Download presentation

Presentation is loading. Please wait.

1

SUBPRIME CRISIS Presented by: Shruti Tiwari

2

Financial Crisis-Meaning Situation in which financial Institutions or assets loose a part of their value. It includes stock market crash, currency crisis & busting of other financial bubbles. Types of Financial crisis : a) Banking Crisis :Sudden rush of withdrawal by depositor (bank run)

Banking Crisis :Sudden rush of withdrawal by depositor (bank run).")

3

b) Wider Economic Crisis Recession: Downturn in economic growth lasting several quarters or more Depression: Prolongated recession Stagnation: Long period of slow but not negatively growth.

Wider Economic Crisis Recession: Downturn in economic growth lasting several quarters or more Depression: Prolongated recession Stagnation: Long period of slow but not negatively growth.")

4

Reasons for Financial Crisis Strategic Complementary in Financial Market Asset- Liability Mismatch Regulatory Failure :Regulators make sure that institutions have sufficient assets to meet out obligations Contagion: Financial crisis spread from one institution to another.

5

Key Terms Credit (Debt) Credit Squeeze :Control of money supply by govt. Liquidity Crisis : business experiences lack of cash required to meet out its debt obligation Freezing of economic activity: Investment sentiments go down, banks are unwilling to lend Monetary policy & Fiscal Policy Investment Banking Mortgages

6

Bailout : Act of loaning or giving capital to a failing business in order to save it from bankruptcy,insolvency. Securitization: Pooling & Repackaging of Cash Flow producing financial assets into securities that are sold to investors Collateral Debt Obligation :Security backed by diversified pool of debt obligation such as bonds loans or structured instrument.

7

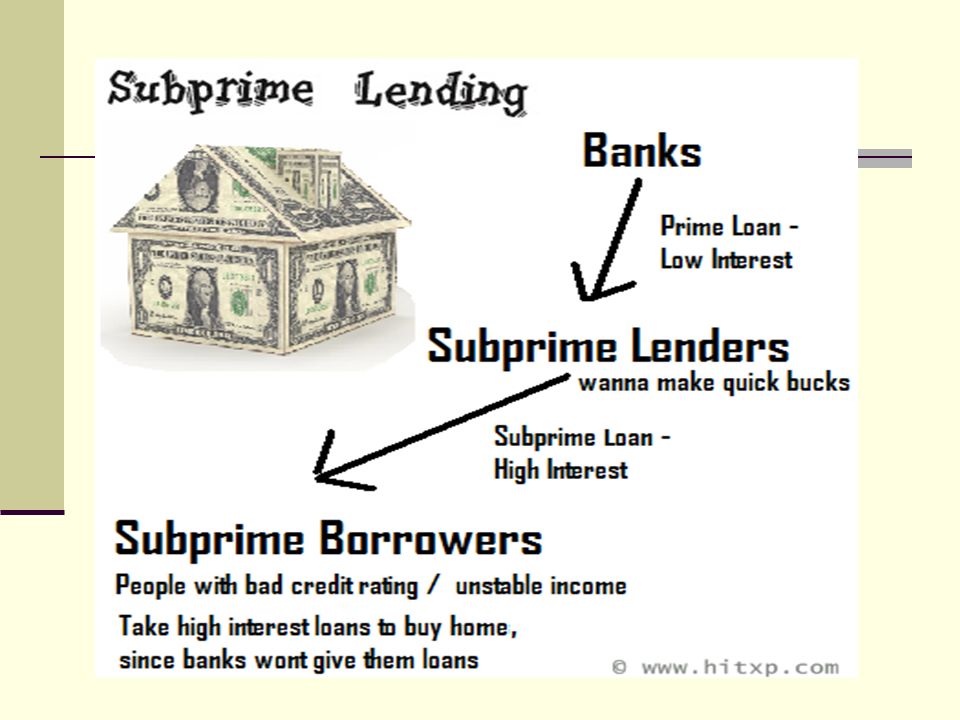

Advertisements in US "No repayment for first 2 years“ "Want to be rich ? Buy Property!“ "Money no enough? Borrow from me!”. "Zero down payment" "Low rate guaranteed"

9

Introduction Borrowers are rated either as 'prime' - indicating that they have a good credit rating based on their track record As 'sub-prime', meaning their track record in repaying loans has been below par. It is the poor and the young who form the bulk of sub- prime borrowers.

10

How it Started..?????? In the mid 90s, there was a push to ease the rules for first time home purchasers under the Clinton administration’s National Home Ownership strategy. Expanding home ownership was also a center piece of George Bush’s agenda as president. 2000 dot com bubble Almost every rule was relaxed.

11

Proof of income for loans was reduced from five years to three. Houses were offered with low or no down payment. “Teaser rates” (where interest rates were as low as 1% initially but then went up to 8%). “Liar mortgages” (in which the information provided by applicants was not checked)

. Liar mortgages (in which the information provided by applicants was not checked).")

13

Sub-prime crisis The sub-prime mortgage crisis is an real estate crisis and financial crisis triggered by a dramatic rise in mortgage delinquencies and foreclosures in the United States. Major adverse consequences for banks and financial markets around the globe. Approximately 80% of U.S. mortgages issued in recent years to sub-prime borrowers were adjustable-rate mortgages.

14

Contd.. As interest rates started falling due to excess liquidity, house prices started rising rapidly, creating a pool of wealth in the hands of Americans, which they unlocked by contracting mortgage loans. It benefited them in two ways — they got huge liquidity at inflated housing prices and at interest rates that were practically lowest in the last 20 years. This became a virtuous cycle, resulting in a very high consumer spending and obviously fuelling global growth.

15

Sub-prime crisis contd…. Securities backed with sub-prime mortgages, widely held by financial firms, lost most of their value. It has started causing problems for Americans in the form of job losses, less consumer spending and the fears of a slowdown.

16

What was the interest rate on sub-prime loans ?????? Interest rate charged on sub-prime loans was typically about two percentage points higher than the interest on prime loans. The higher interest rate additionally meant substantially higher EMIs than for prime borrowers, further raising the risk of default. New instruments were devised to reach out to borrowers Instruments which asked borrowers to pay only interest payments were devised.

17

Federal Fund Rate in the US

18

How did this turn into a crisis? One major reason was that the boom had led to a massive increase in the supply of housing. Thus house prices started falling This increased the default rate among sub prime borrowers Many of whom were no longer able or willing to pay the collateral is typically the home being bought This increased the supply of houses for sale while lowering the demand, thereby lowering prices even further and setting off a vicious cycle. The declining value of the collateral means that lenders are left with less than the value of their loans and hence have to book losses.

19

The Deterioration of the Sub-prime Market.. Combination of industry trends and economic and financial factors combined to create the current crisis in the mortgage markets. Borrowers with financial difficulties could not sell their homes to pay off mortgages In 2006 and 2007, borrowers suffered “Payment Shock” when teaser rates on many hybrid ARMs expired and higher variable rates became effective.

20

The Deterioration of the Sub-prime Market Rising defaults on sub-prime and Alt-A mortgages have caused rating agencies to downgrade MBS and CDO bonds backed by sub-prime mortgages. Investors in those securities have already suffered substantial losses, and uncertainty in the financial markets about the value of such securities and potential losses has adversely impacted liquidity in the financial markets.

21

Factors Responsible The immediate cause or trigger of the crisis was the bursting of the United States housing bubble which peaked in approximately 2005–2006. High default rates on "sub-prime" and adjustable rate mortgages (ARM), began to increase quickly thereafter. Once interest rates began to rise and housing prices started to drop moderately in 2006–2007 in many parts of the U.S.

, began to increase quickly thereafter. Once interest rates began to rise and housing prices started to drop moderately in 2006–2007 in many parts of the U.S..")

22

Loans of various types (e.g., mortgage, credit card, and auto) were easy to obtain and consumers assumed an unprecedented debt load. As part of the housing and credit booms, the amount of financial agreements called mortgage-backed securities (MBS), which derive their value from mortgage payments and housing prices, greatly increased.

, which derive their value from mortgage payments and housing prices, greatly increased..")

23

Impact on US Economy Many Banks were closed down Bear Stearns near collapse shaken the confidence of public in its banking system. September 2008 : Lehman brother( biggest investment bank ) filed for bankruptcy. Bailout Packages by US govt. were not enough AIG was saved by providing $ 80 billion bailout by govt. Citi Bank was bailed out by $ 60 billion UK : Northern Rock –Withdrawal of 2 billion pounds

filed for bankruptcy. Bailout Packages by US govt. were not enough AIG was saved by providing $ 80 billion bailout by govt. Citi Bank was bailed out by $ 60 billion UK : Northern Rock –Withdrawal of 2 billion pounds.")

24

Many bailouts were given in European county Nationalization of bank was the step taken by many country's govt. like Russia & Greece

25

Impact on Indian Economy Slowdown in external demand, reversal of capital flow, growth in Industrial production decelerated to 2.8% in 2008-09 from 8% previous year. Service sector remained largely in effected with growth of 9.7% in 2008-09 as against 10.5% in previous year. Real GDP growth slowed down to 6.7% in 2008- 09 as against 9%. Slowdown in Exports.

26

Indian Stock Market in Last one year

27

Actions by central bank Cash Reserve Ratio brought down to 5% in January 2009 from 9% (September 2008) injecting Rs.1600 billion is primary liquidity. Repo and Reverse Repo rates are cut down from 9% to 4.75% and 6% to 3.25% respectively. Banks were advised to step up lending to core sectors. Restriction on interest rate to bulk deposits. Restrictions loosened on External commercial borrowing by corporate.

28

Key Macro Indicators IndicatorPeriod2007-082008-09 Growth, per cent Real GDP GrowthApril-December9.06.9 Industrial production April-February8.82.8 ServicesApril-December10.59.7 ExportsApril-March28.46.4 ImportsApril-March40.217.9 Stock Market (BSE Sensex) April-March16,56912,366 Rs.per US$April-March40.2445.92

April-March16,56912,366 Rs.per US$April-March")

29

India’s Approach to Managing Financial Stability Financial sector, especially banks, subject to prudential regulation Both liquidity and capital. Prudential limits on banks’ inter-bank liabilities Asset-liability management guidelines Basel II framework: guidelines issued. NBFCs: regulation and supervision tightened - to reduce regulatory arbitrage.

30

Lessons for Indian Investors The financial sector in India has a long way to go in developing a sophisticated risk-minimizing strategy by adopting complex financial instruments to limit the sources of risk affecting their asset portfolios. It should adopt better standards to evaluate the credit worthiness of potential borrowers.. Investors should carefully evaluate the future before taking new loans for asset purchases. As a globally integrated economy, international events will leave its mark on our economy whether we like it or not.

Similar presentations