Download presentation

Presentation is loading. Please wait.

1

Enterprise Accounting: Key Questions Chapter 18 How are enterprises defined? How are income and expenses allocated by enterprise? How are internal transactions made?

2

Divide Farm into Enterprises (profit centers) Commodity corn, alfalfa, beef cows, sheep Stages farrowing, nursery, finishing By production cycle (crop year) Cost Centers (machinery, labor)

Commodity corn, alfalfa, beef cows, sheep Stages farrowing, nursery, finishing By production cycle (crop year) Cost Centers (machinery, labor)")

3

Assign Income and Expenses 1. Use account codes to assign direct income and expenses n Seed corn631 n Soybean seed632 n Alfalfa seed634 2. Allocate “overhead” expenses among enterprises n By % of gross income n By % of other expenses n By acres

4

3. Include Internal Transactions raised feed from crops to livestock manure from livestock to crops machinery services do not affect whole farm income or expenses

5

4. Include inventory changes or other accrual adjustments if you summarize by accounting year 5. Not necessary by production cycle

6

Profit and Loss Statement for Farmsim Income Total Crops Hogs Cattle Sales $421,473 $49,117 $105,427 $266,929 Ins payments 0 0 Inventory chg -46,297 21,650 1,653 -69,600 Gross income 375,176 70,767 107,080 197,329 Feed purchased -77,013 0 -42,323 -34,690 Raised crops fed 0 30,642 -10,843 -19,800 Livestock purch -94,000 -1,600 -92,400 Value farm Prod 204,162 101,409 52,314 50,439

7

Verifying Inventories: Crops Sources = + Beginning inventory + Purchases + Production Uses Ending inventory Sold Fed Spoilage Used for seed

8

Verifying Inventories: Livestock Sources = + Beginning inventory + Purchases + Production + Transferred in Uses + Ending inventory + Sales + Death loss + Transferred out

9

Farm Business Analysis—Ch.18 What are the strengths and weaknesses of the farm business? How can we measure how well the farm is doing?

10

Which farm would you prefer? Farm A Net worth $200,000 Labor12 months Net income $30,000 Farm B Net worth $400,000 Labor24 months Net income $50,000

11

What Affects Net Farm Income and Cash Flow? Size Efficiency

12

Size or Scale of the Farm Resources Acres Cows or sows No.of layers Total assets--$ Number of workers Production Pigs sold Cattle fed out Bushels sold Lbs. of milk Gross sales--$

13

Efficiency = production per unit of resources Physical efficiency bushels per acre lbs. milk per cow pigs per sow per year lambs per ewe pounds of feed per lb. of gain

14

Economic Efficiency (value of product per unit or $ of resource) Crop value per acre--$ Asset turnover ratio--% = gross income / total assets Livestock returns per $ of feed Gross income per person (FTE)

Crop value per acre--$ Asset turnover ratio--% = gross income / total assets Livestock returns per $ of feed Gross income per person (FTE)")

15

Economic efficiency also depends on: Value of Product (marketing) Sale price Quality Time Place Cost of Resources Seed, chemicals Cash rent Machinery, fuel Wages Feed

Sale price Quality Time Place Cost of Resources Seed, chemicals Cash rent Machinery, fuel Wages Feed")

16

Economic Efficiency = Units of output x selling price Units of resource x purch.price Ex.: crop value per $ rent paid 160 bu. corn x $2.25/bu. price 1 acre x $145 per acre = $2.48 per $1 spent on rent

17

Economic Efficiency Physical efficiency Marketing Cost of resources

18

Standards of Comparison Budgets Historical records for the same farm Current records from comparable farms

19

Choosing the Right Enterprises Fit the location Fit the operator Fit the resources

20

Net Farm Income also depends on how many of your resources you contribute yourself. Operator labor instead of hired labor. Net worth capital instead of debt. Owned land instead of rented. Net Farm Income is a return to operator labor, net worth and management.

21

Financial Structure Solvency Liquidity Profitability

22

SOLVENCY: Comparing assets to liabilities Net worth - $ Debt-to-asset ratio (or other ratio) Debt-to-asset ratios of 30 % to 40 % are typical, though many farms have no debt.

Debt-to-asset ratios of 30 % to 40 % are typical, though many farms have no debt.")

23

LEVERAGE: degree in debt Total debt-to-asset ratio low averagehigh High rates of profitability or low interest rates allow higher leverage to be sustained.

24

Liquidity (having cash when needed ) Current ratio = current assets current liabilities Working capital = (current assets - current liabilities)

Current ratio = current assets current liabilities Working capital = (current assets - current liabilities)")

25

LIQUIDITY Current ratio should be 2.0 or better Farms with continuous sales can have 1.5, but farms with infrequent sales may need 3.0 Working capital typically equals 25 % to 35 % of annual gross revenue Dairy may be as low as 20% of gross revenue, cash grain as high as 50%

26

Profitability (income and expenses) Net farm income value of unpaid labor ($/year) interest on owner equity (% interest rate x net worth) = Return to management These are opportunity costs

Net farm income value of unpaid labor ($/year) interest on owner equity (% interest rate x net worth) = Return to management These are opportunity costs")

27

Example Net farm income - value of unpaid labor (15 months @ $2,000) - value of owner equity ($300,000 net worth @ 5%) = Return to management $65,000 $30,000 $15,000 $20,000

- value of owner equity ($300,000 net 5%) = Return to management $65,000 $30,000 $15,000 $20,000")

28

Profitability--% Return on Equity--% = (NFI – unpaid labor) / farm net worth Return on debt capital (interest) Interest paid for the year / total liabilities Return on Assets--% (NFI – unpaid labor + interest expense paid) Total farm assets ROA is an average of ROE and the interest rate.

/ farm net worth Return on debt capital (interest) Interest paid for the year / total liabilities Return on Assets--% (NFI – unpaid labor + interest expense paid) Total farm assets ROA is an average of ROE and the interest rate.")

29

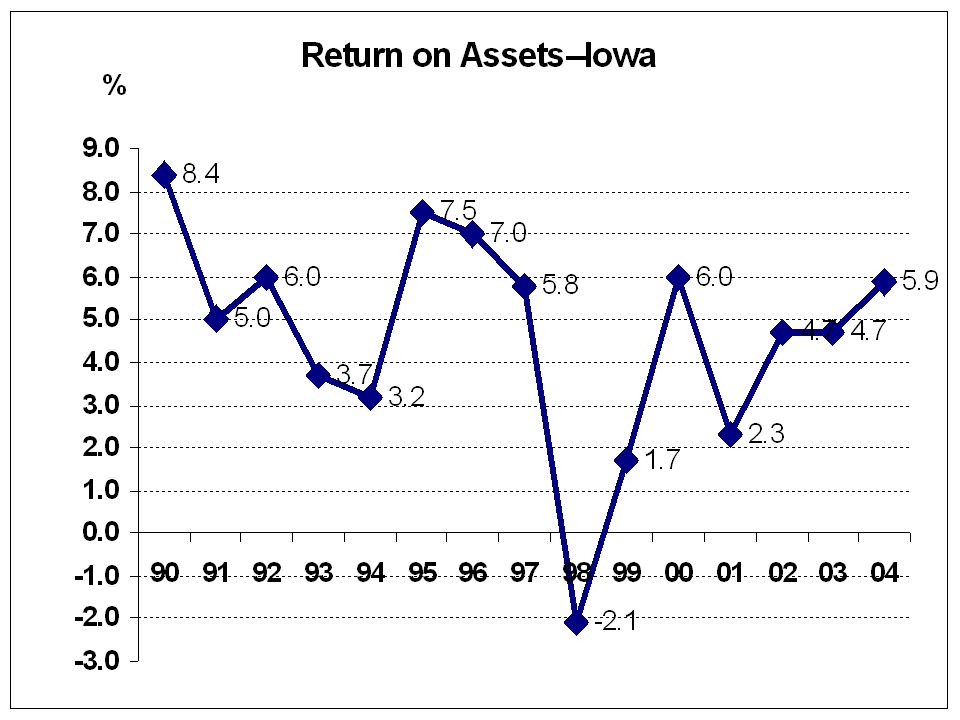

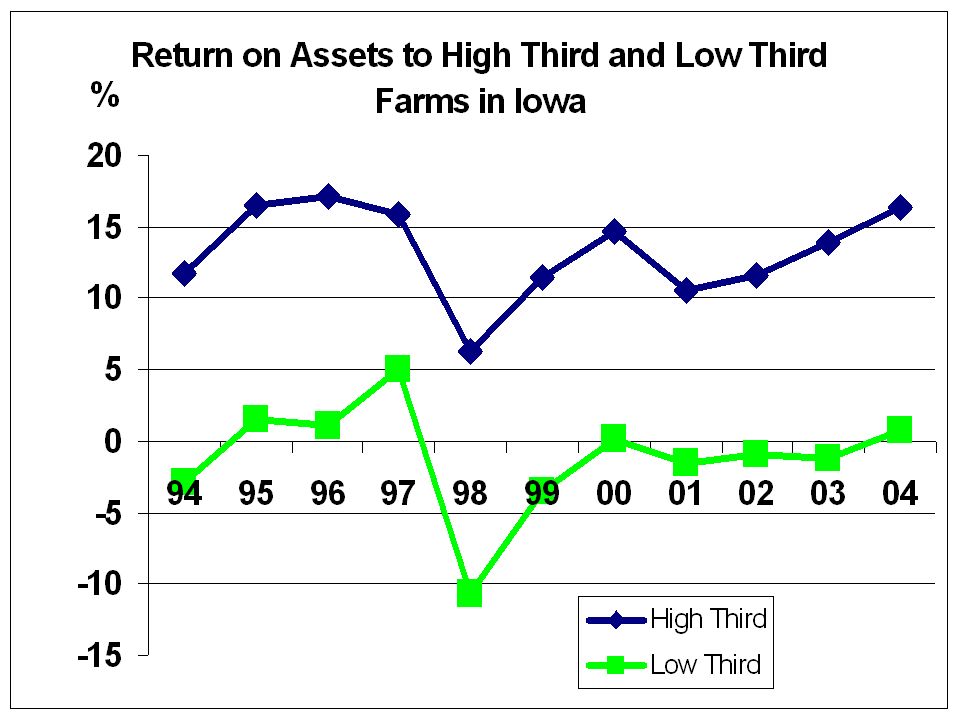

PROFITABILITY Return on assets (ROA) low averagegood

low averagegood")

32

Other ratios Gross revenue can be divided into: operating expense (60 to 70 %) depreciation (5 to 10 %) interest (5 to 10 %) net farm income (15 to 20 %) High profit farms may keep 25 to 30 % of their gross revenue as net income

depreciation (5 to 10 %) interest (5 to 10 %) net farm income (15 to 20 %) High profit farms may keep 25 to 30 % of their gross revenue as net income")

33

FINANCIAL PERFORMANCE MEASURES 1. Compare to similar farms. 2. Look at trends over several years. 3. Supplement ratios with production data and enterprise analysis.

Similar presentations

– Concepts, philosophies and procedures.>")