Download presentation

Presentation is loading. Please wait.

1

CORPORATE FINANCIAL THEORY Lecture 9

2

Megers & Acquisitions Three Areas of Study 1. Determining if a Merger creates value (then developing an offer price) 2. Evaluating M&A offers in the market place (your case analysis assignment) 3. M&A Strategies (biggest area of “talk”) Today - Cover both Part 1 & 3 via lecture Part 2 via example

2. Evaluating M&A offers in the market place (your case analysis assignment) 3. M&A Strategies (biggest area of talk ) Today - Cover both Part 1 & 3 via lecture Part 2 via example.")

3

Recent Mergers

4

Bank of America Family Tree Note: Ironically, MBNA was once owned by a previous version of Bank of America, which sold it in an IPO.

5

Mergers (1962-2011)

")

6

Sensible Reasons for Mergers Economies of Scale A larger firm may be able to reduce its per unit cost by using excess capacity or spreading fixed costs across more units. $ $ $ Reduces costs

7

Sensible Reasons for Mergers Economies of Vertical Integration Control over suppliers “may” reduce costs. Over integration can cause the opposite effect. Pre-integration (less efficient) Company S S S S S S S Post-integration (more efficient) Company S

Company S S S S S S S Post-integration (more efficient) Company S.")

8

Sensible Reasons for Mergers Combining Complementary Resources Merging may results in each firm filling in the “missing pieces” of their firm with pieces from the other firm. Firm A Firm B

9

Sensible Reasons for Mergers Mergers as a Use for Surplus Funds If your firm is in a mature industry with few, if any, positive NPV projects available, acquisition may be the best use of your funds.

10

Dubious Reasons for Mergers The Bootstrap Game Acquiring Firm has high P/E ratio Selling firm has low P/E ratio (due to low number of shares) After merger, acquiring firm has short term EPS rise Long term, acquirer will have slower than normal EPS growth due to share dilution.

After merger, acquiring firm has short term EPS rise Long term, acquirer will have slower than normal EPS growth due to share dilution.")

11

Dubious Reasons for Mergers Boot Strap Game Diversification Investors should not pay a premium for diversification since they can do it themselves. Excuse to change capital structure

12

Dubious Reasons for Mergers The Bootstrap Game

13

Dubious Reasons for Mergers Earnings per dollar invested (log scale) Now Time.10.067.05 Muck & Slurry World Enterprises (before merger) World Enterprises (after merger)

Now Time Muck & Slurry World Enterprises (before merger) World Enterprises (after merger)")

14

Additivity Principle Other People’s Money

15

Estimating Merger Gains Q: If M&A creates value, Why? A: Synergies -Admin -Dup services -lower COC

16

Estimating Merger Gains Questions Is there an overall economic gain to the merger? Do the terms of the merger make the company and its shareholders better off? ????

17

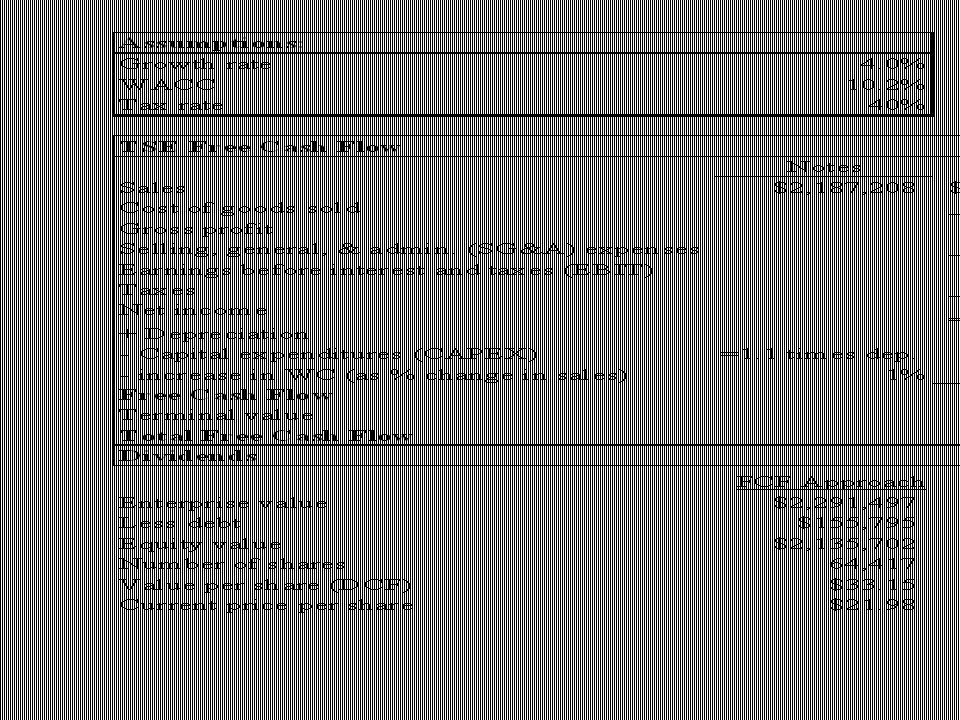

Estimating Merger Gains

18

Example – Two firms merge creating $25 million in synergies. If A buys B for $65 million, the cost is $15 million.

19

Estimating Merger Gains Example – The NPV to A will be the difference between the gain and the cost.

20

Estimating Merger Gains Q: How Much Should A Firm Pay in a M&A? A: Theory Gain = PV AB - (PV A + PV B ) A must pay B part of the gain A: Reality A usually pays B all of the gain, plus more. Why? Premium Paid by A = (Cash - MV B ) + (MV B - PV B )

A must pay B part of the gain A: Reality A usually pays B all of the gain, plus more. Why. Premium Paid by A = (Cash - MV B ) + (MV B - PV B ).")

21

Board Meeting Other People’s Money

22

Takeover Methods Type of Takeovers Hostile Friendly LBO Going Private Greenmail White Knight

23

Takeover Methods Tools Used To Acquire Companies Proxy Contest Acquisition Leveraged Buy-Out Management Buy-Out Merger Tender Offer

24

Takeover Defenses White Knight - Friendly potential acquirer sought by a target company threatened by an unwelcome suitor. Shark Repellent - Amendments to a company charter made to forestall takeover attempts. Poison Pill - Measure taken by a target firm to avoid acquisition; for example, the right for existing shareholders to buy additional shares at an attractive price if a bidder acquires a large holding.

25

Takeover Defenses

26

Board Meeting Wall Street

27

M&A Who Usually Benefits from M&A? Shareholders of B Lawyers & Brokers Execs in A Who Usually Losses in M&A? Shareholders of A Execs in B Employees

28

M&A Analysis Steps for M&A Market Analysis Briefly describe the financial & strategic history of the company Determine pre-announcement value Describe M&A offer Determine merged value (examine synergies) Compare values, offer, & market prices Compare values, offer, & market prices Predict success of M&A Recommend a strategy for investors and shareholders Provide a summary analysis

Compare values, offer, & market prices Compare values, offer, & market prices Predict success of M&A Recommend a strategy for investors and shareholders Provide a summary analysis")

29

M&A Analysis History - News, Annual Report, 10k, etc. (Library & My Web page) (use spreadsheets to present financial facts) (reference your sources) (present both original & summary data) (remember to annualize data) Submit electronically Excel file only Named: Last Name in File Name

(use spreadsheets to present financial facts) (reference your sources) (present both original & summary data) (remember to annualize data) Submit electronically Excel file only Named: Last Name in File Name.")

30

Disney / Cap Cities Deal Announcement of Offer Disney offers to acquire Cap Cities/ABC. Disney will exchange each share of Cap Cities for one share of Disney plus $65 cash. Disney will issue $10bil in new debt to finance the deal.

31

Fact Sheet Forecasted N.E. @ 14% growth rate Forecasted N.E. @ EPSx#New Shares **DisneyMarket Rd7.25%8.0 % EPS$ 2.50$ 2.33

35

Probabilistic Analysis: Monte Carlo Simulation Suppose we allow several assumptions to vary. What is the resulting distribution of the DCF value of equity? Sales growth years 1–3: 14%–17% Sales growth years 4–7: 5%–7% Operating cost/sales: 41%–49% Personnel cost/sales: 13%–17% Receivables/sales: 15%–18% Accounts payable/sales: 15%–18% Other payables/sales: 15/18%

Similar presentations

stations Subcontractors (component.>")

refers to the aspect of corporate strategy, corporate finance and management dealing.>")