Download presentation

Presentation is loading. Please wait.

2

1 Sect. 5 - The Financial Sector Module 22 - Saving, Investment, and the Financial System What you will learn: The relationship between savings and investment spending The purpose of the four principal types of financial assets: stocks, bonds, loans and bank deposits How financial intermediaries help investors achieve diversification

3

Sect. 5 - The Financial Sector Module 22 - Saving, Investment, and the Financial System Savings - Investment Spending Identity - Savings and investment spending are always equal for the economy as a whole *Total Income = Total Spending *Total Income = Consumer Spending + Savings *Total Spending = Consumer Spending + Investment Spending *Consumer Spending + Savings = Consumer Spending + Investment Spending *Savings = Investment Spending

4

3 Budget Surplus - When tax revenue exceeds government spending Budget Deficit - When government spending exceeds tax revenue National Savings - Sum of private savings and the budget balance - total savings generated in the economy Capital Inflow - Net inflows of funds into a country - includes net exports

5

4 Financial System - Where households invest their savings or wealth by purchasing financial assets Financial Asset - A paper claim that entitles buyer to future income from the seller - (loans, bonds, stocks, securities) Physical Asset - A claim on a tangible object giving the owner the right to dispose of as they wish - house, building, equipment

Physical Asset - A claim on a tangible object giving the owner the right to dispose of as they wish - house, building, equipment")

6

5 Three Tasks of a Financial System - 1) Reduce Transaction Costs - Large sums of money can be borrowed from financial institutions without incurring large transaction costs 2) Reduce Financial Risk - People would not likely take financial risks - financial system makes it possible to borrow and invest with less risk Diversification - Investing in several different assets to minimize risk 3) Provide Liquidity - Because the future is uncertain it may be necessary to convert assets into cash quickly

Reduce Transaction Costs - Large sums of money can be borrowed from financial institutions without incurring large transaction costs 2) Reduce Financial Risk - People would not likely take financial risks - financial system makes it possible to borrow and invest with less risk Diversification - Investing in several different assets to minimize risk 3) Provide Liquidity - Because the future is uncertain it may be necessary to convert assets into cash quickly")

7

6 Types of Financial Assets - Loans - A lending agreement between lender and borrower - interest is the cost paid for the loan Bonds - An IOU issued by the borrower with a fixed interest rate and maturity date - more liquid than loans

8

7

9

8

10

9 Types of Financial Assets - Loans - A lending agreement between lender and borrower - interest is the cost paid for the loan Bonds - An IOU issued by the borrower with a fixed interest rate and maturity date - more liquid than loans Loan-Backed Securities - Pooling individual loans together and selling shares in that pool of loans - mortgages, student loans, credit card

11

10 Stocks - A share in ownership of a company - share in the wealth and profit - used to raise capital and defer risk

12

11

13

12 Stocks - A share in ownership of a company - share in the wealth and profit - used to raise capital and defer risk Financial Intermediaries - Institution that transforms the funds gathered from many individuals into financial assets Mutual Funds - Creates a diversified collection of stocks then resells shares to individual investors - lower risk

14

13 Pension Funds & Life insurance Companies - Pension Fund - retirement version of mutual fund Life Insurance Co. - sell policies that guarantee payment to beneficiaries Banks - Allow liquidity for depositors as well as loans from deposits

15

14 Module 23 - The Definition and Measurement of Money What you will learn: The definition and functions of money The various roles money plays and the many forms it takes in the economy How the amount of money in the economy is measured

16

15 Module 23 - The Definition and Measurement of Money Money - Any asset that can easily be used to purchase goods and services - currency or other highly liquid assets like bank deposits Role of Money - Medium of Exchange - An asset used to trade for goods & services

17

16

18

17 Module 23 - The Definition and Measurement of Money Money - Any asset that can easily be used to purchase goods and services - currency or other highly liquid assets like bank deposits Role of Money - Medium of Exchange - An asset used to trade for goods & services Store of Value - It holds purchasing power over time Unit of Account - A standard measure to set prices and make economic calculations

19

18 Types of Money - Commodity Money - A good that has intrinsic value like gold or silver Commodity Backed Money - Has no intrinsic value but is backed by a valuable good like gold or silver

20

19

21

20 Types of Money - Commodity Money - A good that has intrinsic value like gold or silver Commodity Backed Money - Has no intrinsic value but is backed by a valuable good like gold or silver Fiat Money - Money whose value is derived only from its official status as a means of exchange - US currency - does not tie up resources and supply is based on need

22

21 Measuring the Money Supply - Two monetary aggregates calculated by The Federal Reserve M1 = Only cash, travelers checks, and checkable bank deposits - $1,676.4 trillion ( 51% cash, 48% checking, 1% trav. checks) M2 = M1 + Near Moneys (liquid - savings accounts, CDs, money market) - $8,462.9 trillion

M2 = M1 + Near Moneys (liquid - savings accounts, CDs, money market) - $8,462.9 trillion.")

23

22 Module 24 - The Time Value of Money What you will learn: Why a dollar today is worth more than a dollar a year from now How present value can help you make decisions when costs or benefits come in the future

24

23 Module 24 - The Time Value of Money Borrowing, Lending, and Interest - The cost for borrowed money is interest - a percentage of the money we borrow paid over time $X x (1+r ) Ex: $500 x (1 + 0.08) = $500 x 1.08 = $540 Present Value - What is the value of a dollar today as compared to the value of that dollar in the future $X / (1+r ) Ex: $540 / (1 + 0.08) = $540 / 1.08 = $500

Ex: $500 x ( ) = $500 x 1.08 = $540 Present Value - What is the value of a dollar today as compared to the value of that dollar in the future $X / (1+r ) Ex: $540 / ( ) = $540 / 1.08 = $500")

25

Net Present Value - The present value of current and future benefits minus the present value of current and future costs *Best option is the one with the highest net present value

26

25 Module 25 - Banking and Money Creation What you will learn: The role of banks in the economy The reasons for and types of banking regulations How banks create money

27

26 Module 25 - Banking and Money Creation The Monetary Role of Banks - Banks use liquid assets from deposits to finance the investments of borrowers Bank Reserves - Banks cannot lend out all deposits - reserves are held at the bank or with The Federal Reserve - part of M2 T-Accounts - A table showing the assets and liabilities of a business or bank - used to analyze a businesses financial situation

29

28 Module 25 - Banking and Money Creation The Monetary Role of Banks - Banks use liquid assets from deposits to finance the investments of borrowers Bank Reserves - Banks cannot lend out all deposits - reserves are held at the bank or with The Federal Reserve - part of M2 T-Accounts - A table showing the assets and liabilities of a business or bank - used to analyze a businesses financial situation

30

29 Required Reserve Ratio - % of deposits banks must hold in reserve and cannot loan out Bank Run - When many depositors try to withdraw their funds at the same time - caused by a panic or fear of financial trouble Bank Regulation - Deposit Insurance - 1933 The FDIC (Federal deposit Insurance Corporation) insures deposits up to $250,000 Bank Run

insures deposits up to $250,000 Bank Run")

32

31 Required Reserve Ratio - % of deposits banks must hold in reserve and cannot loan out Bank Run - When many depositors try to withdraw their funds at the same time - caused by a panic or fear of financial trouble Bank Regulation - Deposit Insurance - 1933 The FDIC (Federal deposit Insurance Corporation) insures deposits up to $250,000 Bank Run

insures deposits up to $250,000 Bank Run")

33

Capital Requirements - Banks are required to have capital of at least 7% of total assets in addition to required reserves Discount Window - Banks can borrow money from The Federal Reserve at the “discount rate” if necessary How Banks Create Money - Monetary Base - Total of currency in circulation plus bank reserves - is controlled by The Federal Reserve

35

Capital Requirements - Banks are required to have capital of at least 7% of total assets in addition to required reserves Discount Window - Banks can borrow money from The Federal Reserve at the “discount rate” if necessary How Banks Create Money - Monetary Base - Total of currency in circulation plus bank reserves - is controlled by The Federal Reserve

36

Money Multiplier - The total number of dollars created in the banking system for each additional dollar added to the monetary base Multiplier = 1/ rr Ex #1: If rr =.10 then 1/.10 = 10 x $1000 = $10,000 addition to the Money Supply Ex #2: If rr =.05 then 1/.05 = 20 x $1000 = $20,000 addition to the Money Supply

37

Module 26 - The Federal Reserve System: History & Structure What you will learn: The history of The Federal Reserve System The structure of The Federal Reserve System How The Federal Reserve responds to major financial crises

38

Module 26 - The Federal Reserve System: History & Structure The Creation of The Federal Reserve - The central bank of the United States that oversees the banking system and controls the monetary Base (money supply) - Created in 1913 to help control financial crises - given the sole power to issue currency Structure of the Federal Reserve - Board of Governors: - Seven members appointed by the president for 14 year terms - Chair(man) appointed every 4 years - Janet Yellen

- Created in 1913 to help control financial crises - given the sole power to issue currency Structure of the Federal Reserve - Board of Governors: - Seven members appointed by the president for 14 year terms - Chair(man) appointed every 4 years - Janet Yellen")

40

Module 26 - The Federal Reserve System: History & Structure The Creation of The Federal Reserve - The central bank of the United States that oversees the banking system and controls the monetary Base (money supply) - Created in 1913 to help control financial crises - given the sole power to issue currency Structure of the Federal Reserve - Board of Governors: - Seven members appointed by the president for 14 year terms - Chair(man) appointed every 4 years - Janet Yellen

- Created in 1913 to help control financial crises - given the sole power to issue currency Structure of the Federal Reserve - Board of Governors: - Seven members appointed by the president for 14 year terms - Chair(man) appointed every 4 years - Janet Yellen")

41

- 12 regional Federal Reserve Banks provide banking services and supervise the banks in their region

43

- 12 regional Federal Reserve Banks provide banking services and supervise the banks in their region The Federal Reserve Bank of New York carries out open-market operations and holds more gold than anywhere on earth

45

44

48

- 12 regional Federal Reserve Banks provide banking services and supervise the banks in their region The Federal Reserve Bank of New York carries out open-market operations and holds more gold than anywhere on earth Commercial Banks - Accepts deposits, make loans, and is covered by FDIC (Federal Deposit Insurance Corporation) Investment Banks - Trades in financial assets and is NOT covered by FDIC Savings & Loans (thrifts) - Deposit-taking bank, usually specializing in home loans Federal Reserve

Investment Banks - Trades in financial assets and is NOT covered by FDIC Savings & Loans (thrifts) - Deposit-taking bank, usually specializing in home loans Federal Reserve")

49

Savings & Loan Crisis of the 1980s - High inflation of late 70s lowered value of S&L assets and discouraged public from investing in low-interest paying S&Ls Congress de-regulated S&Ls allowing them to undertake more risky and long term investments - by early 1980s many had failed - FDIC paid over $124 billion - caused recession Financial Crisis of 2008 - Low interest rates caused a housing boom making subprime mortgage loans seemed safe - financial institutions sold shares in pools of mortgages. - when housing prices fell many defaulted on their mortgages and investors took heavy losses - investment companies failed

50

Module 27 - The Federal Reserve System: Monetary Policy What you will learn: The function of The Federal Reserve System The tools the Federal Reserve uses to serve its functions

51

Module 27 - The Federal Reserve System: Monetary Policy Functions of the Fed. - Provide Financial Services - Holds bank reserves, clears checks, provides cash, is the bank for the U.S. Government Regulate Banking Institutions - Regulates and supervises the banks within each region Maintain Stability of the Financial System - Maintains the integrity and stability of the financial system Conduct Monetary Policy - Control extreme fluctuations in the economy

52

The Reserve Requirement - Minimum percent of deposits that banks must hold on reserve with the Fed. - face penalties if not maintained Federal Funds Market - Allows banks to borrow reserves from banks with excess reserves at a set interest rate Federal Funds Rate - Interest rate set by the Fed for banks to borrow in the Federal Funds Market The Discount Rate - The interest rate the Fed charges banks on loans through the discount window

53

Open-market Operations - The Fed’s assets consists of short term Govt. bonds known as U.S. Treasury Bills The Fed buys or sells Treasury Bills (from commercial banks) - These transactions start the money multiplier in motion which increases or decreases the money supply

- These transactions start the money multiplier in motion which increases or decreases the money supply.")

55

Open-market Operations - The Fed’s assets consists of short term Govt. bonds known as U.S. Treasury Bills The Fed buys or sells Treasury Bills (from commercial banks) - These transactions start the money multiplier in motion which increases or decreases the money supply

- These transactions start the money multiplier in motion which increases or decreases the money supply.")

56

Module 28 - The Money Market What you will learn: What the the money demand curve is Why the Liquidity Preference Model determines the interest rate in the short run

57

Module 28 - The Money Market The Demand for Money - Firms and individuals want to hold a certain amount of money at any given time - what determines how much?

59

Module 28 - The Money Market The Demand for Money - Firms and individuals want to hold a certain amount of money at any given time - what determines how much? Short-term Interest Rates - Interest rates on financial assets that mature in a year or less Long-term Interest Rates - Interest rates on financial assets that mature a number of years in the future Money Demand Curve - Relationship between the interest rate and the quantity of money demanded by the the public

61

Module 28 - The Money Market The Demand for Money - Firms and individuals want to hold a certain amount of money at any given time - what determines how much? Short-term Interest Rates - Interest rates on financial assets that mature in a year or less Long-term Interest Rates - Interest rates on financial assets that mature a number of years in the future Money Demand Curve - Relationship between the interest rate and the quantity of money demanded by the the public

62

Shifts of Money Demand Curve - Money demand curve shifts just like ordinary demand curve - more or less money demanded at all interest rates

64

Shifts of Money Demand Curve - Money demand curve shifts just like ordinary demand curve - more or less money demanded at all interest rates Changes in Aggregate Price Level - Demand for money is proportional to the change in price level - prices increase 10%, demand for money increases 10% Changes in Real GDP - The greater the quantity of goods and services produced and sold - the greater the money demand Changes in Technology - ATMs, on-line transactions, debit cards, etc. make it less necessary to hold cash - shifts curve ???

65

Changes in Institutions - Demand shifts as banking regulations change allowing banks to offer more options and interest bearing assets Liquidity Preference Model of the Interest Rate - The interest rate is determined by the supply and demand for money - equilibrium interest rate Money Supply Curve - The quantity of money supplied by the Fed. - Supply Curve is vertical because the amount is chosen by the Fed.

67

Changes in Institutions - Demand shifts as banking regulations change allowing banks to offer more options and interest bearing assets Liquidity Preference Model of the Interest Rate - The interest rate is determined by the supply and demand for money - equilibrium interest rate Money Supply Curve - The quantity of money supplied by the Fed. - Supply Curve is vertical because the amount is chosen by the Fed.

68

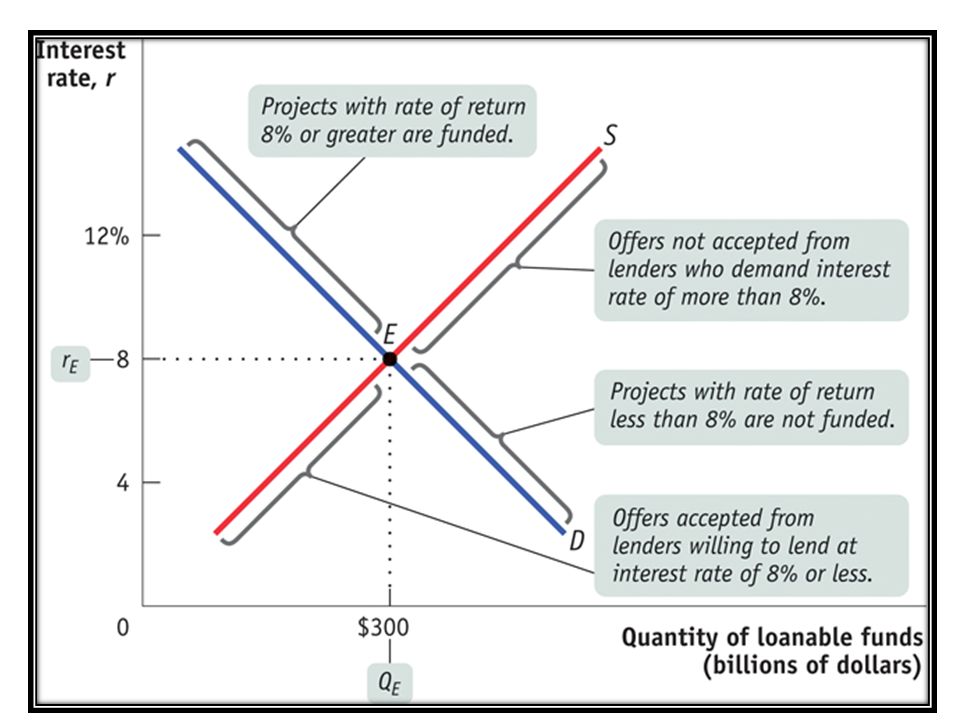

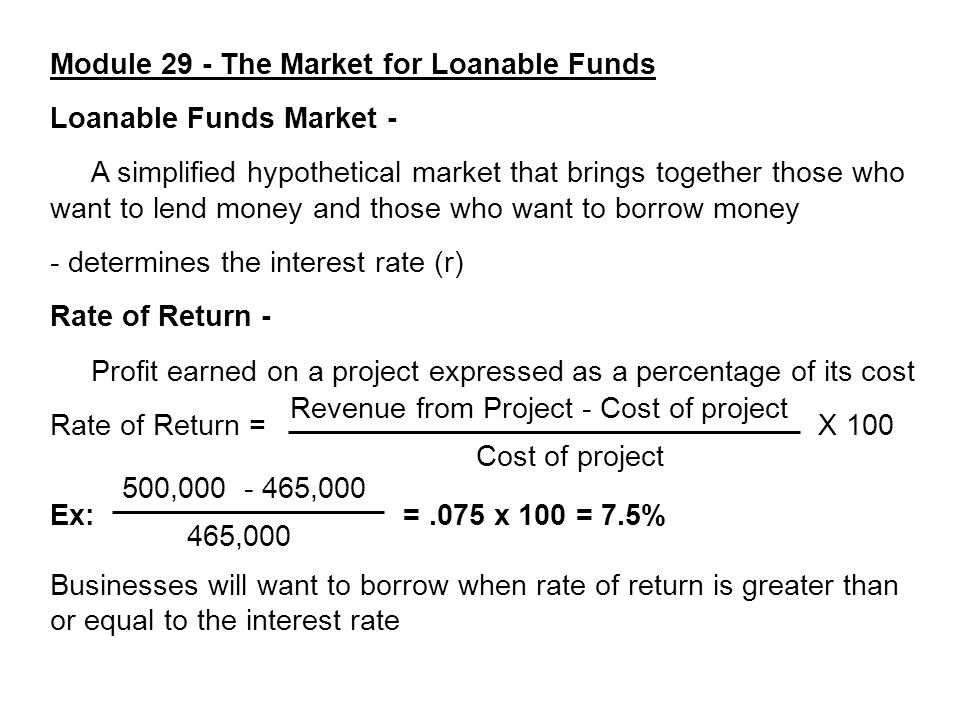

Module 29 - The Market for Loanable Funds What you will learn: How the loanable funds market matches savers and investors The determinates of supply and demand in the loanable funds market How the two models of interest rates can be reconciled

69

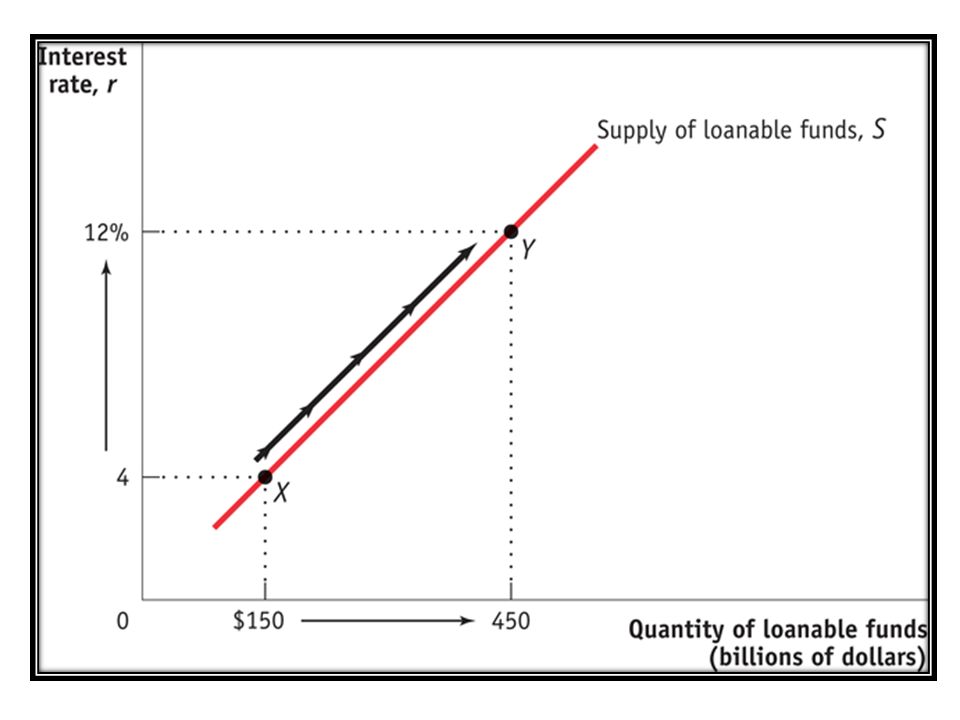

Module 29 - The Market for Loanable Funds Loanable Funds Market - A simplified hypothetical market that brings together those who want to lend money and those who want to borrow money - determines the interest rate (r) Rate of Return - Profit earned on a project expressed as a percentage of its cost Rate of Return = X 100 Ex: =.075 x 100 = 7.5% Businesses will want to borrow when rate of return is greater than or equal to the interest rate Revenue from Project - Cost of project Cost of project 500,000 - 465,000 465,000

Rate of Return - Profit earned on a project expressed as a percentage of its cost Rate of Return = X 100 Ex: =.075 x 100 = 7.5% Businesses will want to borrow when rate of return is greater than or equal to the interest rate Revenue from Project - Cost of project Cost of project 500, , ,000")

73

Module 29 - The Market for Loanable Funds Loanable Funds Market - A simplified hypothetical market that brings together those who want to lend money and those who want to borrow money - determines the interest rate (r) Rate of Return - Profit earned on a project expressed as a percentage of its cost Rate of Return = X 100 Ex: =.075 x 100 = 7.5% Businesses will want to borrow when rate of return is greater than or equal to the interest rate Revenue from Project - Cost of project Cost of project 500,000 - 465,000 465,000

Rate of Return - Profit earned on a project expressed as a percentage of its cost Rate of Return = X 100 Ex: =.075 x 100 = 7.5% Businesses will want to borrow when rate of return is greater than or equal to the interest rate Revenue from Project - Cost of project Cost of project 500, , ,000")

74

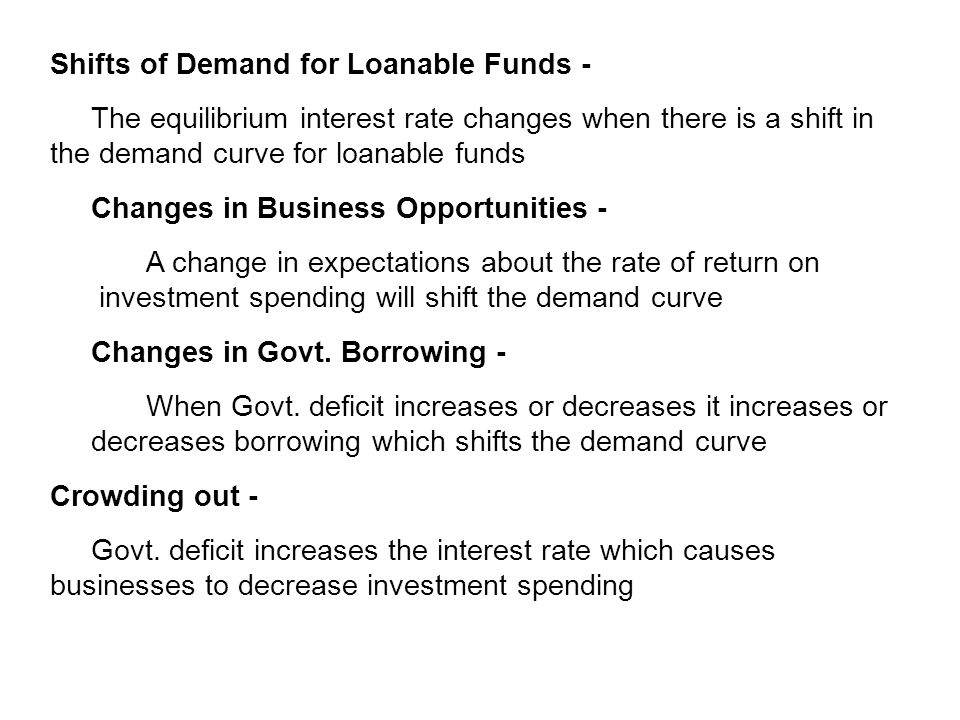

Shifts of Demand for Loanable Funds - The equilibrium interest rate changes when there is a shift in the demand curve for loanable funds Changes in Business Opportunities - A change in expectations about the rate of return on investment spending will shift the demand curve Changes in Govt. Borrowing - When Govt. deficit increases or decreases it increases or decreases borrowing which shifts the demand curve

76

Shifts of Demand for Loanable Funds - The equilibrium interest rate changes when there is a shift in the demand curve for loanable funds Changes in Business Opportunities - A change in expectations about the rate of return on investment spending will shift the demand curve Changes in Govt. Borrowing - When Govt. deficit increases or decreases it increases or decreases borrowing which shifts the demand curve Crowding out - Govt. deficit increases the interest rate which causes businesses to decrease investment spending

78

Shifts of the Supply of Loanable Funds - Changes in Private Savings - As savings increase, the available funds to loan increases - as savings decrease, available funds to loan decreases Changes in Capital Inflows - As foreign investment in U.S. markets changes - this changes available funds to loan

80

Shifts of the Supply of Loanable Funds - Changes in Private Savings - As savings increase, the available funds to loan increases - as savings decrease, available funds to loan decreases Changes in Capital Inflows - As foreign investment in U.S. markets changes - this changes available funds to loan Inflation and Interest Rates - The true cost of borrowing is the real interest rate, not the nominal interest rate Real interest rate = Nominal interest rate - Inflation rate - Expectations about future inflation shifts demand and supply

81

Fisher Effect - An increase in expected future inflation drives up the nominal interest rate

83

Fisher Effect - An increase in expected future inflation drives up the nominal interest rate Interest Rate in the Short-run - Increase in the money supply leads to a fall in the interest rate - Decrease in money supply leads to an increase in interest rate

85

Fisher Effect - An increase in expected future inflation drives up the nominal interest rate Interest Rate in the Short-run - Increase in the money supply leads to a fall in the interest rate - Decrease in money supply leads to an increase in interest rate Interest Rate in the Long-run - A change in the money supply does not effect the interest rate in the long run - long-run interest rate is determined by the supply and demand for loanable funds

87

Fisher Effect - An increase in expected future inflation drives up the nominal interest rate Interest Rate in the Short-run - Increase in the money supply leads to a fall in the interest rate - Decrease in money supply leads to an increase in interest rate Interest Rate in the Long-run - A change in the money supply does not effect the interest rate in the long run - long-run interest rate is determined by the supply and demand for loanable funds

88

87 The End

Similar presentations