Download presentation

1

Pricing Catastrophe Risk: Could CAT Futures Have Coped with Andrew? Stephen P. D’Arcy, FCAS Virginia Grace France Richard W. Gorvett, FCAS Presented at the CAS Spring Meeting Orlando, Florida May, 1999

2

Introduction: Some Definitions Derivative: an instrument whose value is based on the value of another financial instrument Future: an exchange traded contractual arrangement to engage in a transaction at a particular future time Option: the right, but not the obligation, to buy or sell a security at a predetermined price Option Spread: the simultaneous purchase and sale of related options

3

CBOT CAT Insurance Futures Introduced in December, 1992 Quarterly contracts National, Eastern, Midwestern and Western regions Based on ISO paid loss data for 22 insurers, adjusted to industry level, as of 6 months after end of quarter Perils included: Wind Hail Earthquake Riot Flood Settlement value Loss Ratio x $25,000 ($50,000 cap)

")

4

Initial CBOT CAT Futures Minimal trading volume developed Reasons: High risk for sellers Buyers not used to futures Marking-to-market Buyer loses money on the future if catastrophes are low Insurance regulatory resistance Newly created index, which may not correspond to catastrophe risk for a particular insurer Reinsurance is available as an alternative

5

PCS Catastrophe Insurance Options Introduced in 1995 Underlying is the PCS Index Nine Geographic Areas National Five Regions Three States Two Sizes Small Cap (up to $20 Billion) Large Cap ($20 to $50 Billion) Development Period to Value PCS Index Six Months Twelve Months

Large Cap ($20 to $50 Billion) Development Period to Value PCS Index Six Months Twelve Months")

6

PCS Catastrophe Index Valuation PCS Loss Index = PCS Estimate/100 Million Value is rounded to one decimal point Example: PCS Loss Estimate = $7,328,340,000 PCS Index = 73.3 Each point is worth $200

7

PCS Option Pricing Example Example of trade on 11/28/97: 50 Western 1998 150 Annual Calls traded at 2.5 ($500) Each option would have been worth $200 for each $100 million of losses in excess of $15 billion. The maximum value of each option is $10,000 ($5 billion/100 million x $200) since this is a small cap option. For a total cost of $25,000, the buyer purchased $500,000 of catastrophe coverage. Since losses in 1998 were well below $15 billion, this option expired worthless.

since this is a small cap option. For a total cost of $25,000, the buyer purchased $500,000 of catastrophe coverage. Since losses in 1998 were well below $15 billion, this option expired worthless..")

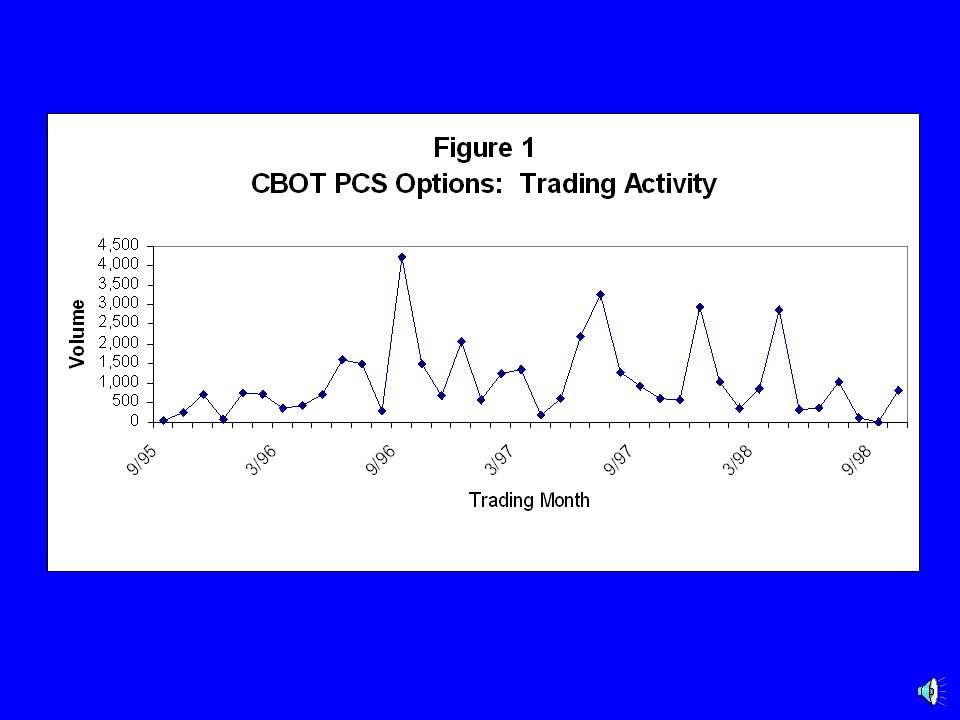

9

Current Status of PCS Options Open Interest 10,682 (as of 5/7/99) Daily Trading Volume: Minimal April 1999:2 Option spreads March 1999:No trades February 1999:1 Option spread Typical Trade: Option Spreads Buyer purchases the lower strike price option and simultaneously sells the higher strike price option.

Daily Trading Volume: Minimal April 1999:2 Option spreads March 1999:No trades February 1999:1 Option spread Typical Trade: Option Spreads Buyer purchases the lower strike price option and simultaneously sells the higher strike price option.")

10

Problems with the PCS Options Large Bid/Ask Spreads Example (5/7/99) National Annual 40/60 Call Spread for 1999 Bid15.0 Ask19.0 Low Liquidity

National Annual 40/60 Call Spread for 1999 Bid15.0 Ask19.0 Low Liquidity")

11

Additional Sources of Information on PCS Options Business Insurance provides prices and trading volume (inside last page) CBOT provides market information: http://www.cbot.com/mplex/quotes/setl/pcscl s.htm

CBOT provides market information: s.htm")

12

The Clearinghouse Guarantee Designed to deal with large, volatile positions and high volume of trade Performance guarantee (“margin”) Guarantee against counterparty default required of both buyer and seller Margin must be very liquid, kept where clearinghouse has immediate access

Guarantee against counterparty default required of both buyer and seller Margin must be very liquid, kept where clearinghouse has immediate access")

13

Marking to Market Positions revalued (“marked to market”) daily based on settlement prices (market value at close) Position losses are transferred out of margin account daily, gains transferred in Keeps stakes low; only need margin for a day or so In event of default, margin account is available to mitigate loss

daily based on settlement prices (market value at close) Position losses are transferred out of margin account daily, gains transferred in Keeps stakes low; only need margin for a day or so In event of default, margin account is available to mitigate loss")

14

Structure of the Clearing System

15

Contract drops in value by $1000

16

A Margin Call If the balance left in the margin account is too low, the broker will issue a margin call If the customer does not immediately bring the margin account back up to an acceptable level, the broker can close out the position If the amount owed is less than the margin account balance, the rest is returned If more is owed, the broker makes up the difference himself

17

Default scenario #1

18

Price Limit Moves Trading is only permitted at prices within a set range around last day’s close If a major piece of news hits the market, the equilibrium price may be outside that band, and trading stops at the top or bottom of the range, which becomes the new close The next day, trading can resume, within a set range around that new close

19

Price Limit Moves and Margin If the new equilibrium price is much higher, price limits moves can happen several days in a row, with price jumping by the limit each day, but no trading This may make it hard for a broker to close a potentially defaulting customer’s position Therefore, margin usually covers more than a normal market move

21

Default scenario #2

22

Clearinghouse Guarantee Clearinghouse guarantees payments only between clearing firms Segregation of customer funds helps to protect customers from their clearing firm’s house account losses Customers may lose in rare cases if the money owed them does not pass through clearinghouse

23

Default scenario #3

24

Clearinghouse Guarantee Clearinghouse will guarantee full payment between clearing firms If margin is exhausted, the clearinghouse can use other components of the guarantee: clearinghouse capital, defaulter’s exchange seats, clearinghouse guarantee funds,… No clearinghouse has ever defaulted, even during the Crash of 1987 (or 1929)...

...")

25

Default scenario #4

26

Clearinghouse Guarantee Clearinghouse monitors firms carefully Looks for large positions Watches firm capital relative to capital requirements Margin is increased if markets show higher volatility Margin will cover a price move of several standard deviations

27

Other benefits of system Simplifies bookkeeping: track position relative to clearinghouse, not with each counterparty Daily marking to market makes losses obvious to all Effectively improves the credit worthiness of the group

29

Hurricane Andrew Hit on August 24, 1992 Pre-Andrew price of National CAT future: $2500 Price immediately after Andrew: $12,000 Limit moves likely for at least 8 days - No trading Final price of National CAT contract: $24,800 Sellers loss: $22,300 per contract 1,652% of initial margin of $1350 Capital supporting exchange guarantees: Under $500 million Insured losses from Andrew: $16 billion

30

Could CAT Futures Have Coped with Andrew? Probably not, if CAT futures had been used to cover a significant share of catastrophe losses.

31

Alternative Approaches to Dealing with Catastrophe Risk Institutional Approaches Managing loss exposures Catastrophe pools Aggregate limit policies for property coverage Strategic use of subsidiaries Adding a hurricane exclusion Capital Market Next presentation

32

Aggregate Limit Policies for Property Coverage Aggregate limits on liability policies Problem of multiple related occurrences Used in CGL, products and professional liability Differences in property aggregate Multiple policies and policyholders Timing of claim payment Advantages Limited coverage from a solvent insurer is better than “full coverage” from an insolvent one Solves availability issue Lower cost of coverage Informs customers of coverage limitations

1 Risk Management in Financial Institutions (II): Hedging with Financial Derivatives Forwards Futures Options.>")