Download presentation

Presentation is loading. Please wait.

1

Bank Efficiency and Market Structure: What Determines Banking Spreads in Armenia? Era Dabla Norris and Holger Floerkemeier

2

Motivation Banking spreads as indicators of efficiency of financial intermediation - Transition-countries financial systems mainly bank- based - High cost of financial intermediation impedes financial deepening Case study: Armenia - Despite progress in banking sector reform: - Low financial intermediation - High banking spreads

3

Comparatively advanced banking sector reforms,

4

... but low financial development,

5

... and persistently high banking spreads.

6

What we do Examine role of bank characteristics, market structure, and macroeconomic variables in explaining intermediation efficiency in Armenia - Is there effect of differences in loan portfolios of banks? - Do variations in market shares across market segments account for differences in spreads across banks? - Has foreign entry played a role? - Is there a spill-over effect of foreign banks on domestic banks? - Does the origin of the foreign bank matter?

7

Armenian Banking System: Stylized Facts Substantial consolidation in past decade gradual tightening of prudential regulations and a number of bank failures By 2007: 21 commercial banks; all privately owned since 2001 Foreign ownership has increased over time (14 banks; over 60 percent of total assets) - Only one international first-tier bank; others banks from CIS countries/ Armenian Diaspora Small banking system (low asset/GDP ratio) but well capitalized, liquid, and profitable, with satisfactory level of asset quality. Low overall concentration but segmented markets

8

Dataset Panel of 20 banks 2002Q4 – 2006Q3 (16 quarters) Bank balance sheet and income data Data sources: - Central Bank of Armenia - ARKA news agency

Bank balance sheet and income data Data sources: - Central Bank of Armenia - ARKA news agency")

9

Methodology (1) I i,t = + B i,t + C t + M t + i,t Alternative spread variables (I) Bank characteristics (B), market structure (C), and macroeconomic variables (M) as regressors OLS and Fixed effects regression Time dummies Robust clustered standard errors

I i,t = + B i,t + C t + M t + i,t Alternative spread variables (I) Bank characteristics (B), market structure (C), and macroeconomic variables (M) as regressors OLS and Fixed effects regression Time dummies Robust clustered standard errors")

10

Methodology – Dependent Variables Ex post interest spread Difference between interest income divided by average loans and interest expenses divided by average deposits Net interest margin Difference between total interest income and expenses over average assets Ex ante spread (incomplete data) Difference between the weighted average lending rate and the weighted average deposit rate

Difference between the weighted average lending rate and the weighted average deposit rate")

11

Methodology – Independent Variables Bank characteristics Overhead (+) Non-interest income (-) Bank size (-) Market share (+) Capital adequacy (+/-) ROA (+/-) Liquidity (+/-) Foreign bank dummy (-) Credit portfolio shares (+/-)

Non-interest income (-) Bank size (-) Market share (+) Capital adequacy (+/-) ROA (+/-) Liquidity (+/-) Foreign bank dummy (-) Credit portfolio shares (+/-)")

12

Methodology – Independent Variables Market structure Concentration [HHI and CR] (+) Foreign participation (-) Market shares in loan segments (+) Macroeconomic variables Exchange rate changes (+) Real GDP growth (-) Inflation (+) Money market rate (+)

![Methodology – Independent Variables Market structure Concentration [HHI and CR] (+) Foreign participation (-) Market shares in loan segments (+) Macroeconomic variables Exchange rate changes (+) Real GDP growth (-) Inflation (+) Money market rate (+)](http://images.slideplayer.com/2/697272/slides/slide_12.jpg "Methodology – Independent Variables Market structure Concentration [HHI and CR] (+) Foreign participation (-) Market shares in loan segments (+) Macroeconomic variables Exchange rate changes (+) Real GDP growth (-) Inflation (+) Money market rate (+)")

13

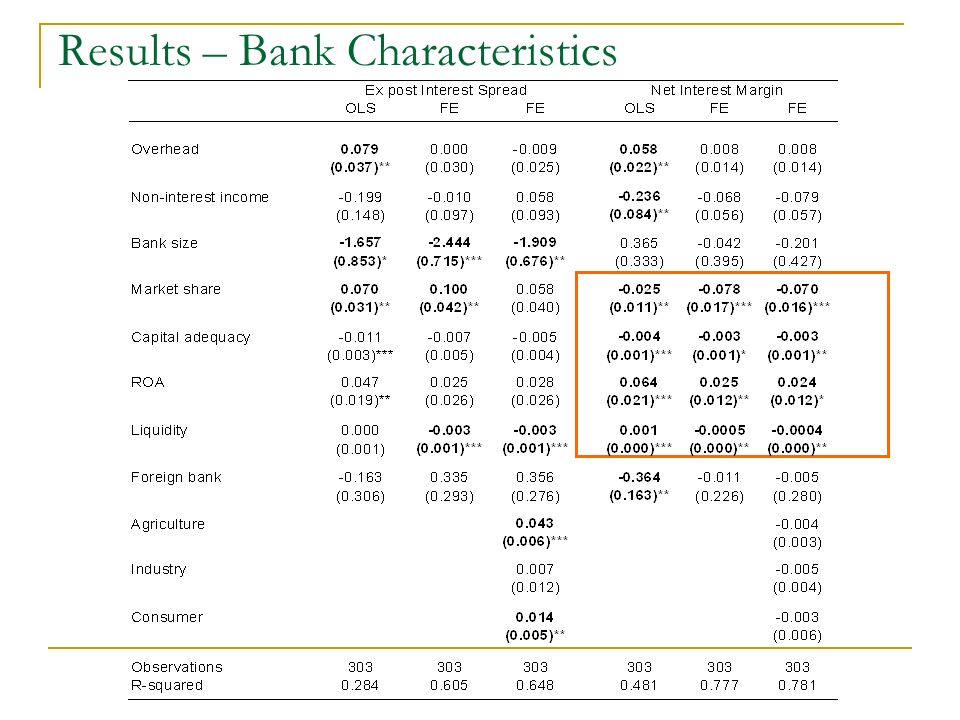

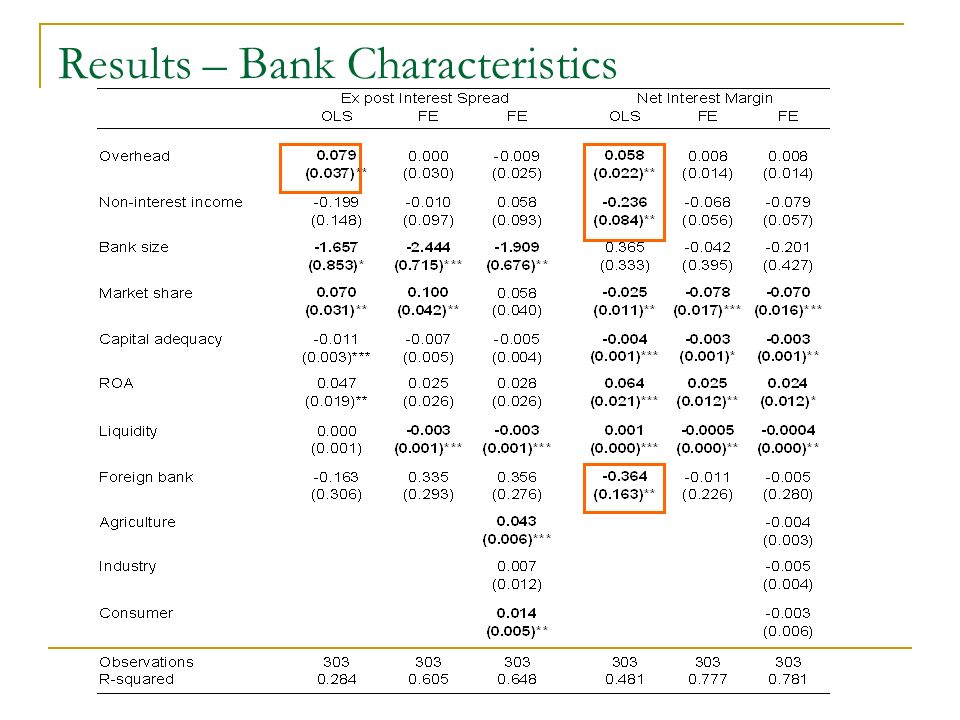

Results – Bank Characteristics

16

Significant role of bank-specific fixed effects Ex-post interest spreads depend on - Bank size (economies of scale) - Deposit market share (market power) - Liquidity - Loan portfolio Net interest margins depend on - Deposit market share (but negative sign) - Capital adequacy - ROA - Liquidity Foreign banks not associated with lower spreads/margins

- Deposit market share (market power) - Liquidity - Loan portfolio Net interest margins depend on - Deposit market share (but negative sign) - Capital adequacy - ROA - Liquidity Foreign banks not associated with lower spreads/margins")

17

Results - Market Structure: Foreign Ownership

18

Results - Market Structure: Concentration

19

Results - Market Share and Macroeconomic Variables

20

Results - Market Structure And Macroeconomic Variables Foreign ownership has no robust impact - foreign bank dummy mostly insignificant - foreign bank presence in loan/deposit market lowers margins evidence of spill-over effect - origin seems to matter for lowering spreads Concentration raises spreads and margins - HHI: impact significant and robust - Market share in industry loans lowers spread - Market share in industry and consumer loans raises margins Macroeconomic variables not very important

21

Conclusions Economies of scale Market power Market segmentation - relationship banking - information sharing - market transparency Foreign ownership - no direct effect - but possibly spillover effects - origin of foreign bank matters

Similar presentations

should be more prevalent in poorer countries, with less developed financial markets, with less well->")

The University of the West Indies, St. Augustine,>")

Asli Demirgüç-Kunt (World Bank) Harry.>")