Download presentation

Presentation is loading. Please wait.

1

What’s Happening? We are catching up to the schedule on the course syllabus. ISMA meeting scheduled for today has been postponed for a week—Jan 28, 4:30 to 5:30 College 8, room Speaker is JP LeBlanc, Director of RAD Development, Borland

2

Chapter 4 Introduction Airline Industry Analysis

3

Major Chapter Topics Airline Industry analysis using the Porter Competitive Model as a clearly defined industry. Revisit Business Strategy Model. Lessons Learned from Consistently Profitable Carriers. Is American Airlines the right standard for the US industry? Importance of Information Technology to the Airline Industry.

4

Consistently Profitable Airlines

Singapore Airlines Geographic Location, National Strategies, Leadership in IT, Competitive Strategies Southwest Airlines Aircraft Utilization, Focus on City Pairs, Point-to-Point Route Structure, Corporate Culture, Cost Savings in Reservation System

5

American Airlines Largest airline in the US versus United while also a contender on the international level. A premium service airline with a hub and stoke route structure. Has consistently been recognized as an industry leader. Currently faces the same financial problems as other major carriers. Faces challenge of dealing with strong unions.

6

Porter Competitive Model

Airline Industry Analysis - North American Market Potential New Entrants Foreign Carriers Regional Carrier Start ups Cargo Carrier Business Strategy Change Aircraft Manufacturers Aircraft Leasing Companies Labor Unions Food Service Companies Fuel Companies Airports Local Transportation Service FAA Hotels Intra-Industry Rivalry SBU: American Airlines Rivals: United, Delta, US Air, Northwest, Southwest Bargaining Power of Suppliers Bargaining Power of Buyers Travel Agents Business Travelers Federal Government Pleasure Travelers Charter Service U.S. Military Cargo and Mail Alternate Travel Services Fast Trains Boats Private Transportation Videoconferencing Groupware Substitute Products and Services Figure 4-2

7

Business Strategy Model - Airline Industry ROUTES AND ROUTE STRUCTURE

PRODUCT/SERVICES Scheduled Passengers Charter Services Cargo Mail Air Express MARKETS Europe North American Pacific Rim Latin American ROUTES AND ROUTE STRUCTURE Short Haul Long Haul Hub and Spoke Point to Point FARE STRATEGY Modified compared to the example in the textbook. Low Fare Premium Fare COMPANY STRUCTURE Independent Alliances INFORMATION SYSTEMS FOCUS Passengers Operations Logistics Business Figure 4-1

8

Benefits of Information Systems to American Airlines

Convenience to Customers Reservation System, Request hotels, car. Knowledge of Customers Frequent-Flyer Program: AAdvantage. Providing a Foundation for Other Systems Yield-Management System. Building a Base for Other Businesses American designed systems for others.

9

Airline Industry Value Chain

FIRM INFRASTRUCTURE -Financial Policy - Accounting -Regulatory Compliance - Legal - Community Affairs HUMAN RESOURCE MANAGEMENT Flight, route and yield analyst training Pilot Training Safety Training Baggage Handling Training Agent Training In-flight Training Product Development Market Research Computer Reservation System, In-flight System Flight Scheduling System, Yield Management System Baggage Tracking System TECHNOLOGY DEVELOPMENT Information Technology Communications PROCUREMENT Route Selection Passenger Service System Yield Management System (Pricing) Fuel Flight Scheduling Crew Scheduling Facilities Planning Aircraft Acquisition Ticket Counter Operations Gate Operations Aircraft On-board Service Baggage Handling Ticket Offices Baggage System Flight Connections Rental Car and Hotel Reservation System Promotion Advertising Advantage Program Travel Agent Programs Group Sales Lost Baggage Service Complaint Follow-up INBOUND LOGISTICS OPERATIONS OUTBOUND LOGISTICS MARKETING AND SALES SERVICE Figure 4-3 Adapted with the permission of Michael E. Porter from Competitive Advantage: Creating and Sustaining Superior Performance, copyright 1985 by Michael E. Porter.

Fuel. Flight Scheduling. Crew Scheduling. Facilities Planning. Aircraft Acquisition. Ticket Counter. Operations. Gate Operations. Aircraft. On-board Service. Baggage Handling. Ticket Offices. Baggage System. Flight. Connections. Rental Car and. Hotel Reservation. System. Promotion. Advertising. Advantage. Program. Travel Agent. Programs. Group Sales. Lost Baggage Service. Complaint Follow-up. INBOUND. LOGISTICS. OPERATIONS. OUTBOUND. LOGISTICS. MARKETING. AND SALES. SERVICE. Figure 4-3. Adapted with the permission of Michael E. Porter from Competitive Advantage: Creating and Sustaining Superior. Performance, copyright 1985 by Michael E. Porter.")

10

Conclusions The Airline Industry is a vivid example of the dynamics of the market that it serves. Shows that establishing strategies dictated by the market is critical. Once the right strategies have been identified, information systems can play an important supporting role.

11

Porter Competitive Model and the Airline Industry

Chapter 4 Porter Competitive Model and the Airline Industry

12

2003 - A Hundred Years of Flight

Aviation is celebrating its centennial year. From its first brave beginnings the civil aviation industry remains dynamic and although some of the priorities have changed, the spirit and passion remain. Some priorities are not new: safety, the need for efficient operations, adequate capacity to meet growth and, of course, customer satisfaction. Other priorities have gained prominence in recent years – security, war risk insurance and environmental concerns – and will remain important in the coming years.

13

This industry is always in the grip of its dumbest competitors.

Robert Crandall Former CEO American Airlines

14

We must look at the world as it is versus how airlines would like it to be.

Robert L. Crandall And as government officials, politicians and consumers would like it to be.

15

Airline Industry Goals

Public Service. (Service to Customers) Return to Investors. Country Strategic Resource. Are these consistent or in frequent conflict?

Return to Investors. Country Strategic Resource. Are these consistent or in frequent. conflict")

16

Airline Profitability

Profitability = [yield X load factor] - cost In order to survive and profit in this tough environment, airlines attempt to manipulate three main variables: Cost, calculated as total operating expenses divided by available seat miles (ASM) Yield, calculated as total operating revenues divided by the number of revenue passenger miles (RPM) Load Factor, calculated as the ratio between RPMs and ASMs, which measures capacity utilization.

Yield, calculated as total operating revenues divided by the number of revenue passenger miles (RPM) Load Factor, calculated as the ratio between RPMs and ASMs, which measures capacity utilization.")

17

United Flight 815 Chicago to LAX, October 31, 2001

204 tickets were sold and 186 people showed up. 68 passengers originated in Chicago and 118 were from connecting flights. 97 passengers terminated at LAX, 89 continued on another flight. Of the 33 passengers that were only Chicago-LAX there were 27 different fares: A frequent flyer passenger paid nothing. A 1st class passenger paid $1, on the day of the flight. A coach passenger paid $ on the day of the flight. A cash fare passenger paid $87.21 twenty-nine days in advance .

18

Change, Challenge and Competition

The National Commission to Ensure a Strong Competitive Airline Industry Change, Challenge and Competition A Report to the President and Congress August 1993

19

Airline Industry Report

The air transportation system has become essential to the economic progress for the citizens and businesses of this nation.

20

The commission questioned some of the most basic assumptions that have formed the foundation of policy toward this industry--and behavior within it--for the past half century.

21

It also questioned whether the

airline industry has basic structural problems or if it is just a collection of poorly managed companies.

22

Commission Findings The Airline Industry is more competitive than before deregulation in 1978. Travelers and shippers are charged less than in 1978. The Airline Industry has never made a sustained, substantial return on investment. It lost huge amounts of money from 1990 to 1993. It canceled many aircraft orders shortly after an unprecedented buying binge. Its freedom to compete in international markets is uncertain because of government restrictions.

23

Commission Conclusions

For the U.S. to prosper in a global marketplace the airline industry must: Be efficient and technologically superior. Have the financial strength to respond to rapid change and opportunity. Efficiently move people, products and services to markets, wherever they exist.

24

Recommendations Efficiency: Reinvent the FAA.

Financial Health: Deal with factors that impact the financial health of the industry. Access to Foreign Markets: Replace the current bilateral system with a multi-national regime.

25

To return their balance sheets to

respectability, most airlines would have to achieve profit margins that are almost unprecedented in their history, and sustain those margins for years.

26

September 11 Impact An absolute disaster for the industry.

27

1990-1993 Was a Disaster! The Gulf War.

The general decline in the world economy. Aircraft fuel price increases. Wages, work rules and work patterns. Chapter 11 bankruptcy airlines. Excess capacity. A very capital intensive business. Too many years as regulated airlines.

28

Airline Industry The shock of September 11th has forced airlines to face an awkward fact: in some respects, aviation is a declining industry. Nov. 22, 2001 The Economist

29

Decline in Air Travel At Thanksgiving in 2000 a record 2.2 million Americans took a flight to spend the holiday with family and friends. Air traffic in October and November 2001 was down by about 25% compared to the previous year in the world's biggest aviation market, thanks to a combination of recession and the attacks on September 11th.

30

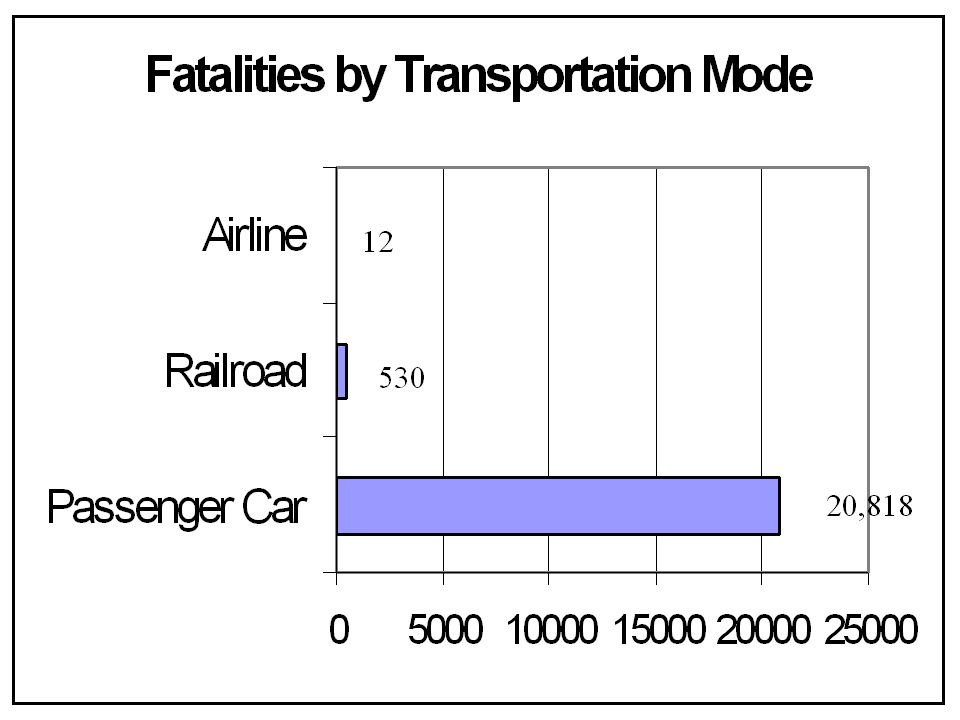

International Travel International travel from America has been hit even harder: the number of Americans flying across the Atlantic is down by over 30%. Never mind that more people are killed on America's roads every three months than have died in the entire history of commercial aviation.

32

Load Factors Despite cutting capacity, the big American airlines are still flying with planes barely 60% full—a figure that would be much lower were it not for hefty discounts. Boeing and Airbus, the two manufacturers of large jetliners, are offering airlines special financing deals to pay for their purchases in order to stave off outright cancellations. The last time the airlines were in such straits, during the Gulf war and recession in , it took them four years to return to profit, even though traffic recovered within a year.

33

European Airlines The situation in Europe is no better.

Two flag carriers, Swissair and Sabena, have collapsed since the terrorist attacks. Other big carriers, such as British Airways (BA) and KLM, are in major financial trouble. Traffic within Europe fell by over 10% in September and October 2001, while traffic from Europe to America and Asia fell by 35% and 17% respectively.

and KLM, are in major financial trouble. Traffic within Europe fell by over 10% in September and October 2001, while traffic from Europe to America and Asia fell by 35% and 17% respectively.")

34

Financial Picture Although air travel, measured by number of passenger-kilometers flown, has long risen faster than economic growth, airline revenues have lagged world GDP growth for the past 20 years in real terms, Revenues and profits per seat have been falling because of greater competition springing from deregulation, first in America and then within Europe and across the Atlantic. Even before the latest slump only a third of mainstream airlines in Europe, America and Asia earned enough to cover their cost of capital, which is 8% on average.

35

Looking for Options In most industries, such a situation would quickly lead to mergers. But this is not so easy for airlines, hemmed in as they are by national ownership rules and rigid international regulation of routes. America's airlines are retreating to their strongholds in the hub airports they dominate, such as Dallas-Fort Worth (American) and Atlanta (Delta). Most airlines have cut at least one “wave” of coordinated flights in and out of their hubs. If additional security checks are introduced for transferring passengers before they board their outbound flights, and the handling of such travelers thus slows down, some observers expect the airlines to switch to fewer flights in larger aircraft.

and Atlanta (Delta). Most airlines have cut at least one wave of coordinated flights in and out of their hubs. If additional security checks are introduced for transferring passengers before they board their outbound flights, and the handling of such travelers thus slows down, some observers expect the airlines to switch to fewer flights in larger aircraft.")

36

Dropping Point-to-Point Flights

The biggest effect has been for airlines to drop non-stop “point-to-point” flights rather than those that go through hubs. The network economics of hubs becomes more attractive for big carriers when times are tough. A study of America's changed airline-route map shows that large carriers are cutting non-stop flights to cities where they do not operate hubs by more than they are trimming hub flights.

37

Unions and Vendors The industry's woes will also force airlines to get tough with unions and suppliers over restrictive practices that raise their costs.

38

European Changes In Europe, where the failure of Swissair and Sabena has shown that there is room for only a handful of mainstream carriers rather than today's 14, a shake-out is already under way.

39

Airlines: How Ugly? The outlook is either bad or outright ugly.

Two problems: Post 9/11 fears and increased hassles based on new security measures.

40

US Airline Industry Must Restructure or Die Aviation Week & Space Technology November 2002

Low-Cost Airlines, Not September 11, Have Transformed Industry Fundamentals "When people say the traditional industry model is broken, they are moving their jaw without putting their brain in gear," responds former American Airlines CEO Robert Crandall. He added that he is skeptical that the industry will ever be competitive as long as there are so many carriers selling what has evolved into a commodity product.

41

Aviation Week Contentions

A collapse in pricing power and a fundamental shift in the buying behavior of business travelers, coupled with fierce competition from low-cost airlines, is forcing U.S. major hub- and-spoke carriers to restructure their operations or face the prospect of eventually going out of business. Airline executives and industry analysts note that the September 11 attacks, while devastating, are not the root cause of the financial crisis gripping major network carriers. The crux of the problem is a combination of excessive costs in relation to carriers' current and projected revenues, an imbalance between the supply and demand for available airline seats, and an inability to boost air fares.

42

Corrective Actions U.S. airlines have axed more than 70,000 jobs. In addition, some unions representing many of the industry's employees have made a commitment to work with management to help the carriers compete more effectively with low-cost rivals. It will take much more than concessions by labor for major U.S. airlines to solve their financial problems. The financial problems carriers are suffering could actually worsen in coming months if the U.S. goes to war with Iraq. The U.S. airline industry cannot take another major hit. A brief war doesn't qualify but a messy, extended war or another significant domestic terrorist attack does.

43

Airline Industry US Market Share

Based on current trends, the domestic market share held by the six major US airlines (American, Continental, Delta, Northwest, United and US Airways) plus Alaska Airlines will drop from 75% in 2002 to 62% in 2010—and 45% by , according to an industry projection. Southwest could pass American to become the largest U.S. airline by 2013, and JetBlue could pass Delta to become the third largest by 2020.

plus Alaska Airlines will drop from 75% in 2002 to 62% in 2010—and 45% by 2020, according to an industry projection. Southwest could pass American to become the largest U.S. airline by 2013, and JetBlue could pass Delta to become the third largest by")

44

Industry Structure Problems

The fact that low-cost carriers have been able to mature this far says as much about what's wrong with the majors as it does about what's right with their low-cost counterparts, and begs the question: does the underlying strategy or business model employed by the large hub-and-spoke airlines still work? Analysts and other industry observers believe it does, but to function properly carriers must reduce their costs and restore the balance between supply and demand.

45

A Sobering Fact Before September 11, 2001, the global industry was showing a net loss on international services of around $3 billion.

46

Corrective Actions Reduced capacity.

Older aircraft may never return to service. Reduced wage pressures. Continued joint agreements. Discounted tickets and more travel packages.

47

Code Sharing Agreements

The US Transportation and Justice Departments approved a pact Friday that will let Delta Air Lines, Continental Airlines and Northwest Airlines share access to each other's routes. The code-share agreement allows each carrier to market the others' routes as its own. One Northwest flight, for instance, might also have a Continental flight number and a Delta flight number. The agreement will be the biggest in the industry. US Airways and United Airlines have a similar agreement and Continental have some shared routes in a deal that dates to 1998.

48

Code Sharing Agreements

It's an especially appealing arrangement to frequent fliers who prefer to build up miles on one airline while flying all three. The government placed several conditions on the deal. Specifically, the DOT said 60 percent of any new code-sharing routes must serve those areas of the country that are considered under-served. It also bans anti-competitive practices like coordinated pricing or shared decisions about route planning and capacity.

49

American Airlines American Airlines asked its employees to come to the aid of the carrier, saying they have no time to waste if they want to keep the financially strapped airline in business. The plea comes as two major unions at the world's largest carrier consider a company request to freeze their wages and another union is trying to hammer out a new contract. Company management says carriers that have reduced costs through bankruptcy protection have put even more pressure on AMR.

50

American Airlines American asked union leaders to start holding weekly meetings, as early as next, week with company management in a collaborative process. The move comes as United Airlines is trying to squeeze large wage cuts from its employees as it undergoes restructuring under bankruptcy protection. About a month ago, American asked its employees to forgo pay increases. The union that represents flight attendants at American said it is taking a close look at the company's finances and may decide at the end of this month whether to forgo pay increases scheduled for this year.

51

Continuing Concerns Fuel costs

Decisions regarding passenger services like whether to charge for food, the need for more electronic capabilities. Upgrading aircraft. Route strategies. Union relations. Relations with travel agents.

52

Porter Competitive Model

Airline Industry Analysis - North American Market Potential New Entrants Foreign Carriers Regional Carrier Start ups Cargo Carrier Business Strategy Change Aircraft Manufacturers Aircraft Leasing Companies Labor Unions Food Service Companies Fuel Companies Airports Local Transportation Service FAA Hotels Intra-Industry Rivalry SBU: American Airlines Rivals: United, Delta, US Air, Northwest, Southwest Bargaining Power of Suppliers Bargaining Power of Buyers Travel Agents Business Travelers Federal Government Pleasure Travelers Charter Service U.S. Military Cargo and Mail Alternate Travel Services Fast Trains Boats Private Transportation Videoconferencing Groupware Substitute Products and Services Figure 4-2

53

Business Strategy Model - Airline Industry ROUTES AND ROUTE STRUCTURE

PRODUCT/SERVICES Scheduled Passengers Charter Services Cargo Mail Air Express MARKETS Europe North American Pacific Rim Latin American ROUTES AND ROUTE STRUCTURE Short Haul Long Haul Hub and Spoke Point to Point FARE STRATEGY Modified compared to the example in the textbook. Low Fare Premium Fare COMPANY STRUCTURE Independent Alliances INFORMATION SYSTEMS FOCUS Passengers Operations Logistics Business Figure 4-1

54

Airline Industry Value Chain

FIRM INFRASTRUCTURE -Financial Policy - Accounting -Regulatory Compliance - Legal - Community Affairs HUMAN RESOURCE MANAGEMENT Flight, route and yield analyst training Pilot Training Safety Training Baggage Handling Training Agent Training In-flight Training Product Development Market Research Computer Reservation System, In-flight System Flight Scheduling System, Yield Management System Baggage Tracking System TECHNOLOGY DEVELOPMENT Information Technology Communications PROCUREMENT Route Selection Passenger Service System Yield Management System (Pricing) Fuel Flight Scheduling Crew Scheduling Facilities Planning Aircraft Acquisition Ticket Counter Operations Gate Operations Aircraft On-board Service Baggage Handling Ticket Offices Baggage System Flight Connections Rental Car and Hotel Reservation System Promotion Advertising Advantage Program Travel Agent Programs Group Sales Lost Baggage Service Complaint Follow-up INBOUND LOGISTICS OPERATIONS OUTBOUND LOGISTICS MARKETING AND SALES SERVICE Figure 4-3 Adapted with the permission of Michael E. Porter from Competitive Advantage: Creating and Sustaining Superior Performance, copyright 1985 by Michael E. Porter.

Fuel. Flight Scheduling. Crew Scheduling. Facilities Planning. Aircraft Acquisition. Ticket Counter. Operations. Gate Operations. Aircraft. On-board Service. Baggage Handling. Ticket Offices. Baggage System. Flight. Connections. Rental Car and. Hotel Reservation. System. Promotion. Advertising. Advantage. Program. Travel Agent. Programs. Group Sales. Lost Baggage Service. Complaint Follow-up. INBOUND. LOGISTICS. OPERATIONS. OUTBOUND. LOGISTICS. MARKETING. AND SALES. SERVICE. Figure 4-3. Adapted with the permission of Michael E. Porter from Competitive Advantage: Creating and Sustaining Superior. Performance, copyright 1985 by Michael E. Porter.")

55

Benefits of Information Systems to American Airlines

1. Convenience to Customers. 2. Knowledge of Customers. 3. Providing a foundation for other systems. 4. Building a base for other businesses.

56

Four Three Consistently Profitable Airlines

1. Singapore Airlines 2. Cathay Pacific 3. British Airways 4. Southwest Airlines

57

Singapore Airlines Consistently profitable but experiencing profit pressures. Winner of multiple awards for “airline excellence.” An extension of the country strategy to be the business and travel gateway to Southeast Asia. An impressive travel infrastructure. Leader of the Orient Airlines Association (OAA) Abacus reservation system. Price collusion on major routes. Nervous regarding U.S. carrier price competition.

Abacus reservation system. Price collusion on major routes. Nervous regarding U.S. carrier price competition.")

58

Why SIA is So Good! Clarity and Commitment (to customer service).

Continuous Training. Internal Communications. Consistent External Communications. Connection with Customers. Benchmarking. Rewards and Recognition. Professionalism, Pride and Profits.

59

Southwest Airlines A U.S. carrier success story.

Commuter airline that concentrates on city pairs. (Average flight is 400 miles or less and takes less than one hour) CEO Herb Kelleher, a Connecticut attorney turned Texan, had the best labor relations in the industry and an excellent company culture. Lowest cost structure in the industry. Company vision was to provide low cost airline service to an increasingly larger number of people. Objective to minimize reservation costs.

CEO Herb Kelleher, a Connecticut attorney turned Texan, had the best labor relations in the industry and an excellent company culture. Lowest cost structure in the industry. Company vision was to provide low cost airline service to an increasingly larger number of people. Objective to minimize reservation costs.")

60

A Strength of Southwest Airlines

1. Focus. 2. Focus. 3. Focus

61

Best Airlines for Business Travelers

11. Finnair 12. British Airways 13. Alaska 14. Air France 15. Varig 16. Aer Lingus 17. Kiwi 18. Air Canada 19. American ** 20. Delta** Singapore Airlines Swiss Air Cathay Pacific Midwest Express ** Japan Airlines Quantas ANA Virgin Atlantic Lufthansa KLM-Royal Dutch Source: Zagat Survey of Frequent Flyers

62

Deregulated But Very Regulated

Safety factors. Air traffic controllers. Impact on constituents. International routes.

63

Computer Reservation System:

Business Traveler Choice? Personal Traveler Choice? Ticket-less Versus No Reservation?

64

Airline Alliances The Star Alliance is the largest of the major groupings. Consisting of 15 airlines led by United Air Lines and Lufthansa. Star serves about 815 destinations in more than 130 countries. Oneworld, which is eclipsed by only Star among the major airline alliances, is led by British and American Airlines. Eight airlines offer service to 550 destinations in more than 130 countries. SkyTeam is quickly becoming a major alliance player by serving more than 450 destinations in nearly 100 countries. Led by Air France and Delta, SkyTeam has also consolidated cargo services.

65

Interplay among government regulations,

airline strategies, and airplane capabilities shapes the evolution of world aviation. Boeing Corp.

66

Barriers to Entry Access to airports continues to be impeded by:

(1) Federal limits on takeoff and landing slots at the major airports in Chicago, New York, and Washington (2) Long-term, exclusive-use gate leases (3) “Perimeter Rules” prohibiting flights at New York’s LaGuardia and Washington’s National airports that exceed a certain distance.

Federal limits on takeoff and landing slots. at the major airports in Chicago, New York, and Washington. (2) Long-term, exclusive-use gate leases. (3) Perimeter Rules prohibiting flights at New York’s LaGuardia and Washington’s National airports that exceed a certain distance.")

67

US Industry Strength Fifteen major US carriers represent the following significance in the world-wide airline industry: 29% of the aircraft 46% of the employees 32.5% of the the 2000 passenger miles Based on a number of years of operating in a deregulated environment within the US that forced them to compete in a very tough market.

68

The Bad News Cumulative Net Profit of Scheduled US Airlines:

Started in 1938 1999 – 15.6 billion profit 1970 – 2.2 billion profit 1980 – 5.8 billion profit 1989 – 8.2 billion profit 1994 – 4.8 billion loss 1997 – 5.4 billion profit 1998 – 10.3 billion profit 2000 – 18.1 billion profit 2001 – 12 billion profit

69

Airline Industry Conclusions

It is a vivid example of the dynamics of the markets that it serves. Establishing strategies dictated by the market is critical. Once the right strategies have been identified, information systems can play an important supporting role.

70

Possible Exam Questions

1. Identify an industry where information systems act as a significant barrier to entry and explain the significance of this barrier. 2. Identify and explain the two basic strategies and three supporting strategies used by intra-industry rivals. 3. What is the primary benefit to be derived through the use of the Porter Value Chain? 4. Explain the logic and growth as a competitive strategy and provide two company examples where this was a key strategy.

Similar presentations