Download presentation

Presentation is loading. Please wait.

1

www.vsnlinternational.com Evolution of transoceanic lambdas A GLIF capacity supplier perspective 23th APAN meeting Manila, January 22-26th 2007 Yves Poppe, Director Business development, IP Services

2

www.vsnlinternational.com VSNL International | Member of the Tata Group Tata Group 125-year old largest private sector group $17.6 billion in revenues Acquired VSNL in February 2002 VSNL acquired Tyco in Nov 2004 VSNL acquired Teleglobe in Feb 2006 Tata Consultancy Services (TCS) Asia’s largest software & systems integration services company 33 countries across 5 continents Key player in high-growth international markets VSNLTata Teleservices 46% 100% VSNL International 100%

Asia’s largest software & systems integration services company 33 countries across 5 continents Key player in high-growth international markets VSNLTata Teleservices 46% 100% VSNL International 100%")

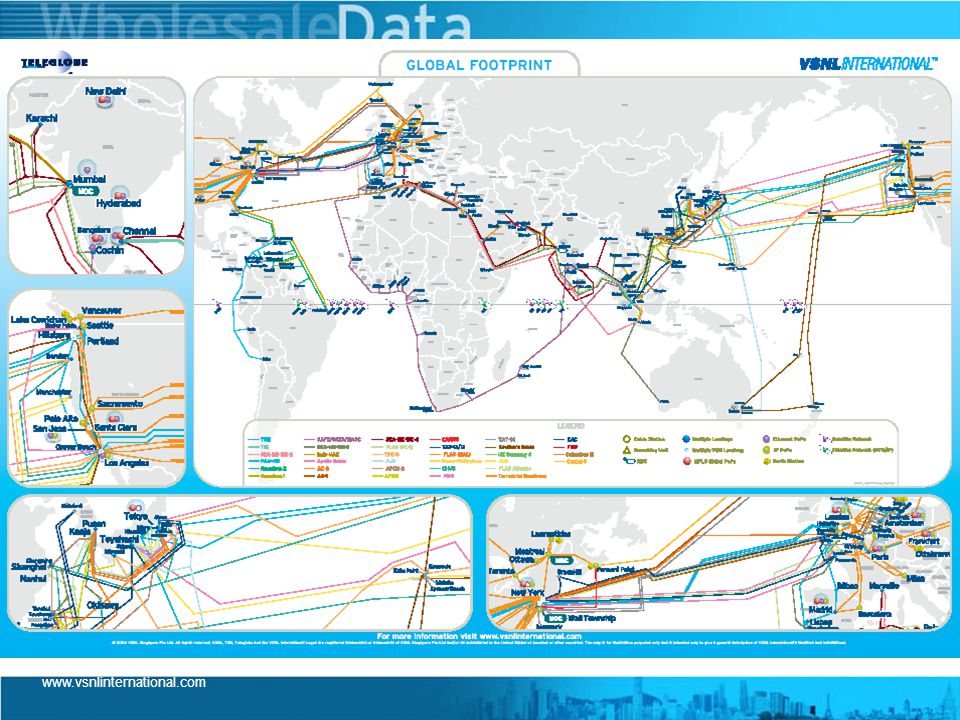

3

www.vsnlinternational.com

4

Global Lambda Integrated Facility - Pacific Source: http://www.glif.is/ VSNL GTS

5

www.vsnlinternational.com Global Lambda Integrated Facility – Atlantic VSNL GTS Source: http://www.glif.is/

6

www.vsnlinternational.com VSNL International : historical lambda provider to the R&E Feb 1995: Teleglobe provides the first NGI connection for the Brussels G7 Summit:: 155mb Teleglobe donates the capacity for two years to Canarie and co-represents Canada in the GIBN (Global Interopability of Broadband Networks) As member of the Canarie technical advisory Council, Teleglobe encourages the creation of Starlight in Chicago. 2001: Teleglobe sets up the first transoceanic lambda linking Surfnet to Starlight at 2.5 gbps First lambdagrid workshop in Amsterdam 2002: iGrid2002 Amsterdam, Tyco provides a 10gig connection between Netherlight and Abilene in NY through the IEEAF foundation. Level3 provides the second transatlantic link. 2003: creation of GLIF at the third lambdagrid workshop in Reykjavik. Tyco provides the Pacific and Atlantic connectivity for «little Gloriad». Teleglobe had provided the predecessor project Naukanet. November 2004: VSNL acquires Tyco cable networks (GTS) 2005: Gloriad expands with a Tyco/VSNL 10 gbps link between Korea and the US February 2006: VSNL acquires Teleglobe

2005: Gloriad expands with a Tyco/VSNL 10 gbps link between Korea and the US February 2006: VSNL acquires Teleglobe.")

7

www.vsnlinternational.com Turn of the century Atlantic capacity battle Design, lit capacity and RFS design(Gb) lit RFS AC-1 180 180 may 98 Level 3/GC (Project Yellow) 1,280 640 Sep00 TAT-14 (Club) 640 640 Apr01 Hibernia (360networks, Inc.) 2,560 160 Jun01 FLAG Atlantic-1 (FLAG/GTS) 2,400 320 Sep01 Atlantic Crossing -2 (Global Crossing) ** 2,560 1Q01 VSNL transatlantic *** 2,560 460 Jun02 Apollo (C&W) 3,200 640 Feb03 Total 12,820Gbps! ** Cancelled, AC-2 joining Level 3 *** originally Tyco Atlantic, sold to VSNL nov 2004 Lit capacity 2006: 3,020Gb up around 210gig over last 12 months (source: Telegeography 2006)

.")

8

www.vsnlinternational.com Miami London (x2) Hunmanby Highbridge (x2) New York (x2) Wall Township (x2) To Santa Clara To Los Angeles 4 Fiber Pairs per cable; 2 Cables Supports 64 10Gb/s waves per fiber pair Lisbon Madrid Bilbao Paris Frankfurt (x2) Amsterdam Groningen VSNL Atlantic

Hunmanby Highbridge (x2) New York (x2) Wall Township (x2) To Santa Clara To Los Angeles 4 Fiber Pairs per cable; 2 Cables Supports 64 10Gb/s waves per fiber pair Lisbon Madrid Bilbao Paris Frankfurt (x2) Amsterdam Groningen VSNL Atlantic")

9

www.vsnlinternational.com Turn of the century Trans- Pacific capacity build-out Design, lit capacity and RFS design(Gb) lit RFS TPC-5 (club) 20 20 jan 97 Southern Cross 480 240 Nov 00 China-US (club) 80 80 Jan 00 PC-1 (Global Crossing & Marubeni) 640 180 jan 00 Japan-US (club) 640 400 sep 01 VSNL Pacific ** 7,680 640 Jan 03 FP-1 FLAG Pacific *** 5,120 2Q02 360 Pacific *** 4,800 3Q02 Total 9,540Gbps ** = april 01: Tycom joins FLAG aug 01: FLAG withdraws, Tycom continues alone nov 03 : up for sale; nov 04: bought by VSNL ***= project dropped Lit capacity 2006: 1,560 Gb 400 gig lit in last 12 months (Telegeography 2006)

lit RFS TPC-5 (club) jan 97 Southern Cross Nov 00 China-US (club) Jan 00 PC-1 (Global Crossing & Marubeni) jan 00 Japan-US (club) sep 01 VSNL Pacific ** 7, Jan 03 FP-1 FLAG Pacific *** 5,120 2Q02 360 Pacific *** 4,800 3Q02 Total 9,540Gbps ** = april 01: Tycom joins FLAG aug 01: FLAG withdraws, Tycom continues alone nov 03 : up for sale; nov 04: bought by VSNL ***= project dropped Lit capacity 2006: 1,560 Gb 400 gig lit in last 12 months (Telegeography 2006)")

10

www.vsnlinternational.com 8 Fiber Pairs Cable Supports 96 10Gb/s waves per fiber pair Hillsboro (x2) Los Angeles (x2) Seattle Portland Tokyo (x2) Emi Toyohashi Guam 8 Fiber Pairs Per Cable Ring Supports 64 10Gb/s waves per fiber pair City-to-City Connectivity to: Portland Seattle Los Angeles Santa Clara Tokyo 8 Fiber Pairs Cable Supports 96 10Gb/s waves per fiber pair VSNL Pacific Maruyama Santa Clara (x2) To New York

Los Angeles (x2) Seattle Portland Tokyo (x2) Emi Toyohashi Guam 8 Fiber Pairs Per Cable Ring Supports 64 10Gb/s waves per fiber pair City-to-City Connectivity to: Portland Seattle Los Angeles Santa Clara Tokyo 8 Fiber Pairs Cable Supports 96 10Gb/s waves per fiber pair VSNL Pacific Maruyama Santa Clara (x2) To New York")

11

www.vsnlinternational.com New trans-pacific gold rush? 3 major announcements in recent weeks Dec 18th 2006; TransPacific Express (TPE): First China –US cable agreement signed by China Telecom, China Unicom, China Netcom, Chunghwa, Verizon and Korea Telecom US-Qindao and US-Shanghai, branches to Korea and Taiwan 5.12Tb design capacity; 1.28Tb lit initially; 500 million US$, RFS end 2008 Dec 29th 2006: Reliance announces Flag NGN with 4 cables System 1: Asia - India, Malaysia, Singapore, Indonesia, Vietnam, Philippines, Brunei, Hong-Kong System 2: Africa - Kenya, Mozambique, Republic of South Africa, Tanzania, Madagascar, Mauritius System 3: Mediterranean - Greece, Cyprus, Turkey, Malta, Libya, Lebanon System 4: Trans-Pacific - US West Coast, Japan, China and Hong Kong (2009) To be built over next 36 months; 1.28Tb, 1.5 billion $ Jan 15th 2007: Asia Netcom announces EAC Pacific Japan-US Northern route and Philippines-US via Guam and Hawai as Southern route Philippines-Japan to close the ring; 2.56Tb design capacity (4 fiber pairs) ; 636 million $ committed, RFS july 2008 These 3 projects will more than double transpacific capacity when completed!

: First China –US cable agreement signed by China Telecom, China Unicom, China Netcom, Chunghwa, Verizon and Korea Telecom US-Qindao and US-Shanghai, branches to Korea and Taiwan 5.12Tb design capacity; 1.28Tb lit initially; 500 million US$, RFS end 2008 Dec 29th 2006: Reliance announces Flag NGN with 4 cables System 1: Asia - India, Malaysia, Singapore, Indonesia, Vietnam, Philippines, Brunei, Hong-Kong System 2: Africa - Kenya, Mozambique, Republic of South Africa, Tanzania, Madagascar, Mauritius System 3: Mediterranean - Greece, Cyprus, Turkey, Malta, Libya, Lebanon System 4: Trans-Pacific - US West Coast, Japan, China and Hong Kong (2009) To be built over next 36 months; 1.28Tb, 1.5 billion $ Jan 15th 2007: Asia Netcom announces EAC Pacific Japan-US Northern route and Philippines-US via Guam and Hawai as Southern route Philippines-Japan to close the ring; 2.56Tb design capacity (4 fiber pairs) ; 636 million $ committed, RFS july 2008 These 3 projects will more than double transpacific capacity when completed!.")

12

www.vsnlinternational.com Remarkable Central Asian build-out April 2002: RFS for i2i; 8.12Tb capacity; 160Gb lit, 50% Bharti 50% Singtel owned Feb 2004: VSNL and Asia Netcom announce their Tata Indicom cable (TIC) between Chennai and Singapore cable ; RFS was nov 2004 with an initial lit capacity of 320gbps and a design capacity of 5.12Tbps; connects into EAC and on to North America. Oct 2005: BSNL announces India-Sri Lanka cable Dec 2005: Seamewe-4 operational; Sept 2006: Falcon operational March 2006: BSNL and MSNL announce new India-Singapore cable August 2006: VSNL announces new multi-terabit India-Europe cable, RFS mid 2008, named IMEWE and new intra-Asia cable (Singapore-HK-Japan) RFS Q3 2007 « Indian operators now control more than a third of the global undersea cable systems in the world with VSNL being among the top three » The Hindu Business Line, March 6 th 2006

RFS Q « Indian operators now control more than a third of the global undersea cable systems in the world with VSNL being among the top three » The Hindu Business Line, March 6 th")

13

www.vsnlinternational.com Segment 3 ALCATEL FUJITSU ALCATEL AND FUJITSU Segment 1 Segment 2Segment 4 VSNL Network Administrator 16-member Consortium Hosts Mumbai-based network operating center 1.28 Tera bits per second design capacity Connecting 3 continents over 20,000km Initially equipped with 160 Giga bits bandwidth (DWDM technology) 640 Gigabits matrix Digital Cross Connect in every station SMW- 4 | Asia to Europe

640 Gigabits matrix Digital Cross Connect in every station SMW- 4 | Asia to Europe")

14

www.vsnlinternational.com Chandigarh Ambala Karnal Ghaziabad Delhi Gurgaon Jaipur Agra Gwalior Itarsi Bhopal Nagpur Jalgaon Vadodra Bhavnagar Nadiad Surat Nasik Kalyan Aurangabad MUMBAI HYDERABAD Kolhapur Panaji Guntur Rajahmundry Hubli CHENNAI Mysore Salem Erode Thrissur ERNAKULAM TRIVENDRUM Quilon Kottayam Alappuzha Madurai Trichy Thanjavur Vellore MANGALORE Kannur Kozhikode Amritsar Jalandhar Ludhiana Hissar Rohtak Bhatinda Mehsana Ajmer Udaipur Karwar Tuticorin Tirunelvelli Belgaum Vizag Patiala Virudhunagar Lucknow Bareilly Kanpur Allahabad Fatehpur Patna Varanasi Arrah Ranchi Kolkata Cuddalore Rajkot Ahmedabad Nellor e Vijayawada Eluru Satara Sholapur Jamnagar Junagarh Pune Valsad Bharuch Raipur Jaunpur Kachipuram Nagercoil Chapra Cuttack Bhubaneshwar Kharaghpur Chittoor Kolar COIMBATORE Biaora Ujjain Dewas Krishnagiri Hassan Medikeri Tirupati Renigunt a SMW-3 Karaikkudi Davangere Shimoga Chickmagalore Tumkur Srikakulam Warrangal Karimnagar Chandrapur Raipur Jabalpur Bhandara Narsinghpur Seoni Balaghat Bilaspur Mandla Akola Edalabad Khandwa Indore Vidisha Damoh Ambala Karnal Ludhiana Rohtak Patiala Pathankot Hoshiarpur Patna Varanasi Arrah Chapra Meerut Jhansi Chattarpur Panna Rewa Tonk Bhilwara Rewari Faridabad Shivpuri Guna Ratlam Banswara Godhra DhuleBuldana Parbhani Nanded Nizamabad Ahmednagar Osmanabad Gulbarga Bidar Bellary Raichur Mehboobnagar Sangareddy Anantpur BANGALORE Pondicherry Pali Jodhpur Jammu Udhampur Srinagar Shimla Sriganganagar Sikar Churu Muzzanagar Saharanpur Dehradun Farakka Siliguri Bongaigaon Shillong Guwahati Misa Tejpur Itanagar Kohima Imphal Aizawal Agartala Surendranagar Palanpur Raigarh Rourkela Jamshedpur Chittorgarh Owns more than 25,000 route Km of fiber Connecting 200+ cities in India Lighting up multi lambda capacity SDH Routes DWDM Routes Other Carriers VSNL National Indian Fibre Network

15

www.vsnlinternational.com Some final thoughts Back in 1994-1995, the thought of multiple 10 gig waves was distant future. The brand new Cantat-3 cable, lit in october 1994 with 5 gbps design capacity doubled the transatlantic capacity and was supposed to take 17 years to fill! Then came internet! A prediction of cable builds with 1000 times that capacity 5 years later would have been met with ridicule DWDM and unrealistic growth forecasts contributed to the big telecom crash. Major shift in cable-ownership: Asia owns most of the intra-Asia and Transpacific capacity. Current capacity enough for big science projects? Commercial applications for end-to end user controlled light paths? A lambda divide on top of a digital divide? Who would predict it will take 17 years to fill current and currently planned capacity? The next 10 years are bound to bring their share of major surprises. Soliton technology? Petabit level cable capacity?

Similar presentations

>")

, International Telecommunication Union (ITU) Market Forecasting.>")

Future development of Telecoms and Strategic Initiatives of the ITU HKUST, 7 th December 2000 The.>")