Download presentation

Presentation is loading. Please wait.

1

Chapter 4 Understanding Interest Rates

2

The talk last Thursday was very comprehensive. I will add only a little bit content One video clip about John Howard, former Prime Minister of Australia. He promised no raise in interest rate. But interest rate was raised several times. Why he had to? The real power behind interest rate change?

3

Fixed Payment Loan— Yield to Maturity

4

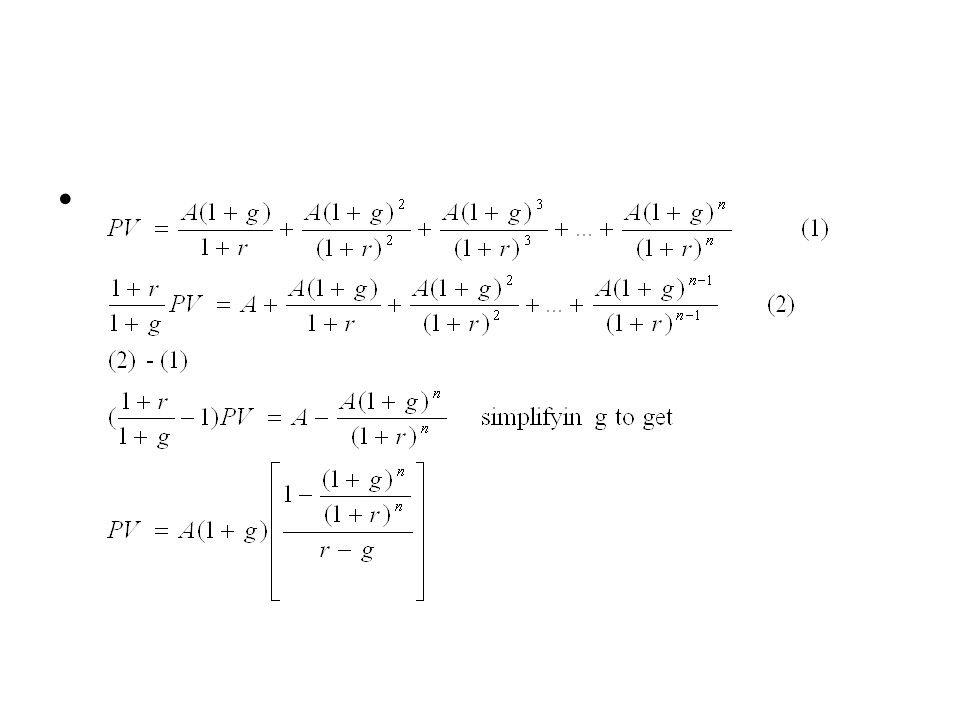

Calculating present value

5

The above method is a general technique. We will calculate an annuity growing at the rate of g

7

Credit Market Instruments Simple Loan Fixed payment Loan Coupon Bond Discount Bond

8

The usefulness of different kinds of loans Fixed payment Loan –Good for stable income entities such as families in residential mortgages Coupon Bond –Good for large investment whose payoff in the deep future Discount Bond –Tax advantage

9

Example of the tax advantage of discount bond 20 year’s coupon bond. Principle 1000 dollar. 6% coupon paid annually. Interest rate at 6%. So bond is sold at face value. A discount bond for 20 years. Current price 1000 dollar. Compounding at 6% per annum, future value at 3207.14 Assume the tax rate for the investor is 30%. Calculate the final wealth for both bonds at the end of the 20 th year.

10

A further assumption: Interest rate doesn’t change over the bonds’ life. All coupon income reinvested in the same kind of coupon bond. With coupon bond the final wealth is 2277 With discount bond, the final wealth is 2545. Near 300 dollar saving Synthetic bond: coupon and principle go to different investors.

11

The Invention of Interest: Sumerian Loans From Marc van de Mieroop in The Origin of Value The earliest recorded loan contracts can be attributed to over 5000 years ago, in today’s Iraq. The Sumerian word for interest was also used to indicate a lamb. (p. 24) The biological connection –Sheep give birth to lamb –Money give birth to interest

The biological connection –Sheep give birth to lamb –Money give birth to interest.")

12

What is “normal” or “natural” interest rate? Sumer: 20% Rome: 12% Prime rate: around 6% Credit card rate: 18% Why credit card holders are willing to accept such high rates?

13

The biological foundation of discount rate Consider the life in our hazardous evolutionary past. Suppose a mother gives birth to 10 children. On average, 2 grows to reproductive age. The expected life expectancy is 12. The discount rate can be calculated as

14

10(1+r)^(-12) = 2 r = 14.5% Adding inflation rate, it is pretty close to the credit card rate.

^(-12) = 2 r = 14.5% Adding inflation rate, it is pretty close to the credit card rate.")

15

Interest rate and housing price Suppose a house is bought for 200,000 dollars. The required down payment is 20% of the house price. The rest of the money is borrowed through a 25-year mortgage with monthly payments. What is the amount of down payment and what is the amount of borrowing? The annual percentage rate on the mortgage loan is 6%. Calculate the monthly payment. Now suppose the government tries to making housing more affordable. It reduces the interest rate to 4%. What is the new monthly payment on the mortgage? Does the government policy improve the affordability of housing market over the short term? If the housing supply doesn’t increase, those who can afford the monthly payment of the original 200,000 dollar house will likely to buy the same kind of house. What will be the new price of the house which as originally sold for 200,000 dollars, if monthly payment is kept at the same level when interest rate was at 6% and down payment is 20% of the housing price? What is the new down payment? Over the long term, will lowering the interest rate alone improve or deteriorate the affordability of housing market?

16

Homework 9, 11, 13, 15

17

Extra Homework Suppose a house is sold for 300,000 dollars. The required down payment is 25% of the house price. The rest of the money is borrowed through a 30-yeat mortgage with monthly payments. What is the amount of borrowing? The annual percentage rate on the mortgage loan is 7%. Calculate the monthly payment. Now suppose the government tries to making housing more affordable. It reduces the interest rate to 4%. What is the new monthly payment on the mortgage? Does the government policy improve the affordability of housing market? If the housing supply doesn’t increase, the people who can afford the monthly payment of the original 300,000 dollar house will likely to buy the same kind of house. What will be the new housing price if monthly payment is the same at the level when interest rate was at 7% and down payment is 25% of the housing price? What is the new down payment? Who will benefit from the low interest rate environment? Over the long term, will the government policy alone improve or deteriorate the affordability of housing market?

Similar presentations

>")