Download presentation

Presentation is loading. Please wait.

1

Ryszard Ławniczak Katarzyna Blanke-Ławniczak Communication Challenges for Reverse Globalization’s Acquisitions EconPR 2010 April , 2010 Poznań g.15.00

2

Contents: The concepts of „reverse globalization” and „revers globalization acquisitions” Explaining the new phenomenon (what underpins the new trend?) Communication challenges for South-North FDI Strategies and instruments applied to overcome the obstacles for up-stream M&A’s

Communication challenges for South-North FDI. Strategies and instruments applied to overcome the obstacles for up-stream M&A’s.")

3

I. The concept of „reverse globalization” and „revers globalization acquisitions”

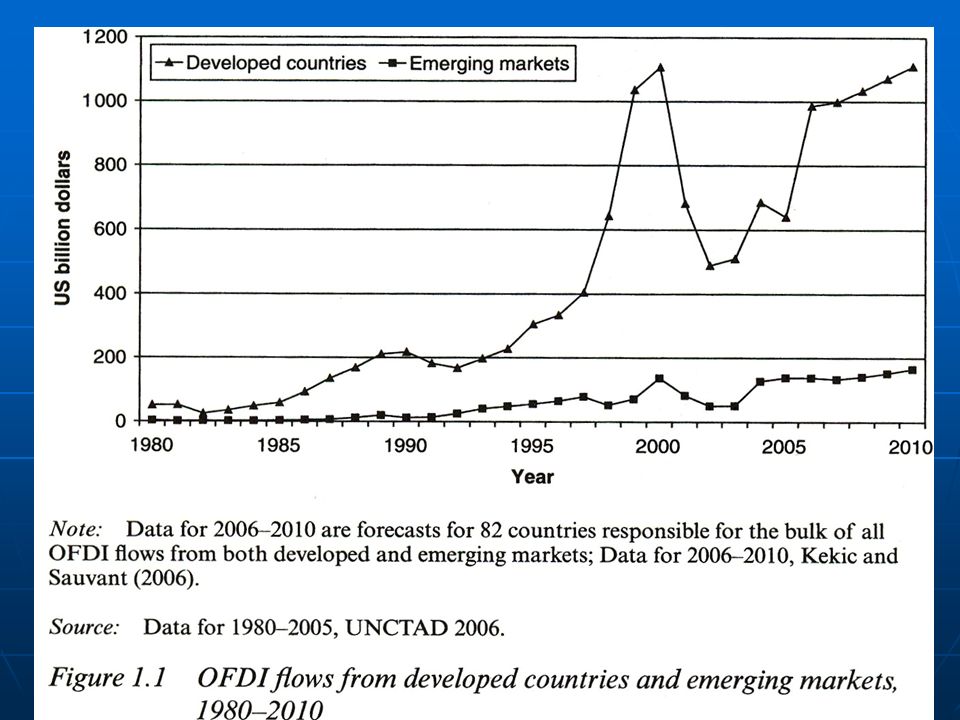

Economic globalization is generally understood as increasing economic integration of national economies as a result of rapid increase of cross-border flows of good, service, technology and capital. It was so far characterised mainly by the downhill flow of foreign direct investment from developed economies integrating with less developed.

4

Reverse globalization

Is a relatively new term, not yet fully „confirmed” ,and it is understood as: 1st – „bringing back activities” by companies withdrawing from overseas ventures, e.g. as a consequence of increased transportation costs from higher oil prices, which may outweight the other cost advantages from moving manufacturing to low-cost emerging markets (Jeff Rubin)

")

5

2nd, reversal of technology flows to developed economies – the new situation when emerging markets companies bring technology and capital and e.g.California, provides the labour and consumer market ( nearly 50% of California State’s solar energy needs are met by Chineese companies)

")

6

3rd, likely long-term consequence

of „uphill flow of capital” from emerging markets, buying companies not just bonds - in the developed world

9

Nasser al. Shaali, the CEO of Dubai International Financial Center (DIFC)

has in 2007 defined „reverse globalization” as a new situation „…when you have emerging market players going out and acquiring developed institutions – (which) is a tide that no matter how to try to swing against it, will be very, very prelevent in the years to come”

is a tide that no matter how to try to swing against it, will be very, very prelevent in the years to come")

10

Reverse globalization’s acquisitions (RGA) represents a new, long-term trend in the global economy, namely the South-North FDI (or up-market FDI) originating from emerging economies (i.e. developing and transition economies) and destined to advanced countries.

and destined to advanced countries..")

11

The above mentioned phenomenon of FDI from emerging into developed countries isn’t totally new. Already in the 1980’s Japaneese corporations invested heav into UK, and U.S. Today we simply observe the second, much larger wave of such FDI’s.

12

According to the Emerging Markets International acquisition Tracker (EMIAT) from KPMG’s Advisory practice emerging-to developed (E2D) deals have been recorded in the period , among others: by Indian corporations 121 – by Russian by Chineese 97 – by Central & Eastern European

![]()

13

According to Dealogic, in 2009 , for the first time, emerging markets outbound mergers and acquisitions flows outpaced inbound M&A flows, reaching US 131,8bn

14

The bigest sources of outward foreign investments and outward M&A :

The BRIC countries (Brazil, Russia India, China) Middle-East Arab (Gulf) countries Other smaller emerging countries, among them Central & East-European, like Poland Our study covers BRIC countries + Poland !

Middle-East Arab (Gulf) countries. Other smaller emerging countries, among them Central & East-European, like Poland. Our study covers BRIC countries + Poland !")

15

Major players in outward M&A deals:

BRIC private multinationals State-owned enterprices (SOEs) Sovereign wealth funds (SWFs) (e.g. in Russia, SOEs account for 26% and in China – for 75 outbound M&A.)

Sovereign wealth funds (SWFs) (e.g. in Russia, SOEs account for 26% and in China – for 75 outbound M&A.)")

16

The most spectacular E2D deals:

Who? Whom? When? Price Mittal Steel (India) Arcelor (France) 2006 $26.5bln Lenovo (China) IBM (personal computer division) 2005 $1.75 bln TATA (India) Corus (UK/Netherlands) 2007 $13.5bln TATA Motors (india Jaguar LandRover (UK) 2008 $2.3bln LUKOIL Nelson Resources Ltd.(UK); Getty Oil (US) 2001 $2bln $71m

Arcelor (France) $26.5bln. Lenovo (China) IBM (personal computer division) $1.75 bln. TATA (India) Corus (UK/Netherlands) $13.5bln. TATA Motors (india. Jaguar LandRover (UK) $2.3bln. LUKOIL. Nelson Resources Ltd.(UK); Getty Oil (US) $2bln. $71m.")

17

The most spectacular E2D deals (cont.):

Who? Whom? When? Price CBRD (Brazil) INCO (Canada) 2007 $16.7bln Geely (China) VOLVO ( car unit) 2010 $1.8 bln ORLEN (Poland) 494 ARAL petrol stations (Germany) 2002 E140mln

INCO (Canada) $16.7bln. Geely (China) VOLVO ( car unit) $1.8. bln. ORLEN (Poland) 494 ARAL petrol stations (Germany) E140mln.")

18

II. Explaining the new phenomena

19

Technological Managerial Know-how Know-how Raw materials Growth

potential Motivation for RGA’s Capital costs Profit margin Investment climate Source:DB Research

20

Motivation for RGAs Strategic, long lerm:

acqusition of raw materials (e.g.China) acquisition of „invisible assets” such as brand recognition and new technology (e.g.China, Russia, India) aquisition of foreign brands as one of the ways to develop global competitivnes

acquisition of „invisible assets such as brand recognition and new technology (e.g.China, Russia, India) aquisition of foreign brands as one of the ways to develop global competitivnes.")

21

Motivation cont.: diversification of markets

preemptive step to secure access against protectionist barriers foreign acquisition as a country branding investment military/strategic aims

22

Short term: Sound assests shifting to avoid decline in their relative value as a result of revaluation (e.g.China) Use of opportunities for takeovers of bunkrupt developed market firms (global financial crisis)

")

23

Geely Cahirman Li Shufu on Volvo acqusition:

„There are 3 levels of implications: 1. China –made cars access to the world 2. enhance the image of the chineese independent brand and enable China-made cars to have a share in the global arena 3. benefit Chineese consumers.”

24

Forces fuelling the new trend:

liberalization of trade and financial markets (OECD, WTO) liberalization of internal regulations in home countries relative surplus of capital easier access to global capital markets

liberalization of internal regulations in home countries. relative surplus of capital. easier access to global capital markets.")

25

Common sources of comparative advantage

High priority for investment proportion in research and developent Priority for human capital formation (e.g.education of engineers) Accumulation of huge amount of foreign exchange National government support (ownership advantage) Cost advantage Large domestic markets (huge population)

Accumulation of huge amount of foreign exchange. National government support (ownership advantage) Cost advantage. Large domestic markets (huge population)")

26

Country specific features:

India: mostly family owned firms with a dominant equity holder Broad range of sectors like steel, pharmaceuticals, infomation technology, services, automobiles China: Much of the OFDI carried out by large SOEs but also by SWFs Focused mainly on oil and petroleum, construction, shiping, telecom, automobiles

27

Russia: mainly state owned multinationals(SOM) majority of Russian OFDI is concentrated in oil, gas and metalurgy sector Brasil dominated by private sector in search of markets, natural resources and better investment climate

28

Poland: specifics of Polish transformation (early „pieriestroika”, relative opening to the „West”, legacy of the socialist education) the speed of decision making process managerial skills the positive effects of „shock therapy”

29

III. Communication challenges for South-North FDI HOST COUNTRIES

They find the expression in escalation of protectionism, especially on grounds of the national security, and preservation of working places.

30

They are also primarily related to the developed countries businesses, governments and peoples:

fears , national pride concerns about „established order of industrial hegemony”. existing stereotypes and different type of prejudicie perception that EMI’s are beneficiaries of unfair state aid.

31

To overcome those fears EMIs have to address

their communication efforts to gain trust fight stereotypes and prejudicies (e.g. Mittal- „company of Indians”) uphold high quality standards (e.g. Quality of Mittal’s steel;„Now China is going to junk a solid high-quality brand” – (web comment on Geely/Vovo deal) build up a brand narrow the cross-cultural differences

uphold high quality standards. (e.g. Quality of Mittal’s steel;„Now China is going to junk a solid high-quality brand – (web comment on Geely/Vovo deal) build up a brand. narrow the cross-cultural differences.")

32

HOME COUNTRIES Micro level:

managment issues – cultural gap, skills and courage limited fincial resources Meso level: lack of institutions in support of E2D deals Macro level: administrative barriers foreign currency restictions

33

IV. Strategies and tools in support for successful up-stream M&A’s

34

HOW to communicate -communication channels

Government communication Corporate communication Outsourcing to global communication conglomerates (WPP,OMNICOM etc.) Building up an international lobbying organization

Building up an international lobbying organization.")

35

WHAT to communicate – key messages:

it’s merger not takeover message (case: Mittal Steel/Arcelor) „Together we are stronger” employment argument local content argument CSR

„Together we are stronger employment argument. local content argument. CSR.")

36

key messages (cont): management remains – you know it better approach (Case TATA/Jaguar LandRover deal) „JaguarLandRover will retain their distinctive indentities” or „Volvo remains Volvo” double standards arguments - „you should practice what you pray”

37

WHAT communicate to host country and international publics:

Problem Message Case Management oposition management remains („you know it better”); „it’s a merger not takeover” (Case TATA/Jaguar LandRover deal); (case:Arcelor/ Mittal) Employment reduction Job creation/ preservation; assymetry China M&A Associations Campaign Quality standards products will retain their distinctive indentities”; dont’confuse china OWNED with China BUILT „JaguarLandRover TATA, or „Volvo remains Volvo”

; „it’s a merger not takeover (Case TATA/Jaguar LandRover deal); (case:Arcelor/ Mittal) Employment reduction. Job creation/ preservation; assymetry. China M&A Associations. Campaign. Quality standards. products will retain their distinctive indentities ; dont’confuse china OWNED with China BUILT. „JaguarLandRover TATA, or „Volvo remains Volvo")

38

WHAT communicate to host country and international publics (cont.):

Problem Message Case Competition for „national champions” Local content; dilution of national origin; trustful brand ORLEN/Germany; Lenovo /Ogilvy &Mother brand building contract Local oposition cost reduction; CSR; new huge markets Geely/Volvo National pride dilution of national origin of ownership Mittal; Kulczyk; ORLEN

39

WHAT communicate to host country and international publics (cont. 2):

Problem Message Case National security concerns firm owership doesn’t matter; NATO/ OECD/ WTO membership Poland Unfair government aid SOE and SWF are focused on shareholders value; double standards; assymetry/reciprocity Chinese Foreign Ministry intervention; CNOOC Chairman’s interview

40

WHAT communicate to home country publics:

Problem Message Case Management perception shifting Internal PR -„we can do it” ORLEN National economic interest Opportunity to gain a recognised brand Hummer/Sichun Tengzhong deal Oposition against global economic supremacy Globalization is a two-way street US No to Chineese acquisition of US banks National pride Government communication e.g. Media articles in India and China

41

Concluding remarks Reverse globalization acquisitions (up-stream FDI) is a new, long term trend in the global economy Challenges faced by emerging markets investors in developed countries are based on fears, prejudicies, false stereotypes and neglegance of intercultural differences. Further intensive and sophisticated communication efforts are necessary in support for succesfuls South-North deals.

42

Thank you for your attention

Similar presentations

Conference.>")

By the end of 1990s, produced.>")