Download presentation

Presentation is loading. Please wait.

1

Cash Management Cash Cycle

Factors that influence the desired level of cash Optimal cash inventories Short-term investment strategies

2

Managing an entity’s Resources

The Manager Life cycle effects, Business cycle, public events, etc. Resource Decisions Cash Management Inventory Management Working Capital Management Investment in Human Capital Long-term Assets Accounts Receivable Investment Decisions Operating Decisions Recruitment, Selection Training, Productivity Performance Appraisal Compensation Unions & Labor Relations Cash Inflows Human Resources Decisions Value Creation Economics of Information Database Management Data Modeling IS Planning & Development Information Decisions Discount Rate Cost of Capital Financial Markets Financing Decisions Debt vs. Tax Financing

3

Overview ST fin’l planning = deals w/ short-lived assets and liabilities (working capital management); concerned w/ 1) size of investment in CA like cash, A/R, Inventory…a tool is cash budget analysis and 2) how to finance ST assets…a tool is performing credit analysis

size of investment in CA like cash, A/R, Inventory…a tool is cash budget analysis and 2) how to finance ST assets…a tool is performing credit analysis.")

4

Managing WC involves determing:

How much to invest in CA? - CA vs. FA - Nature of activities/programs In each CA? - Cash, A/R, Inventory - Cash Mgt - A/R is Credit Mgt - Inv = POM & Cash balance models

5

Our objectives Learn about the Cash Cycle

Understand the factors that influence the desired level of cash Learn two models that calculate the optimal level of cash Gain an overview of what factors/areas are inputs to a cash budget and how they affect the cash balance

6

Objectives of Public Money Managers

Bringing the entity’s cash resources within control Achieving optimum conservation and utilization of the funds

7

Key areas of Public Cash Management

Organization Collection and disbursement of funds Netting of interagency payments Investment of excess funds Optimal level of cash balances Cash planning and budgeting Bank relations

8

Treasury Management of Cash Balances

Operate with smaller amount of cash Supervision is centralized Better service from banks Proper allocation of funds

9

How much cash should a organization keep on hand?

Enough cash to make payments when needed. (transactions motive) (Daily or Weekly Cash Budget helpful) Additional cash may be held for unexpected requirements. (precautionary motive)

(Daily or Weekly Cash Budget helpful) Additional cash may be held for unexpected requirements. (precautionary motive)")

10

The size of the minimum cash balance depends on:

How quickly and cheaply a organization can raise cash when needed. How accurately managers can predict cash requirements. (Cash Budget helpful) How much precautionary cash the managers need for emergencies.

How much precautionary cash the managers need for emergencies.")

11

The organization’s maximum cash balance depends on:

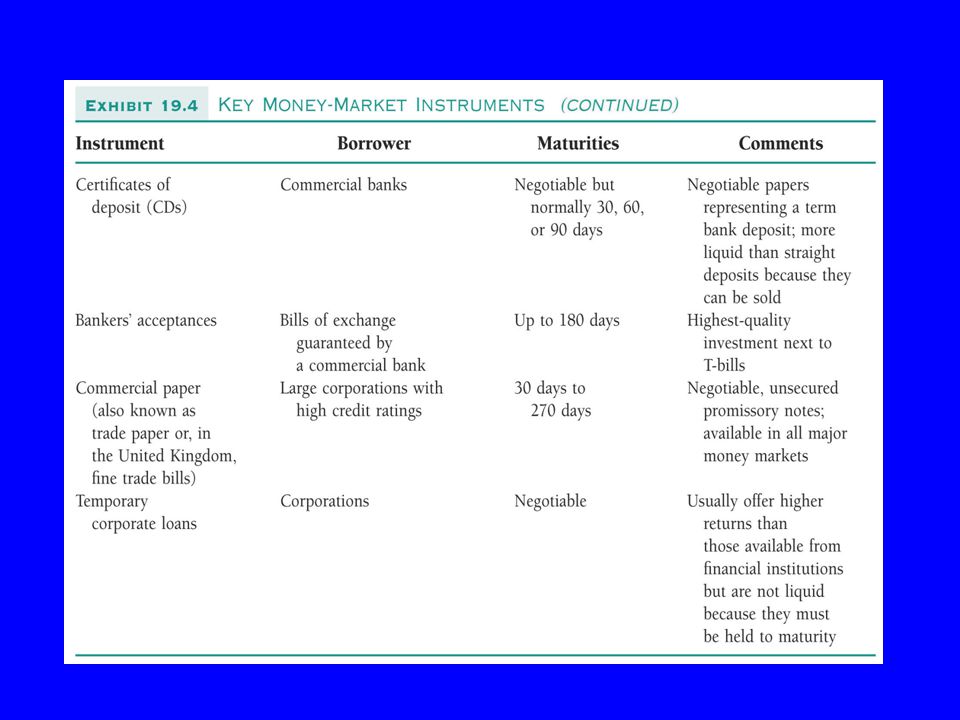

Available (short-term) investment opportunities e.g. money market funds, CDs, commercial paper Expected return on investment opportunities. e.g. If expected returns are high, organizations should be quick to invest excess cash Transaction cost of withdrawing cash and making an investment Demand for Cash for daily transactions (Cash Budget helpful)

investment opportunities. e.g. money market funds, CDs, commercial paper. Expected return on investment opportunities. e.g. If expected returns are high, organizations should be quick to invest excess cash. Transaction cost of withdrawing cash and making an investment. Demand for Cash for daily transactions. (Cash Budget helpful)")

12

Consider Cash an ‘Inventory’

An inventory approach to Cash Balance decisions: the trade-offs: - hold little cash = invest remainder in M/S to earn interest Grantsville has a daily demand for cash of $10,000. Grantsville’s treasurer invests excess cash in the state investment pool that earns .01% per day. In order to transfer funds from the state pool, Grantsville must pay a transaction cost of $20. How much cash should it transfer when it runs out. (Grantsville can complete the cash transfer electronically so it waits until the cash balance is zero). - if hold too little cash = incur transactions costs to meet cash needs - hold lots of cash = forgo investing in M/S and earning interest

. - if hold too little cash = incur transactions costs to meet cash needs. - hold lots of cash = forgo investing in M/S and earning interest.")

13

Optimal Cash Balance via Baumol Model

r = .01% .0001 TC = $20 Cost ($) Z*= [(2M*TC)/r] Z* Total Costs Z = $63,246 Holding Costs: (Z/2)*r Order Costs:(M/Z)*TC Z* Order Quantity (Z)

Z*= [(2M*TC)/r] Z* Total Costs. Z = $63,246. Holding Costs: (Z/2)*r. Order Costs:(M/Z)*TC. Z* Order Quantity (Z)")

14

Problems with the Baumol Model

Cash flows may not be very predictable, much less constant Treasurers may want a ‘safety stock’ of cash

15

The Miller - Orr Model The Miller-Orr Model provides a formula for determining the optimum cash balance (Z), the point at which to sell securities to raise cash (lower limit L) and when to invest excess cash by buying securities and lowering cash holdings (upper limit H). Depends on: transaction costs of buying or selling securities variability of daily cash (incorporates uncertainty) return on short-term investments

, the point at which to sell securities to raise cash (lower limit L) and when to invest excess cash by buying securities and lowering cash holdings (upper limit H). Depends on: transaction costs of buying or selling securities. variability of daily cash (incorporates uncertainty) return on short-term investments.")

16

The Miller - Orr Model H Z L Buy Securities Upper Limit

Dollars in the Cash Account Z L Lower Limit Sell Securities Days of the Month

17

The Miller-Orr Model - Target Cash Balance (Z)

3 3 x TC x V 4 x r Z = L where: TC = transaction cost of buying or selling securities V = variance of daily cash flows r = daily return on short-term investments L = minimum cash requirement

18

The Miller-Orr Model - Target Cash Balance (Z)

Example: Suppose that short-term securities yield 5% per year and it costs the organization $50 each time it buys or sells securities (TC). The daily variance of cash flows is $1000 (V) and your bank requires $1,000 minimum checking account balance (L).* 3 Z = $1,000 = $3,000 + $1,000 = $4,000 3 x 50 x 1000 4 x .05/360

. The daily variance of cash flows is $1000 (V) and your bank requires $1,000 minimum checking account balance (L).* 3. Z = + $1,000. = $3,000 + $1,000 = $4, x 50 x x .05/360.")

19

The Miller-Orr Model - Upper Limit

The upper limit for the cash account (H) is determined by the equation: H = 3Z - 2L where: Z = Target cash balance L = Lower limit In the previous example: H = 3 ($4,000) - 2($1,000) = $10,000

is determined by the equation: H = 3Z - 2L where: Z = Target cash balance L = Lower limit. In the previous example: H = 3 ($4,000) - 2($1,000) = $10,000.")

20

The Miller - Orr Model Buy Securities Upper Limit

$10,000 Dollars in the Cash Account $4000 $1000 Lower Limit Sell Securities Days of the Month

21

Cash Pooling Centralized cash management involves transfer

of an agency’s cash in excess of minimal operating requirements into a centrally managed account also known as a cash pool. Procedure and Benefits

22

Investment of excess funds

24

The Collection & Disbursement of Public Funds

Managing Cash Balances Safety Liquidity Maximize pool of funds available for investment Concentration Accounts Zero-balance accounts Highest yield Controlling Cash Collection & Disbursement Dual responsibility Receipts maintained in a location separate from cash & checks Certification of vouchers

25

Collection of funds Need for accelerating collections

How to accelerate collection of receivables

26

Disbursement of funds Importance of disbursement of funds

Review of disbursements Payment instruments being used (checks, drafts, wire transfers, etc.) Bank charges and internal costs Techniques being used Time involved for processing of instruments

Bank charges and internal costs. Techniques being used. Time involved for processing of instruments.")

27

Payments Netting in Public Cash Management

Need for payments netting Procedure involved Only netted amount is transferred (bilateral netting) Netting center (multilateral netting)

Netting center (multilateral netting)")

28

Our objectives Learn about the Cash Cycle

Understand the factors that influence the desired level of cash Learn two models that calculate the optimal level of cash Gain an overview of what factors/areas are inputs to a cash budget and how they affect the cash balance

29

Stop Here

30

Payments netting in Public Cash Management (contd.)

")

31

Payments Netting in Public Cash Management (contd.)

")

32

Cash Planning and Budgeting

33

Cash Planning and Budgeting (contd.)

")

Similar presentations

.>")