Download presentation

Presentation is loading. Please wait.

1

Chapter 9 Buying a Home

2

Learning Objectives Decide whether renting or owning is better, both financially and personally. Explain the up-front and monthly costs of buying a home. Describe the steps in the home-buying process. Distinguish among the traditional and alternative ways of financing a home and list the advantages and disadvantages of each. Identify the important aspects of selling a home.

3

Mortgage: a real estate loan

Introduction Mortgage: a real estate loan (the property itself serves as collateral)

")

4

Why the recent explosion in mortgage foreclosures?

Facts & Figures: 90% of young people rent 80% of people own homes Housing values typically increase less than 4% annually Since 2006, home prices have declined 20-50% in most markets Is a home an investment or just a place to live? CONSIDER Why the recent explosion in mortgage foreclosures?

5

Short-term: renters win, based on initial upfront costs

Should you rent or buy? Short-term: renters win, based on initial upfront costs Rent Damage/security deposit Lease contract Periodic tenancy Tenancy for specific time Subleasing Your rights w/o a lease (pg 250)

")

6

Equity and Appreciation Deductibility of items on taxes

Long-term: homeowners win, when income taxes and appreciation are considered Equity and Appreciation Deductibility of items on taxes Real estate taxes Mortgage interest Beware of flipping Being “upside down” (under water) Foreclosure Strategic default (pg 253)

Foreclosure. Strategic default (pg 253)")

7

What does it cost to buy a home?

Most up-front costs are due at the closing (PG 255) ** Closing costs can range 2-10% of loan ** Down payment Attorney fees Title search/insurance Home inspection Appraisal fee Points … and many more!

** Closing costs can range 2-10% of loan ** Down payment. Attorney fees. Title search/insurance. Home inspection. Appraisal fee. Points. … and many more!")

8

When does it make sense for a buyer to do this?

Points Homebuyers can “buy down” the interest rate on their loan 1 point = 1% of loan amount Homebuyer pays for points at closing Lender receives money upfront as compensation for offering a lower rate When does it make sense for a buyer to do this?

9

Important Terms to Understand

Monthly payments include principle & interest Property taxes & homeowners insurance may be ESCROWED: PITI Loan-to-value ratio (LTV) (Lenders expect 80%) Ex: $80,000 mortgage ÷ $100,000 home value = 80% PMI if LTV is too high (pg 257) Protects who? Paid for by who? The New Realities of Home Buying (pg 258) Historically Low Interest Rates Tougher Lending Standards A Buyer’s Market Larger Down Payments

(Lenders expect 80%) Ex: $80,000 mortgage ÷ $100,000 home value = 80% PMI if LTV is too high (pg 257) Protects who Paid for by who The New Realities of Home Buying (pg 258) Historically Low Interest Rates. Tougher Lending Standards. A Buyer’s Market. Larger Down Payments.")

10

How are property taxes determined? (pg 259) ADVICE:

Based on the ASSESSED VALUE of buildings and land Many people appeal their assessed value… and win! How does NY compare? ADVICE: Decide Based on ALL Costs! (Average 30-40% added to loan payment for all other housing costs)

")

11

Steps in Home Buying

12

Get your finances in order Clean up your credit!

Use Internet to Estimate Housing Costs Prequalify for Loan (Determine your own affordability first!) Front-end ratio: PITI compared to gross income PITI should not exceed 25-29% of gross income Back-end ratio: PITI + all other monthly debt (car, student loans, etc) compared to gross income Should not exceed 33-41% of gross income Search for home online and in person

Front-end ratio: PITI compared to gross income. PITI should not exceed 25-29% of gross income. Back-end ratio: PITI + all other monthly debt (car, student loans, etc) compared to gross income. Should not exceed 33-41% of gross income. Search for home online and in person.")

13

Agree to terms with seller (NEGOTIATE!)

Make offer; counteroffer Specify conditions (contingency clauses) Sign purchase contract Formally apply for Mortgage Loan Good faith estimate Mortgage lock-in rate Prepare for closing Hire your own inspector Hire your own attorney Closing Day! Uniform Settlement Statement

Sign purchase contract. Formally apply for Mortgage Loan. Good faith estimate. Mortgage lock-in rate. Prepare for closing. Hire your own inspector. Hire your own attorney. Closing Day! Uniform Settlement Statement.")

14

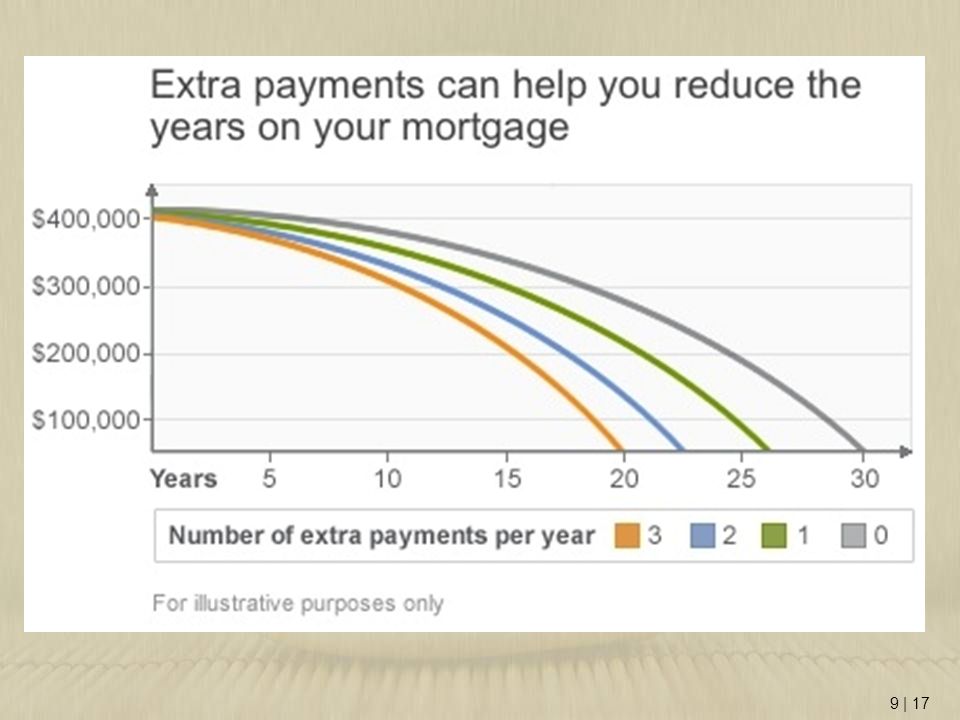

Financing a Home The mathematics of mortgage loans

A mortgage is a collateralized loan Lender has a lien on the real estate A mortgage is an amortized loan (pg 269) How are monthly payments divided between P & I? See chart page 268 Equity = Market Value of Home - Loan Balance Some people made additional payments on loan Affect of this?

How are monthly payments divided between P & I See chart page 268. Equity = Market Value of Home - Loan Balance. Some people made additional payments on loan. Affect of this")

15

Amortization Table for Fixed Rate Loans

18

3 Factors Affect the Mortgage Payment

The Amount Borrowed (see chart pg 270) The Interest Rate SHOP AROUND! Even tiny increments make a HUGE difference The Length of the Loan Conventional Fixed-Rate ARMs (variable-rate loans) Teaser Rate Rate Caps Types of Mortgages <= where is the risk?

The Interest Rate. SHOP AROUND! Even tiny increments make a HUGE difference. The Length of the Loan. Conventional Fixed-Rate. ARMs (variable-rate loans) Teaser Rate. Rate Caps. Types of Mortgages. <= where is the risk")

19

The Main Types of Mortgages What’s the best choice for you?

Fixed-Rate, Fixed-Payment Mortgage Various terms: 10, 15, 20 or 30 years fixed interest rate, fixed monthly payment Each payment consists partly of principle and interest Payments made in early years mainly go toward interest, with very small reductions in loan principal Adjustable-rate mortgages (ARMs) Interest rate varies over life of the loan Why are the initial interest rates typically lower than most fixed-rate mortgages to start? Caps helps to reduce some risk Considerations when evaluating Fixed vs. ARMs What’s the best choice for you? Locale rates

Interest rate varies over life of the loan. Why are the initial interest rates typically lower than most fixed-rate mortgages to start Caps helps to reduce some risk. Considerations when evaluating Fixed vs. ARMs. What’s the best choice for you Locale rates.")

21

Alternative Mortgages

Growing Equity Goal is to reduce interest costs by paying off loan early Bi-weekly mortgage option Reverse Mortgage Second Mortgage Home Equity Loan or Home Equity Line of Credit Rates slightly higher than first mortgages “Eating one’s house” Fin PP pg 276 Mortgage Refinancing Traditional limit for HELs and HELOCs: 80% of MV less loan balance (pg 274).

.")

Similar presentations

Explain the advantages of pre- qualification Describe the different types of mortgages available Ascertain.>")

Analyze the various sources of borrowing available to a client and.>")