, or Location

60

By Time of Year

61

By Time of Day

62

By Type of Injury

63

Direct Loss Indirect Loss

64

INDIRECT Loss of Production Employee Morale Loss of Quality Employee Time of Staff to Manage Claims Damage to Equipment & Property

65

YOU LOSE $4 FROM YOUR BOTTOM LINE FOR EVERY $1 YOUR INSURANCE CARRIER PAYS IN WORKERS’ COMPENSATION CLAIMS INSURANCE YOU $1

67

Question 1: Is your rating information accurate? Question 1: Is your rating information accurate?

68

Question 2: Are you managing your claims to have an impact on your premium? Question 2: Are you managing your claims to have an impact on your premium?

69

Question 3: Are you managing your Loss Control Service to have an impact on your premium? Question 3: Are you managing your Loss Control Service to have an impact on your premium?

70

Question 4: Are you creating accountability by properly communicating the results? Question 4: Are you creating accountability by properly communicating the results?

71

Question 5: Are your current vendors a resource? Question 5: Are your current vendors a resource?

Similar presentations