Download presentation

Presentation is loading. Please wait.

1

Preliminary Results 12 May 2009 Working together for Greener logistics solutions For period ended 28 February 2009 www.stobartgroup.com

2

Highlights Year of growth, laying foundations for the multimodal strategy Good financial results despite downturn in economy Entering a period of consolidation and organic growth Some operating cashflow will be invested whilst continuing to recognise a return to shareholders Dividend proposed – final 3.3p = total 6.0p – paid 22 June 2009 Board changes Outlook

3

Financial Review Ben Whawell Chief Financial Officer

4

Financial Highlights Results include 11 months of acquired James Irlam and Stobart Rail businesses, 8 months of acquired Innovate business and 3 months of London Southend Airport Revenue £431.1m 11 months of James Irlam and Stobart Rail 8 months of Innovate Chilled £108.8m 2007/2008 Revenue Notes EAFFC £27.5m Normalised comprising the underlying operating profit of £31.4m less fleet financing costs of £3.2m and share based payments of £0.7m £5.4m 2007/2008 EAFFC Notes Earnings after Fleet Financing Costs Profit Before Tax £23.1m Normalised PBT stated before the credit for purchase of London Southend Airport of £3.6m and restructuring costs of £2.7m £3.5m 2007/2008 PBT Notes EPS 7.7p Normalised EPS using continuing earnings before the credit for London Southend Airport of £3.6m, restructuring costs of £2.7m and allowing for a 28% tax charge. 2.3p 2007/2008 EPS Notes Earnings per Ordinary Share from Continuing Operations from continuing operations

5

Other Financial Measures ROCE 9.0% Calculated using underlying PBT. Capital includes all assets less current liabilities excluding financing 11 months of James Irlam and Stobart Rail 8 months of Innovate Chilled 2007/2008 Notes Return on Capital Employed Gearing 29.8% Calculated as net debt (excl. HP finance) divided by equity (excl. HP financed assets) 26.7% 2007/2008 Gearing Notes Net Debt £120.7m Net debt excluding HP is £67.4m £75.2m 2007/2008 Net Debt Notes

divided by equity (excl. HP financed assets) 26.7% 2007/2008 Gearing Notes Net Debt £120.7m Net debt excluding HP is £67.4m £75.2m 2007/2008 Net Debt Notes.")

6

Profit & Loss Account Continuing Operations 28 February 2009 £m 29 February 2008 £m Revenue431.1108.8 Operating expenses (underlying)(399.7)(102.9) Share based payment(0.7)- Finance lease cost(3.2)(0.5) EAFFC (underlying)27.55.4 Finance costs (net)(4.4)(1.9) Profit before tax (underlying)23.13.5 Restructuring costs(2.7)- Credit for business purchase (LSA)3.6- Profit before tax (reported)23.93.5 EPS - basic9.8p2.3p EPS - adjusted7.7p2.1p

(399.7)(102.9) Share based payment(0.7)- Finance lease cost(3.2)(0.5) EAFFC (underlying) Finance costs (net)(4.4)(1.9) Profit before tax (underlying) Restructuring costs(2.7)- Credit for business purchase (LSA)3.6- Profit before tax (reported) EPS - basic9.8p2.3p EPS - adjusted7.7p2.1p")

7

Division performance Note 1 Normalised EAFFC comprising the underlying operating profit less fleet financing costs and share based payments Note 2 Normalised PBT stated before restructuring costs and the credit for purchase of London Southend Airport Note 3 Calculated using underlying PBT. Capital includes all assets less current liabilities excluding financing. 2008/09 Revenue £387.3m PBT 2 (underlying) £22.1m EAFFC 1 £24.5m ROCE 3 10.0% Eddie Stobart 2008/09 Revenue £38.2m PBT 2 (underlying) £3.4m EAFFC 1 £3.5m ROCE 3 29.2% Stobart Rail 2008/09 Revenue £14.6m PBT 2 (underlying) £0.9m EAFFC 1 £2.6m ROCE 3 3.0% Stobart Ports 2008/09 Revenue £1.7m PBT 2 (underlying) £0.1m EAFFC 1 £0.1m ROCE 3 2.0% Stobart Air

£22.1m EAFFC 1 £24.5m ROCE % Eddie Stobart 2008/09 Revenue £38.2m PBT 2 (underlying) £3.4m EAFFC 1 £3.5m ROCE % Stobart Rail 2008/09 Revenue £14.6m PBT 2 (underlying) £0.9m EAFFC 1 £2.6m ROCE 3 3.0% Stobart Ports 2008/09 Revenue £1.7m PBT 2 (underlying) £0.1m EAFFC 1 £0.1m ROCE 3 2.0% Stobart Air.")

8

Discontinued Discontinued loss on investment properties of £29.9m Increase of (£4.8m) since interim date as complete write off of all JV interests and write down of Debden now held for sale Still potential for upside on ultimate disposals

since interim date as complete write off of all JV interests and write down of Debden now held for sale Still potential for upside on ultimate disposals")

9

Acquisitions James Irlam Full integrated at year end. Ahead of expectation PBT £6.9m WA Developments – now Stobart Rail Significantly ahead of expectation PBT £3.5m Innovate – now Stobart Chilled Large restructuring exercise Platform in place for growth PBT £1.1m London Southend Airport Relatively new Long term value and returns proposition PBT £0.1m

10

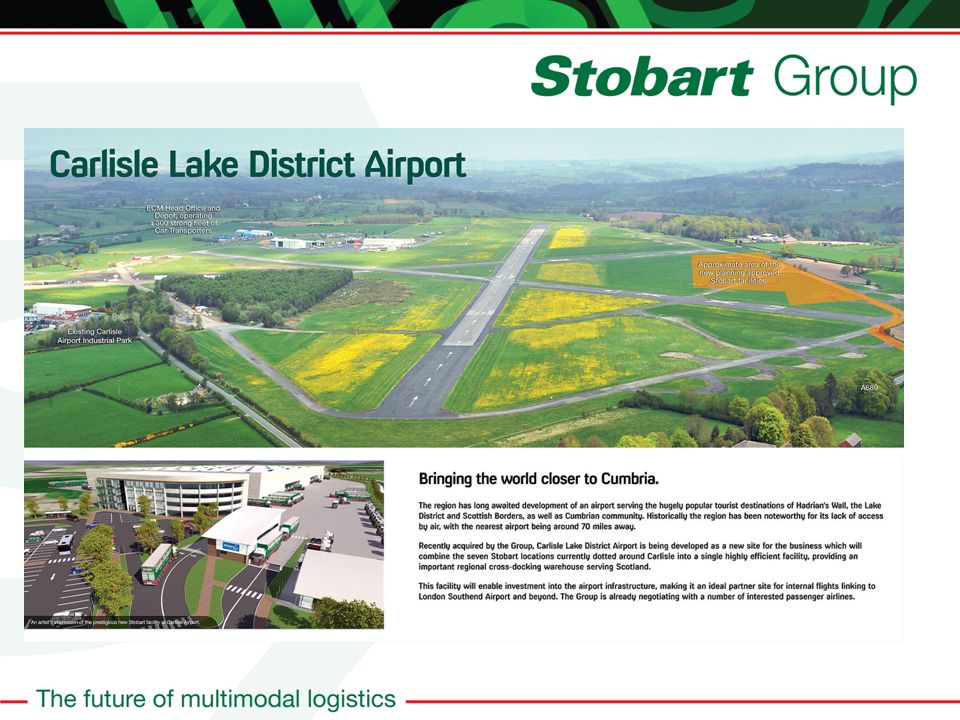

Asset Development Widnes Phase 1 First quarter of site £40m development Key logistics opportunities London Southend Airport Station development - quick connections to London Medium-term runway extension Carlisle Airport Option being pursued New distribution centre as part of 460 acre site Waterway Port (Runcorn) Continue to evaluate development potential

Continue to evaluate development potential")

11

Balance Sheet 28 February 2009 £m 29 February 2008 £m Non-Current assets434.8279.7 Current assets (excl. cash)73.845.8 Cash7.34.5 Loans and borrowings (excl. HP)(74.7)(53.1) HP liabilities(53.4)(27.3) Trade and other payables(73.0)(43.5) Tax and deferred tax(34.5)(21.0) Disposal group net assets(1.1)24.0 Net Assets279.2209.1 Gearing – including HP Gearing – excluding HP 43.2%36.3% 29.8%26.7%

Cash Loans and borrowings (excl. HP)(74.7)(53.1) HP liabilities(53.4)(27.3) Trade and other payables(73.0)(43.5) Tax and deferred tax(34.5)(21.0) Disposal group net assets(1.1)24.0 Net Assets Gearing – including HP Gearing – excluding HP 43.2%36.3% 29.8%26.7%.")

12

Cash Flow Statement 28 February 2009 £m 29 February 2008 £m Continuing profit before tax23.93.5 Discontinued loss before tax(29.9)(30.4) Non-cash adjustments46.234.4 Working capital movements7.7(20.4) Cash generated from operations47.9(12.9) Tax paid(1.1)(0.9) Investing activities(128.0)68.2 Financing activities80.4(102.6) Decrease in cash in the period(0.8)(48.2)

(30.4) Non-cash adjustments Working capital movements7.7(20.4) Cash generated from operations47.9(12.9) Tax paid(1.1)(0.9) Investing activities(128.0)68.2 Financing activities80.4(102.6) Decrease in cash in the period(0.8)(48.2)")

13

Debt Reconciliation Non HP £mHP £mTotal £m B/f at 29 February 200847.927.375.2 Vehicles acquired under HP33.9 Repayments of HP15.8(15.8)- Non-Vehicle cap ex20.8 Proceeds on disposal of fixed assets(4.8) Cash raised in share issue (net of costs)(83.4) Acquisition cash consideration76.5 Net debt assumed on acquisitions16.88.024.8 Drawdown of RCF Dividends14.6 Operating cash flows(47.9) Tax Paid1.2 Net loans advanced to JVs2.8 Interest payable net7.6 Dividend receivable from JVs(0.6) c/f at 28 February 200967.353.4120.7

- Non-Vehicle cap ex20.8 Proceeds on disposal of fixed assets(4.8) Cash raised in share issue (net of costs)(83.4) Acquisition cash consideration76.5 Net debt assumed on acquisitions Drawdown of RCF Dividends14.6 Operating cash flows(47.9) Tax Paid1.2 Net loans advanced to JVs2.8 Interest payable net7.6 Dividend receivable from JVs(0.6) c/f at 28 February")

14

Repayment terms: Year End Balance HP in line with asset life £53.4m Working capital - rolling 12 months £16.6m RCF - August 2010 £25.0m Term loans - 2011 to 2021 £21.9m Vendor loan notes – December 2010 £6.0m Income shares – options March 2010 £5.2m Total £128.1m Debt terms

15

Strategy and Business Update Andrew Tinkler – CEO William Stobart - COO

16

KPIs 20092008 % change Revenue£431.0m£108.8m+296% EAFFC£27.5m£5.4m+409% Normalised PBT£23.1m£3.5m+560% EPS7.7p2.1p+267% Fleet Utilisation84.1%82.1%+2.4% Euro 4/5 Compliance81%56%+44.6% Reportable Accident Riddor1.30%1.43%-9.1%

19

Eddie Stobart Update

20

Chilled

21

Warehousing

22

Automated

23

Stobart has identified a unique, painless way to SIGNIFICANTLY reduce road-bourn pollution and the carbon footprint, whilst cutting the number of haulage vehicles on Britains hard-pressed roads and actually reducing road damage... all WITHOUT increasing fuel consumption! Developing the future of Road Transport The Companys innovative proposal, which is currently before Government, is the introduction of new semi-trailers which, through a more efficient proportion, actually offers as much as a 13% increase in carrying capacity when loaded with standard roller-cages, yet are shorter than existing standard trailers with a forklift mounted on the back. The slightly longer trailers remain within the 44 tonne weight limit and also feature rear wheel steering, that actually reduces road wear and improves manoeuvrability; allowing the turning circle to remain fully compliant with current legislation. The proposed trailers are fully compatible with current tractor units and cost a negligible amount extra that is quickly offset by the improved product-to- market costs of the increased capacity. Advantages with no disadvantages >Less than 1 metre longer than a standard trailer. >Up to 13% more FMCG cage capacity. >8% more CHEP pallet capacity. >Greater fuel-to-load efficiency. >No increase on the approved 44 tonne gross weight. >Less road congestion and pollution. >Significantly fewer vehicles on the road. >Rear wheel steering reduces road damage and improves manoeuvrability. >Fully compatible with current tractor units. >Complies with maximum turning circle legislation, despite the increased length. The new trailer has been exclusively tested and approved for Stobart by MIRA, confirming it is fully compliant with current legislation on turning circles, despite the increased length.

25

Runcorn waterway port Potential to be a major new facility for the North West

26

Stobart Rail Update Engineering

27

Stobart Rail Freight

28

Developments Rail Distribution facilities Air

33

Contact Details Andrew Tinkler Chief Executive Officer tinklera@eddiestobart.co.uk01228 882300 William Stobart Chief Operating Officer stobartw@eddiestobart.co.uk01228 822500 Ben Whawell Chief Financial Officer whawellb@eddiestobart.co.uk01925 605323 David Irlam Executive Director irlamd@eddiestobart.co.uk01925 605400 Trevor Howarth Legal Director and Company Secretary howartht@eddiestobart.co.uk01925 605400 Julie Gaskell Head of Communications gaskellj@eddiestobart.co.uk01925 605400 07768 038912

Similar presentations