Download presentation

Presentation is loading. Please wait.

1

Real Estate Business Ethics

7

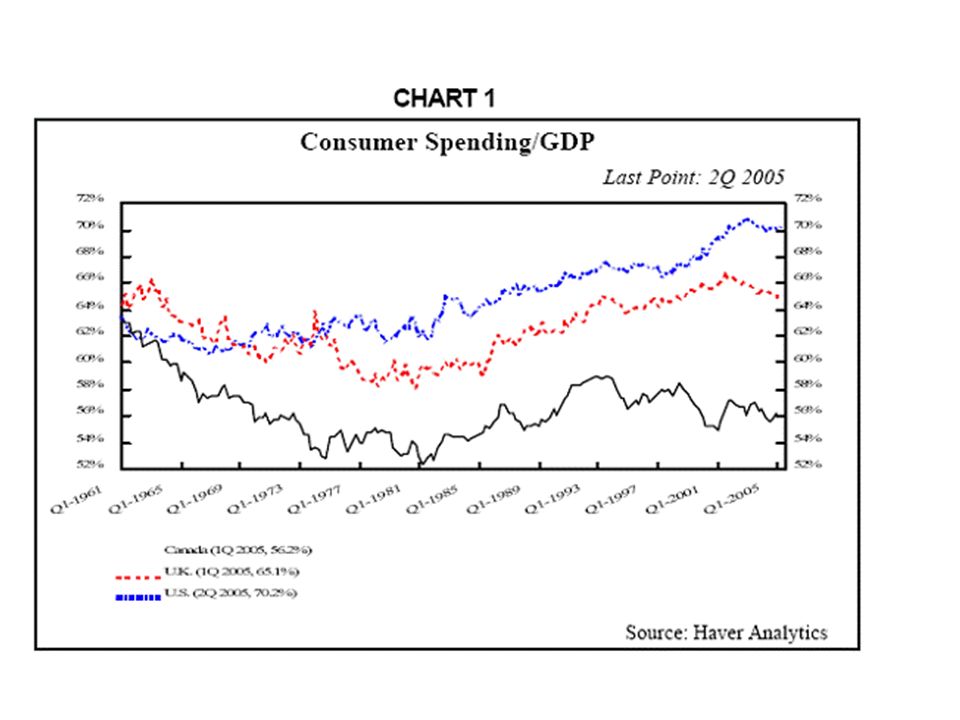

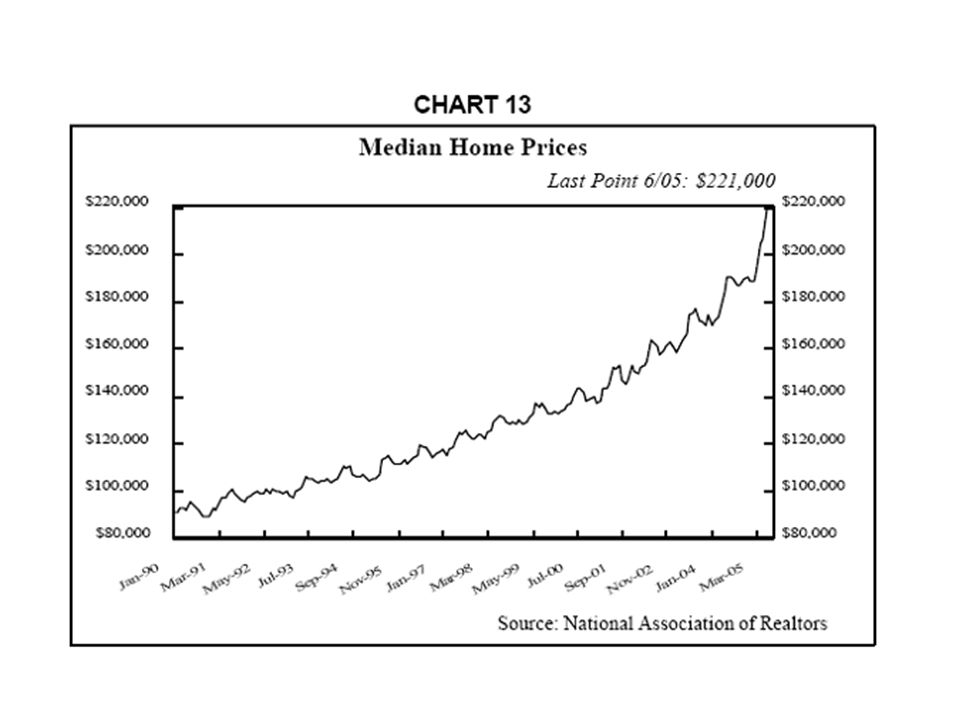

Real Estate and Consumption Increasing real estate prices has made increasing consumption possible

8

Magnitude The Economist, –the total value of residential property in developed economies rose by more than $30 trillion over the past five years, to over $70 trillion –an increase equivalent to 100% of those countries' combined GDPs.

9

Magnitude larger than –the global stock market bubble in the late 1990s (an increase over five years of 80% of GDP) or –America's stock market bubble in the late 1920s (55% of GDP). –In other words, it looks like the biggest bubble in history.

10

Causes historically low interest rates have encouraged home buyers to borrow more money households have lost faith in equities after stock markets plunged

14

Bubble Michael Mandel at Business Week –Residential investment is absorbing a staggering 5.8% of gross domestic product. –That’s the highest level since the late 1940s and early ‘50s, when an entire generation of returning soldiers was setting up families and expanding into newly built suburbs. –This time, Americans are building second homes and enlarging current ones at a record pace.

15

Bubble Measured by the increase in its share of GDP, the housing boom so far is 40% larger than tech

16

Current Situation Housing affordability nationwide has dropped to a 13-year low The household debt-service ratio has soared to a record high. Over one-third of all homeowners devote more than 30% of their incomes to monthly mortgage payments. Twelve percent of homeowners devote over half of their incomes.

17

Current Situation Sub-prime borrowers accounted for 28% of all new mortgage lending in the past six months, vs. 5% five years ago. In the first half of 2005, two-thirds of homebuyers financed more than 80% of their purchase. 17% of homeowners have a loan-to-value ratio (LTV) of 95% or more, versus only 3% one decade ago. (That means that 17% own less than 5% of their home's value free, and clear). About 42% of first-time buyers made NO down- payment on their home purchases in 2004.

of 95% or more, versus only 3% one decade ago. (That means that 17% own less than 5% of their home s value free, and clear). About 42% of first-time buyers made NO down- payment on their home purchases in")

18

Current Situation Nearly 20% of ALL American home-owners would see their home equity wiped out entirely by a mere 5% decline in home prices.

19

ARMs ARMs are typically initially made at a lower rate and then increase after a fixed period of time, usually one, three, five, seven or 10 years. This fall the adjustable-rate mortgages (ARMs) that millions of Americans took out during the recent housing boom will be reset Many homeowners will see their monthly mortgage payments shoot up by as much as 20%.

that millions of Americans took out during the recent housing boom will be reset Many homeowners will see their monthly mortgage payments shoot up by as much as 20%..")

20

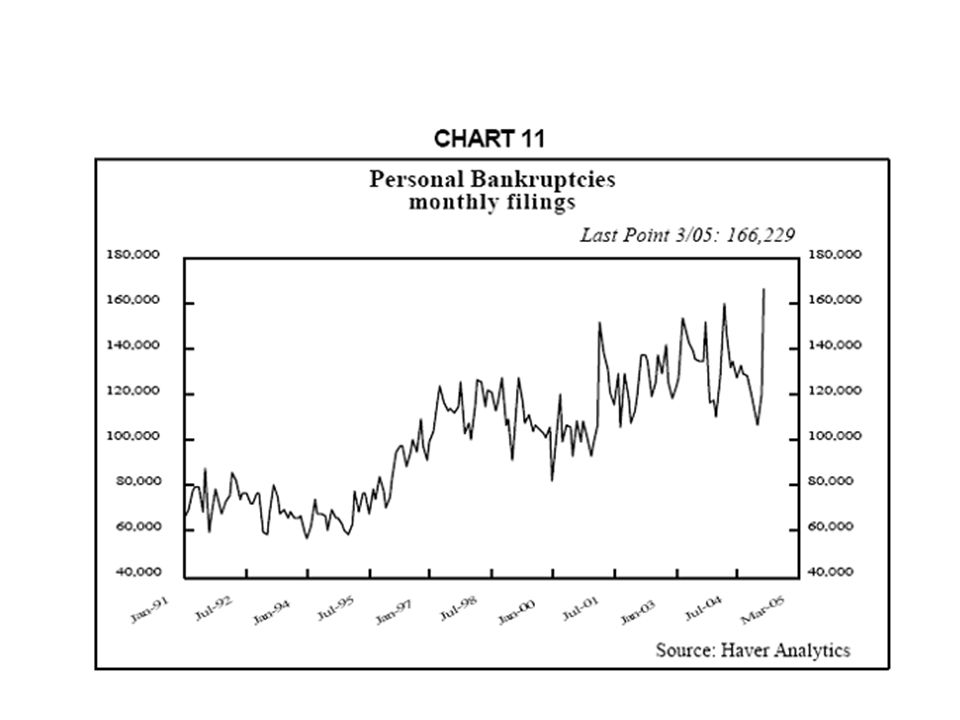

ARMs According to the Mortgage Bankers Association, of all mortgages financed in 2005, 36% were ARMs -- the highest ever. Between $400 billion and $500 billion in ARMs are due to be reset by the end of 2006. Next year more than $1.5 trillion will be reset. Year-to-date, there has been a 39% increase in foreclosures over last year.

22

Current Situation The Enrons of the bust phase will be the firms now pedaling –adjustable-rate, –no-interest/nothing-down –assorted other types of “sub-prime” mortgages.

23

Current Situation At Countrywide Financial, the largest mortgage lender in the U.S., the principal value of negative amortization loans rose almost 100 times, from a value of $33 million at the end of 2004 to $2.9 billion on June 30.

25

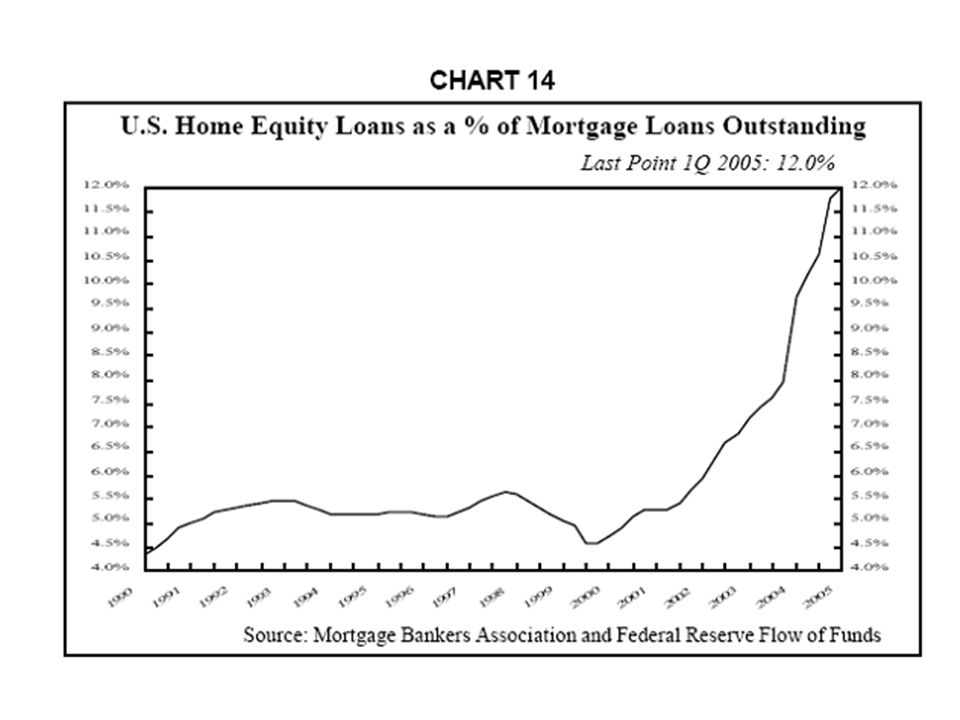

Real Estate Bubbles= More Debt Twofold borrowing by household owners is needed: –FIRST, to boost housing prices –SECOND, to withdraw equity

27

Real Estate Bubbles= More Debt they heavily entangle banks and the whole financial system as lenders –property bubbles have historically been the regular main causes of major financial crises –Japan’s property deflation has continued for 13 years now

28

Consequences Yale economist Robert Shiller predicts a 25% drop in residential property prices. The Economist hints at a worldwide recession when the air goes out of the real estate market.

29

Consequences Yale economist Robert Shiller predicts a 25% drop in residential property prices. The Economist hints at a worldwide recession when the air goes out of the real estate market.

30

Consequences Since the end of 2001, housing-related industries have produced a whopping 43% of the nation's total net private sector employment growth. Any slackening of real estate activity would slow employment growth in the industry.

31

These ferocious excesses of the housing bubble –soaring prices –shriveling home equity –vanishing affordability –idiotic lending practices

32

Policy-Fairness Should the large lenders be bailed out? Will the million of homeowners be bailed out?

Similar presentations

Analyze the various sources of borrowing available to a client and.>")