Download presentation

Presentation is loading. Please wait.

1

McGraw-Hill/Irwin Copyright © 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Making Capital Investment Decisions: Incremental Cash Flows Module 3.1

2

6-1 6.1 Incremental Cash Flows Cash flows matter—not accounting earnings. Incremental cash flows matter. Changes in revenues, expenses, taxes, any cash flow as a result of the decision to invest. Opportunity costs matter (if it effects cash flows). Side effects like cannibalism and erosion matter. Taxes matter: we want incremental after-tax cash flows. Sunk costs do not matter. Sunk costs are expenses already paid

. Side effects like cannibalism and erosion matter. Taxes matter: we want incremental after-tax cash flows. Sunk costs do not matter. Sunk costs are expenses already paid.")

3

6-2 Cash Flows—Not Accounting Income Consider depreciation expense. Firms (nor yourself) ever write a check made out to “depreciation.” Much of the work in evaluating a project lies in taking accounting numbers and converting them to cash flows.

ever write a check made out to depreciation. Much of the work in evaluating a project lies in taking accounting numbers and converting them to cash flows..")

4

6-3 Incremental Cash Flows Sunk costs are not relevant Just because “we have come this far” does not mean that we should continue to throw good money after bad. Opportunity costs do matter. Just because a project has a positive NPV, that does not mean that it should also have automatic acceptance. Specifically, if another project with a higher NPV would have to be passed up, then we should not proceed.

5

6-4 Incremental Cash Flows Side effects (“externalities”) matter. If our new product causes existing customers to demand less of our current products, we need to recognize that. If, however, synergies result that create increased demand of existing products, we also need to recognize that.

6

6-5 Estimating Cash Flows Cash Flow from Operations OCF = EBIT – Taxes + Depreciation Net Capital Spending Do not forget salvage value (after tax, of course). Changes in Net Working Capital For example, new projects often require an upfront investment in inventory. When the project winds down, we enjoy a return of net working capital (assuming all inventory sold).

..")

7

6-6 Interest Expense Later chapters will deal with the impact that the amount of debt that a firm has in its capital structure has on firm value. For now, it is enough to assume that the firm’s level of debt (and, hence, interest expense) is independent of the project at hand. It is being handled through the firm’s discount rate

is independent of the project at hand. It is being handled through the firm’s discount rate.")

8

McGraw-Hill/Irwin Copyright © 2013 by The McGraw-Hill Companies, Inc. All rights reserved. “Shark” example 9-7

9

6-8 Shark Attractant Project Estimated sales50,000 cans Sales Price per can$4.00 Cost per can$2.50 Estimated life3 years Fixed costs$12,000/year Initial equipment cost$90,000 100% depreciated straight-line over 3 year life Investment in NWC$20,000 Tax rate34% Cost of capital20% 9-8

10

6-9 Pro Forma Income Statement Sales (50,000 units at $4.00/unit)$200,000 - Variable Costs ($2.50/unit)125,000 Gross profit$ 75,000 - Fixed costs12,000 - Depreciation ($90,000 / 3)30,000 EBIT$ 33,000 - Taxes (34%)11,220 Net Income$ 21,780 9-9 OCF = NI + Dep = 21,780+30,000 = 51,780

$200,000 - Variable Costs ($2.50/unit)125,000 Gross profit$ 75,000 - Fixed costs12,000 - Depreciation ($90,000 / 3)30,000 EBIT$ 33,000 - Taxes (34%)11,220 Net Income$ 21, OCF = NI + Dep = 21,780+30,000 = 51,780")

11

6-10 Projected Total Cash Flows Year 0123 OCF$51,780 NWC -$20,00020,000 Capital Spending -$90,000 IATCF-$110,00$51,780 $71,780 9-10 Note:Investment in NWC is recovered in final year Equipment cost is a cash outflow in year 0

12

6-11 Shark Attractant NPV and IRR 9-11 OCF = EBIT + Depreciation – Taxes OCF = Net Income + Depreciation (if no interest) Outside of taxes

Outside of taxes")

13

McGraw-Hill/Irwin Copyright © 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Some ugly details: OCF, Depreciation, Salvage, and NWC 9-12

14

6-13 The Tax Shield Approach to OCF A common approach (see equation 6.7) OCF = (Sales – costs)(1 – T) + Dep*T OCF=(200,000-137,000) x.66 + (30,000 x.34) OCF = 51,780 OCF = after-tax operating income + tax shield OR, the same equation rearranged: OCF = (Sales – costs – Dep)(1 – T) + Dep 9-13

OCF = (Sales – costs)(1 – T) + Dep*T OCF=(200, ,000) x.66 + (30,000 x.34) OCF = 51,780 OCF = after-tax operating income + tax shield OR, the same equation rearranged: OCF = (Sales – costs – Dep)(1 – T) + Dep 9-13")

15

6-14 Changes in NWC GAAP requirements: Sales recorded when made, not when cash is received Cash in = Sales - ΔAR Cost of goods sold recorded when the corresponding sales are made, whether suppliers paid yet or not Cash out = COGS - ΔAP Buy inventory/materials to support sales before any cash collected is an investment in Net Working Capital 9-14

16

6-15 Depreciation & Capital Budgeting In practice, firm’s use the most advantageous depreciation schedule allowed by the IRS. In this class, we will pretty much stick to good simple ‘straight-line’ depreciation. Depreciation is a non-cash expense Only relevant because of tax affects Depreciation tax shield = D*T 9-15

17

6-16 Computing Depreciation Straight-line depreciation D = (Initial cost – salvage) / number of years Straight Line depreciate Salvage Value but sometimes market value is not equal to expected salvage value, in which case there is a taxable event when the asset is sold. MACRS Depreciate 0 Recovery Period = Class Life Multiply percentage in table by the initial cost 9-16

18

6-17 After-Tax Salvage If the salvage value is different from the book value of the asset, then there is a tax effect Book value = initial cost – accumulated depreciation After-tax salvage or “Net Salvage Cash Flow” = salvage – T(salvage – book value) 9-17

9-17")

19

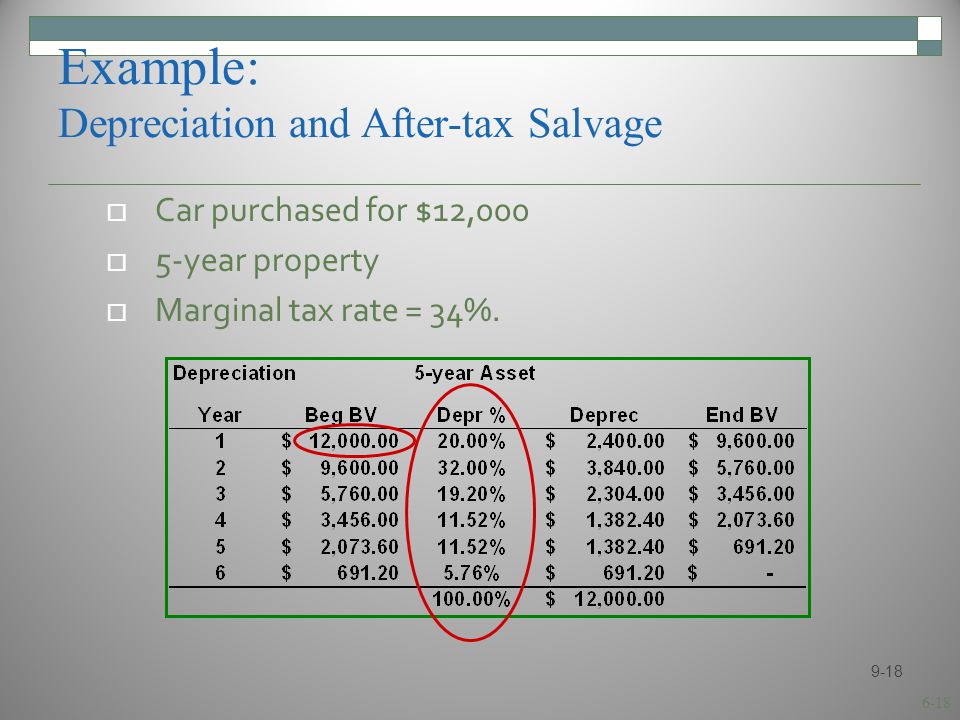

6-18 Example: Depreciation and After-tax Salvage Car purchased for $12,000 5-year property Marginal tax rate = 34%. 9-18

20

6-19 Salvage Value & Tax Effects 9-19 Net Salvage Cash Flow = SP - (SP-BV)(T) If sold at EOY 5 for $3,000: Net Salvage Cash Flow = 3,000 - (3000 - 691.20)(.34) = $2,215.01 = $3,000 – 784.99 = $2,215.01 If sold at EOY 2 for $4,000: Net Salvage Cash Flow = 4,000 - (4000 - 5,760)(.34) = $4,598.40 = $4,000 – (-598.40) = $4,598.40

(T) If sold at EOY 5 for $3,000: Net Salvage Cash Flow = 3,000 - ( )(.34) = $2, = $3,000 – = $2, If sold at EOY 2 for $4,000: Net Salvage Cash Flow = 4,000 - ( ,760)(.34) = $4, = $4,000 – ( ) = $4,598.40")

21

6-20 Some examples over the next few slides Base Inc Starts as a very straightforward example Then incorporates some breakeven analysis on the tax rate Ohio Forge – just a small twist Nike Ballet – some complexities added

22

6-21 Base Inc Base Inc is considering an investment that should increase sales by $5.5 million per year for 10 years, and increase operating costs by $4.5 million per year for 10 years, as they will hire more people. The investment costs $5 million and will be depreciated straight-line to it’s zero salvage value over 10 years. Should they invest if r=10% APR, their tax rate is 25%, and there are no NWC adjustments? 9-21

23

6-22 Base Inc NPV calculation Cash flows Dep = 5/10 = 0.5 million / year CF = (5.5-4.5)(1-.25) +.25(0.5) = 1.0+0.125 = 1.625 m/year NPV = 1.125/.1(1 – 1/(1.1) 10 ) – 5 NPV = 6.9125-5 = +1.9125 NPV>0, therefore, accept the investment 9-22

(1-.25) +.25(0.5) = = m/year NPV = 1.125/.1(1 – 1/(1.1) 10 ) – 5 NPV = = NPV>0, therefore, accept the investment 9-22")

24

6-23 Base Inc (a tax question) What tax rate would make the investment unacceptable? Need to find the tax rate that yields an annual relevant incremental after tax cash flow such that PV of benefits = PV of costs Step 1: Find the relevant cash flow Step 2: Find the tax rate 9-23

25

6-24 Base Inc (a tax question) Find relevant cash flow with PV ann = 5 5 = CF/.1(1 – 1/(1.1) 10 ) 5 = CF(6.1445) CF = 0.8137 million Find tax rate that produces 0.8137 million CF 0.8137= (5.5-4.5)(1-tax) +.tax(0.5) 0.8137= 1– tax + 0.5tax = 1-0.5tax tax = (0.8137-1) / -0.5 tax = 0.3726 or 37.26% Illustrates the “supply side” argument that raising taxes reduces investment (and jobs). In this case, if the firm faced a tax rate of 37.26% or higher, they should not invest. 9-24

26

6-25 Base Inc (note on subsidies) Note: if we found that an NPV would only be positive with a tax rate < 0, then it would require a “tax subsidy” in order to make the investment worthwhile (See “green” industry at- large today). It is not surprising that many firms negotiate state and local taxes, as well as straight cash grants. For example: http://news.yahoo.com/judge-eyes-challenge-delaware- bloom-154744849.html http://news.yahoo.com/judge-eyes-challenge-delaware- bloom-154744849.html “To persuade Bloom Energy to build a manufacturing facility at a former Chrysler plant in Newark, DE, the Markell administration offered the company up to $16.5 million in strategic fund grants. It also offered the University of Delaware, which owns the site, $7 million to make it ready for Bloom's factory.” 9-25

Similar presentations