Download presentation

Presentation is loading. Please wait.

1

Bank Supervision Russian Style: Evidence of conflicts between micro- and macro-prudential objectives Sophie Claeys Koen Schoors May 2007

2

Motivation Not about bureaucrats versus politicians Not about turf wars between agencies Not about conflict between regulation and supervision But about goal conflict within agencies Two goals under scrutiny Systemic stability (macro-prudential) Individual bank stability (micro-prudential)

Individual bank stability (micro-prudential)")

3

Conflicts of interest Bank Supervision Deposit Insurance Management international reserves Monetary policy Central Bank Lender of last resort -Money emission -Management of the payments system Inflation versus systemic stability Exchange rate versus inflation oriented policy Systemic versus individual bank stability Deposit insurance versus individual bank stability

4

Conflicts of interest Bank Supervision Deposit Insurance Management international reserves Monetary policy Central Bank Lender of last resort -Money emission -Management of the payments system Inflation versus systemic stability Exchange rate versus inflation oriented policy Systemic versus individual bank stability Deposit insurance versus individual bank stability

5

Short term conflict between objectives Systemic versus Individual bank stability Central Banks reponsible for systemic stability Lender of Last Resort function (LLR) Creates Moral Hazard Need for prudential regulation / bank supervision Strict enforcement of rules systemic stability The consequence may be forbearance Dynamic inconsistency between rule-based supervision and systemic stability?

Creates Moral Hazard Need for prudential regulation / bank supervision Strict enforcement of rules systemic stability The consequence may be forbearance Dynamic inconsistency between rule-based supervision and systemic stability")

6

Literature Theoretical literature touches on these conflicts of interest Bagehot (1873): Goodhart and Huang (1999): constructive ambiguity Cordella and Yeyati (2003): contingent ex ante commitment Freixas et al. (2000): forebearance towards money-center banks Kahn and Santos (2005): endogenous forbearance More obscure reasons for forbearance Boot and Thakor (1993): reputation seeking supervisors Wall and Peterson: too big to fail Kane (2000): too big to discipline adequately Mitchell (1999): too many to fail Heineman and Shüler (2004): regulatory capture

: forebearance towards money-center banks Kahn and Santos (2005): endogenous forbearance More obscure reasons for forbearance Boot and Thakor (1993): reputation seeking supervisors Wall and Peterson: too big to fail Kane (2000): too big to discipline adequately Mitchell (1999): too many to fail Heineman and Shüler (2004): regulatory capture.")

7

Why Russia ? CBR has all authorities and owns important commercial banks LLR Banks supervision and control Monetary policy and exchange rate policy no turf wars and ample scope for conflicts of interest CBR designs and enforces the rules No regulation versus supervision problem Enforcement is measurable Although we do not observe fines etc, We do observe license withdrawals, i.e. the ultimate sanction for repeated and/or severe breaches

8

Bank creation and destruction (monthly data) peak of 347 banks in November 1990

peak of 347 banks in November 1990")

9

Why 1999-2002 ? April 1996: Revised set of prudential regulations 1998: move away from RAS towards IAS August 1998 quadruple crisis pre and post crisis data are difficult to compare March 1999: new law on bank restructuring central role of CBR in licensing behaviour Focus on bank license behaviour of the CBR: Later there is a new crisis (2004) and the introduction of deposit insurance (2005)

and the introduction of deposit insurance (2005).")

10

Empirical approach Analyze enforcement of prudential regulations Dependent variable is license revokal Control for economic variables that explain bank failure Control for tacit CBR objectives (systemic stability) Enforcement is measured as the impact of non- compliance with bank standards on license revokal Hypothesis I: De-licensing is driven by micro-prudential concerns Hypothesis II: Micro- and micro-prudential concerns do not conflict

Enforcement is measured as the impact of non- compliance with bank standards on license revokal Hypothesis I: De-licensing is driven by micro-prudential concerns Hypothesis II: Micro- and micro-prudential concerns do not conflict")

11

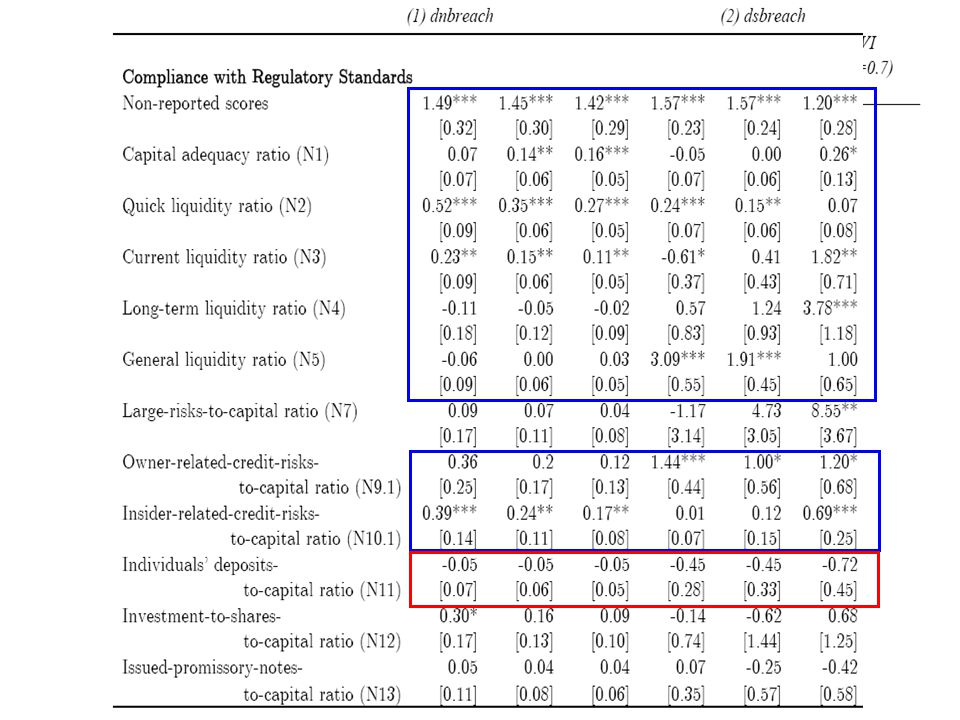

Micro-prudential concerns: the bank standards? N1 or the capital adequacy ratio N2 or the instant liquidity ratio N3 or the current liquidity ratio N4 or the long-term liquidity ratio N5 or the general liquidity ratio N7 or maximum large credit risk N9.1 or maximum risk per borrower-shareholder N10.1 or maximum credit to insiders N11, minimal coverage of household deposits by capital N12 or minimal coverage by the banks investments in shares by capital N13 or the banks own promissory notes liability risk ratio

12

How to measure enforcement?

13

Principles of Compliance measures We observe bank compliance to regulatory standards: Every quarter banks report scores on the bank standards We know the time-varying regulatory threshold for every standard This allows the identification of time and bank specific breaches We use this information to construct measures for bank compliance to regulatory standards We value current breaches higher than past breaches CBR cares more about current than past breaches Still past breaches are not totally forgiven

14

Compliance measures I Number of breaches Define for every bankquarter the standard-specific breaches (score exceeds threshold) Each bank i has a number of breaches, defined as: We discount past breaches using and construct:

Each bank i has a number of breaches, defined as: We discount past breaches using and construct:")

15

Compliance measures II Average severity of breach One-sided average severity of breach defined as We discount past breaches using and construct: We also create a dummy if standards are not reported

16

Macro-prudential objectives Regional banking coverage or minimal competition Regional Herfindahl index Political influence Share of government claims in assets – government capture Government ownership Pocket-banks – political incentives to show forbearance for bank standards N9.1 and N10.1. Systemic stability Size (TBTF or TBTDA) Too many too fail Money center banks (interbank liabilities) Protect deposit banks – forbearance for N11 (household deposits over capital)

Too many too fail Money center banks (interbank liabilities) Protect deposit banks – forbearance for N11 (household deposits over capital).")

17

Economic fundamentals Return on assets Cost/assets Interbank liabilities/liabilities Regional market share (assets) Non performing loans/loans Reserves/assets Government bonds/assets

Non performing loans/loans Reserves/assets Government bonds/assets")

18

The data Registration data of the CBR Complete database available from CBR All banks (1988 till now), All licensing data (when received, type, when revoked, reason for revocation) Interfaks database from 1999 up till 2002 Quarterly bank balances, profit and loss data, Quarterly bank specific scores on every standard 99-02 Mobile database Quarterly bank specific scores on standards 97-99, for calculation of compliance variables only

, All licensing data (when received, type, when revoked, reason for revocation) Interfaks database from 1999 up till 2002 Quarterly bank balances, profit and loss data, Quarterly bank specific scores on every standard Mobile database Quarterly bank specific scores on standards 97-99, for calculation of compliance variables only")

19

Hypothesis I - +

22

Hypothesis II - + -

24

Main findings I Bank failures are sensibly related to economic variables Efficiency Loan quality Reserves Macro-prudential objectives matter: Banks are less likely to face license revokal IF They are in highly concentrated regional bank markets They are large They are money center banks There are too many failing banks

25

Main findings II There is some level of enforcement of bank standards Capital adequacy standards Liquidity standards, but is his good news? Insider bank standards Forbearance is related to systemic stability issues Offenders of liquidity standards are not punished in poorly banked regions Frequent offenders of capital adequacy get away if they are large Severe liquidity shortages are forborne if they are too many banks too fail. But frequent offenders are punished in that case.

26

Concluding remarks Not all is bad in Russian bank supervision But Need to think about appropriate role for CBR Doing everthing implies doing nothing perfect The found conflict may be a general problem Further work in other develping markets needed

Similar presentations

Robert Marquez (Arizona State University) The views expressed.>")