Download presentation

Presentation is loading. Please wait.

1

Realities at Retail Gil Brechtel President and Chief Executive Officer Magnet

2

Realities at Retail Magazine Information Network (MagNet) Owned by the major US wholesalers Recognized as the newsstand industry’s only central data repository Capture US and Canadian wholesalers’ store level allocation, sales and return information at least weekly 125,000 retailer accounts and 8,000 titles Receive retailer Point of Sale information daily or weekly from retailers and wholesalers Provide data and consultancy services to publishers and national distributors Newsstand Industry Historical Sales Perspective - 2003-2007 Wholesaler competition started in 1995 Significant margin shift from wholesalers to retailers Most smaller players exited the business and four major wholesalers dominated servicing large geographical areas with regional distribution centers Wholesalers put more pressure on publishers for discounts Reduced service and overhead costs in an attempt to maintain profit levels Despite all of the cost cutting, sales actually increased between 2003 and 2007

Owned by the major US wholesalers Recognized as the newsstand industry’s only central data repository Capture US and Canadian wholesalers’ store level allocation, sales and return information at least weekly 125,000 retailer accounts and 8,000 titles Receive retailer Point of Sale information daily or weekly from retailers and wholesalers Provide data and consultancy services to publishers and national distributors Newsstand Industry Historical Sales Perspective Wholesaler competition started in 1995 Significant margin shift from wholesalers to retailers Most smaller players exited the business and four major wholesalers dominated servicing large geographical areas with regional distribution centers Wholesalers put more pressure on publishers for discounts Reduced service and overhead costs in an attempt to maintain profit levels Despite all of the cost cutting, sales actually increased between 2003 and 2007")

3

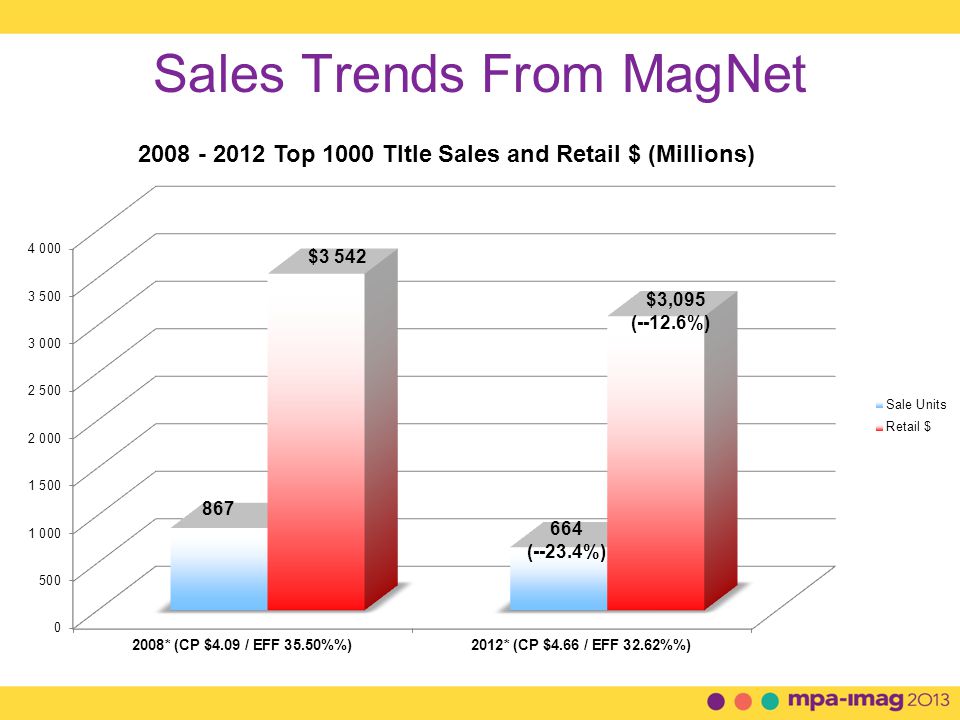

Sales Trends From MagNet

4

Newsstand Industry Historical Sales Perspective - 2008-2012 The economy tanked in early in 2008 bringing magazines sales with it The sales decline continued through the end of 2012 Celebrity and newsweekly title sales losses a major contributing factor Celebrity title information and major news stories available to consumers in real time through social and digital media Small titles ceased publishing, dropped by wholesalers or left newsstand Technological advances, social media and mobile affected newsstand sales iPad - Release in early 2010 provided another platform to receive content Facebook - 400 million users in 2010, now 1.1 billion, 665 million every day Smart phones - Represent 55% of US mobile phone use– 130 million people Kroger Supermarkets reduced average customer checkout wait time in 2,400 stores from 4 minutes to 26 seconds using infrared cameras and technology Wal-Mart testing “Scan & Go” system in 200 stores Customers scan barcodes of products they are buying and bag them as they shop Self checkout screen reads barcodes and prompts customer to pay Realities at Retail

5

Sales Trends From MagNet

10

Largest quarterly sales decline compared to same period previous year in memory Top 50 titles and titles ranked lower than 1000 in sales contributed 97% of the sales loss – $96M Titles ranked 50-1000, over 50% of the business collectively performed fairly well Contributing factors: Continual high unemployment along with tax increases at the beginning of 2013 22 million unemployed or “underemployed Americans” May, 2013 4-6% reduction in take home pay effective January 1, 2013 Consumers have less discretionary income Many major weekly titles had 12 issues in 2013 compared to 13 in 2012 975 fewer releases in the first quarter this year – 6.3% less than 2012 Mainly non-weekly titles no longer on the newsstand or cutting frequencies Non-weekly title sales flat much of the third and fourth quarter last year Competition from new media for content delivery and consumers’ leisure time Realities at Retail

11

Newsstand sales environment has impacted the supply chain Many publishers have stopped publishing titles or moved only to digital format Retailers cutting back on space as sales decline Realities at Retail

12

Top Chains Share of Market 2012 RankChain HQ2008 $2012 $$ Var 1Wal Mart Stores/HQ$659$498-24.3% 2Barnes & Noble Inc HQ$261$227-12.8% 3Kroger Co/HQ$236$177-25.1% 4CVS/Caremark Corp$158$122-22.6% 5Safeway Inc/HQ$162$116-28.8% Top 5 Sub-total$1,476$1,141-22.7% ROM$3,358$2,286-31.9% Total$4,834$3,427-29.1%

13

Newsstand sales environment has impacted the supply chain Many publishers have stopped publishing titles or moved only to digital format Retailers cutting back on space as sales decline Wholesalers with high fixed costs explore other opportunities to increase sales as financial losses continue Retailer demands for SBT has impacted their cash flow positions Anderson News Company, the largest magazine wholesaler closed its doors in early 2009, creating a vacuum while other wholesalers attempted to service the effected retailers Many small retail accounts stopped handling magazines as they couldn’t get service Major Southern wholesaler on shaky financial footing Wholesalers not really interested in expanding marketshare in current environment So are printed magazines and newsstand sales really dead or on life support? Currently, 75% of consumers still prefer to read magazines in print – Deloitte’s 2013 Consumer Media Survey 88% last year 78% of consumer magazine publishers’ revenue derived from print – MediaWeek Current consensus of opinion is that print is more profitable than digital and newsstand is more profitable than subscriptions Realities at Retail

14

A deeper dive into the numbers shows that many titles are prospering in this tough newsstand environment Both specials and regular frequency titles Realities at Retail So if print is dead why are consumers spending so much on high cover priced newsstand only products? No subscriptions Little or no advertising and no rate base to meet Brands sell – Time, Life, Us, Meredith, Taste of Home usually successful High quality cover and paper stock and good pagination very important Book-a-zines – high cover priced specials have prospered during the same five year period 20082009201020112012 Retail $ $194,750,000$231,303,000$263,043,000$293,756,400$352,016,000 Units 19,244,00022,134,00022,406,00024,594,00029,102,000 CP $10.12$10.45$11.74$11.94$12.10

15

Top Book-a-zines 2012

16

Book-a-zine Sales Sample 2012 01 Sales360,300 Dealers50,700 Retail $ (000’s) $3,368 Index+130% US Price$9.99 2013 35 Sales203,600 Dealers53,300 Retail $ (000’s) $2,468 Index+120% US Price$11.99 2012 16 Sales195,800 Dealers46,600 Retail $ (000’s) $2,018 Index+64% US Price$9.99 2012 28 Sales191,300 Dealers49,500 Retail $ (000’s) $2,529 Index+164% US Price$12.99

$3,368 Index+130% US Price$ Sales203,600 Dealers53,300 Retail $ (000’s) $2,468 Index+120% US Price$ Sales195,800 Dealers46,600 Retail $ (000’s) $2,018 Index+64% US Price$ Sales191,300 Dealers49,500 Retail $ (000’s) $2,529 Index+164% US Price$12.99")

17

Sales Increases in Quarter 1, 2013 2012 12 Retail $+23% 2012 12 Retail $+51% 2012 12 Retail $+24%

18

Sales Increases in Quarter 1, 2013 2013 01 Retail $+6% 2013 01 Retail $+11% 2013 01 Retail $+9%

19

Sales Increases in Quarter 1, 2013 2013 02 Retail $+15% 2013 02 Retail $+46% 2013 02 Retail $+5%

20

Distribution And Expansion Works 2012 10 Draw+73% Retail $+67% Dealers+55% 2012 08 Draw+86% Retail $+105% Dealers+18% 2012 10 Draw12% Retail $+34% Dealers+11%

21

Distribution and Expansion Works 2012 10 Draw+23% Retail $+56% Dealers+25% 2013 02 Draw+136% Retail $+384% Dealers+60% 2012 21 Draw29% Retail $+257% Dealers+13%

22

Secrets to newsstand success: Be proactive – Don’t give up on the newsstand Work with your distributor or consultant to look for opportunities for dealer expansion and sales Insist that your title’s distributions are worked more that a few times per year You can increase your newsstand profitability by reducing your newsstand production and distribution costs without a sales loss Produce titles that pique consumer’s interest to beat the competition for the consumers’ dollars in a tough economy Consumer’s perceived value of the publication is very important Newsstand is the only place in the magazine world where the consumer must decide in a very short time period whether or not they are getting the “bang for the buck” with their purchase With fewer advertising pages and current cover prices, too many titles are failing the “Thud Factor” test Newsstand can be your most profitable source of revenues, but you have to work at it! Realities at Retail

23

Thank You For Your Attention

Similar presentations

Geometry (29%)>")