Download presentation

Presentation is loading. Please wait.

1

課程 14: Mergers and Acquisitions - A Topic in Corporate Finance

3

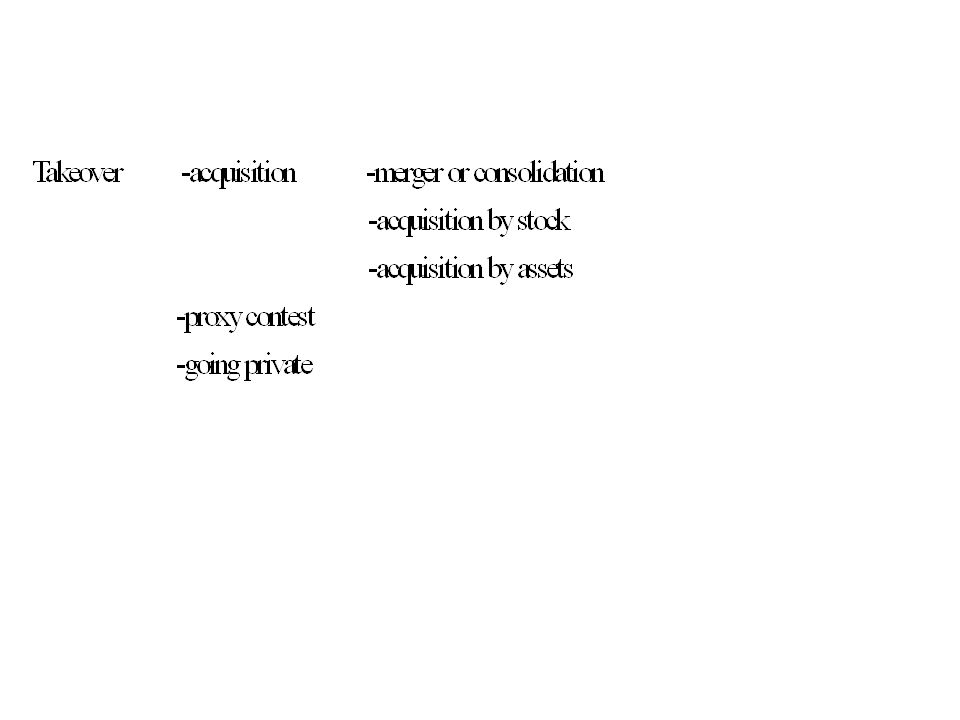

Takeover is a general term referring to the transfer of control of a firm from one group of shareholders to another. Merger: A merger refers to the complete absorption of one firm by another. The acquiring firm retains its identity and the acquired firm ceases to exists as a separate business entity. Bidder: the acquiring firm Target firm: the firm is to be acquired. Consolidation: A consolidation is the same as a merger except that an entirely new firm is created. Old firm cease to exist.

4

Acquisition by stock: To acquire a firm by purchasing the firm’s voting stocks in exchange for cash, shares of stocks, or other securities. Tender offers is a public offer to buy shares by one firm directly from the shareholders of another firm. The tender offer is communicated to the target firm’s shareholders by public announcement.

5

1.In an acquisition by stock, no shareholder meeting have to be held and no vote is required. 2.The target firm’s management and board of directors are bypassed. 3.Acquisition by stock is occasionally friendly. Resistance by the target firm’s management often makes the cost of acquisition by stock higher than that of a merger. 4.Many acquisitions by stock end up with a formal merger later.

6

Acquisition by assets. A firm effectively acquires another firm by buying most or all of its assets. This type of acquisition requires a formal vote of the shareholders of the selling firm.

7

Acquisition classifications Horizontal acquisition: same industry, same business. Vertical acquisition: involves firms at different steps of the production process. Conglomerate acquisition: two firms are not related.

8

Proxy contest An attempt to gain control of a firm by soliciting a sufficient number of stockholders votes to replace existing management. Proxy contest occurs when a group attempts to gain controlling seta on the board of directors by voting in new directors.

9

Going private transaction An publicly owned stocks in a firm are purchased by a small group of investors. Usually the group includes members of incumbent management. A large percentage of money needed to buy up stocks is usually borrowed. So such transactions are known as leveraged buyouts(LBOs). LBOs took place often in the 1980’s in USA.

. LBOs took place often in the 1980’s in USA..")

10

Taxes and acquisition Taxable acquisition: the shareholders of the target firm are considered to have sold their shares, and their capital gains needed to be taxed. The general requirement for tax-free states are that the acquisition be for a business purpose, and that there be a continuity of equity interest. i.e. the shareholders in the target firm must retain an equity interest in the bidder. Like cash→stock: taxable stock→stock: tax-free

11

Accounting for acquisitions Two methods: 1. the purchase method Example:

12

A pays B 18 million in cash. A+B=38. Market value of B’s fixed assets is 14 million. Goodwill must be amortized over a period of time (max. 40 years) The amortization is a deduct from income. The combination of lower reported income and large market value of assets results in lower ROA and ROE.

The amortization is a deduct from income. The combination of lower reported income and large market value of assets results in lower ROA and ROE..")

13

2. Pooling of interests The balance sheets are just added together.

14

Reasons for acquisition Synergy: The acquisition is said to generate synergy. Revenue enhancement *Marketing gains: advertisement, channel, and product mix *Strategic benefits; *market power

15

Cost reduction: more efficiently. *Economy of scale. *Economies of vertical integration *Complementary resources Lower taxes * net operating loses * unused debt capacity: Acquiring some firms that do not use as much debt as they are able. * Surplus funds: free cash flow can be used for investment project Reductions in capital needs: A merger may reduce the combined investment needed by the two firms.

16

Defensive tactics Target firm managers frequently resist takeover attempts * The company charts: The company charts establishes the condition that allows for a takeover. Firms frequently amend corporate charts to make acquiring more difficult. e.q. change voting ration from 2/3 to 90%. This is called supermajority amendment. * Repurchase / standstill agreements: Standstill agreements are contracts where the bidding firms agree to limit its holding in the target firm. A targeted stock repurchase happens that payments are made to potential bidders to eliminate unfriendly takeover attempts. This is greenmail.

17

* Exclusionary self-tender is the opposite of a target repurchase. A firm makes a tender offer for a given amount of its own stock while excluding targeted stockholders. * Poison pills is a financial device designed to make it impossible for a firm to be acquired without managers’ consent. E. q. borrowing money, sell subsidiaries, etc. * Going private and leveraged buyouts

18

* Golden parachutes: Target firms provide compensation to top level managers if a takeover occurs. *Poison put: buy the target firm’s securities at a specified price. *Crown jewel: sell major assets. *white knights

19

Empirical evidence of takeover activities Takeover target bidder tender offer 30% 4% merger 20% 0 proxy contest 8% na 1.tender: unfriendly, cost is high 2.target firm. Gain is high. 3.bidder: To bidding is not for shareholders, but for managers. Gain for bidder firm is low. Another reason for low gain for bidding firm is because the competition is intensive, gain will not by high.

Similar presentations

>")

refers to the aspect of corporate strategy, corporate finance and management dealing.>")