Download presentation

Presentation is loading. Please wait.

1

3 Evaluation of Financial Performance ©2006 Thomson/South-Western

2

2 Introduction This chapter introduces financial statement analysis techniques that are used to accurately evaluate a company’s performance.

3

3 Financial Ratios Are Used By Management for planning and evaluating Credit managers to estimate the riskiness of potential borrowers Investors to evaluate corporate securities Managers to identify and assess potential merger candidates

4

4 Ratio Classifications Liquidity Asset management Financial leverage management Profitability Market-based Dividend policy

5

5 Financial Statements Balance sheet Common-sized balance sheet shows assets, liabilities, and equity as a percent of total assets. Income statement Common-sized income statement shows income and expense items as a percent of net sales. Statement of cash flows

6

Common-Size Balance Sheet

7

Common-Size Income Statement

8

8 Statement of Cash Flow Presents the effects of operating, investing, and financing on the cash balance Direct method presents the effects to net cash provided by operating, investing, and financing. Indirect method presents the adjustments to net income showing the effects to net cash. Used for public financial reports The final results for both are identical.

9

9 Liquidity Ratios Current ratio = Quick ratio = Current assets Current liabilities Current assets – Inventories Current liabilities

10

10 Asset Management Ratios Avg. collection period = Inventory turnover = Fixed-asset turnover = Total asset turnover = Cost of sales Average inventory Sales Net fixed assets Sales Total assets Accounts receivable Annual credit sales/365

11

11 Financial Leverage Management Debt ratio = Debt-to-equity ratio = Times interest earned = Fixed charge coverage = Total debt Total assets Total debt Total equity EBIT Interest charges EBIT + Lease pmts (Interest + Lease pmt + P/S div before tax + pre-tax sinking fund)

")

12

12 Profitability Ratios Gross profit margin = Net profit margin = ROI = ROE = Sales – Cost of sales Sales EAT Sales EAT Total assets EAT Stockholders’ equity

13

13 Market-based Ratios P/E ratio = Market to book ratio = Marketing price per share Current earnings per share Market price per share Book value per share

14

14 Dividend Policy Ratios Payout ratio = Dividend yield = Dividends per share EPS Expected dividends per share Stock price

15

15 Financial Ratio Analysis Trend analysis20X0X1X2 XYZ current ratio 1.92.22.3 Cross-sectional analysis20X2 XYZ current ratio 2.3 Industry norms 2.5 Both simultaneously20X0X1X2 XYZ current ratio1.92.22.3 Industry norms2.52.42.5

16

16 Relationships Among Ratios ROI = ROE = EAT Sales Total assets EAT Total assets = EAT Sales Total assets Equity Net profit margin Total assets turnover Equity multiplier

17

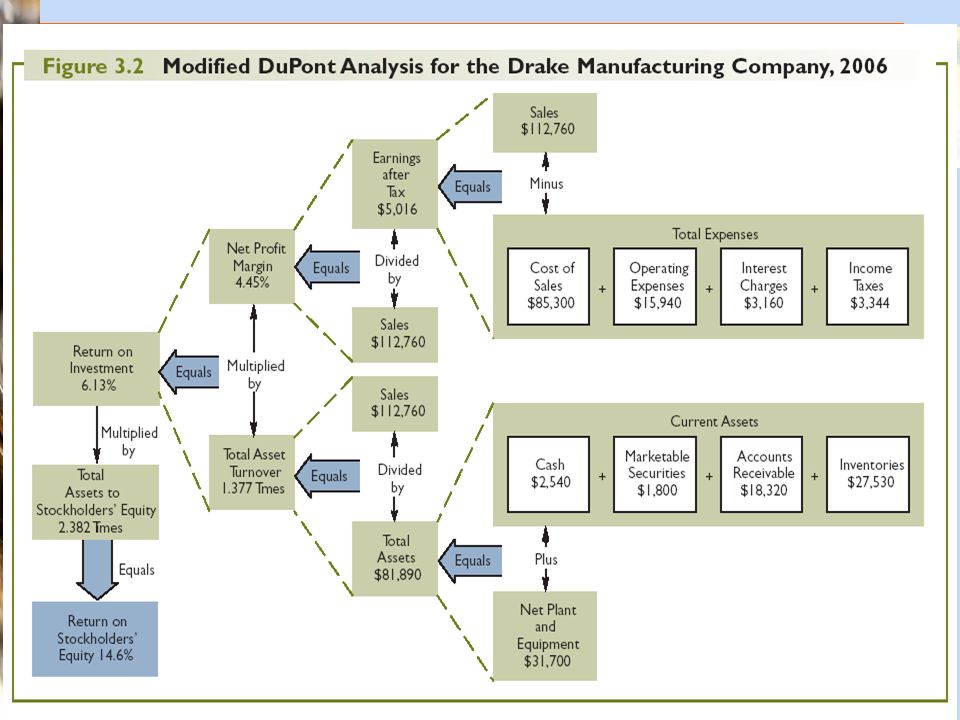

17 Dupont Analysis An excellent way to present ratio analysis for an assignment or for an on- the-job presentation

19

19 Sources of Information Dun and Bradstreet Robert Morris Associates Prentice-Hall’s Almanac of Business and Industrial Ratios Moody’s Standard and Poor’s Annual reports 10Ks Trade associations Trade journals Commercial banks Financial Research Associates Computerized databases

20

Sources of Information on the Web http://finance.yahoo.com/ http://www.dnbcorp.com/ http://www.rmahq.org/ http://www.sec.gov/ http://www.moodys.com/ http://www.hoovers.com/ http://www.bloomberg.com/

21

A Word of Caution Ratios are only as reliable as the accounting data on which they are based Firms that compile industry norms often do not report information about the dispersion of the individual values around the mean ratio Comparative analysis depends on availability of data Financial ratios provide historic record

22

22 Quality and Financial Analysis The quality of a firm’s earnings is positively related to the proportion of cash earnings to total earnings and to the proportion of recurring income to total income. The quality of a firm’s balance sheet is positively related to the ratio of the market value of the firm’s assets to book value of the assets and inversely related to the amount of its hidden liabilities.

23

Problems in Reporting Time of revenue recognition Establishment of reserves Amortization of intangible assets Including all losses and debt “Pro forma” profitability measures

24

Sarbanes-Oxley Transparency of information Accountability in the reporting process Integrity in financial reporting

25

Balance Sheet Quality Issues Charging off assets Hidden liabilities Hidden assets Off balance sheet financing

26

26 Analysis Based on the Market Value of the Firm Market value added (MVA) = Market value – Capital The capital market’s assessment of the accumulated NPV of all of the firm’s past and present projected investment projects Economic value added (EVA) = (r – k) Capital The yearly contribution of a firm’s operations to the creation of MVA

= Market value – Capital The capital market’s assessment of the accumulated NPV of all of the firm’s past and present projected investment projects Economic value added (EVA) = (r – k) Capital The yearly contribution of a firm’s operations to the creation of MVA")

27

27 Problems Caused by Inflation Inventory profit as a result of timing of price increases Inventory valuation methods (LIFO) (FIFO) Rising interest rates causing a decline in the value of long-term debt Differences in the reporting of earnings Recognition of sales

(FIFO) Rising interest rates causing a decline in the value of long-term debt Differences in the reporting of earnings Recognition of sales")

28

28 The Cash Flow Concept Accounting income vs. Cash flow Cash flow is the relevant source of value for the firm. ATCF = EAT + Noncash charges Noncash charges = Depreciation + Deferred taxes

29

29 Complex international aspects of financial statement analysis Influenced by fluctuating exchange rates Statement of Accounting Standards No. 52 deals with foreign currency translation.

30

30 Accuracy of Financial Statements External auditor Generally accepted accounting principles Corporations pose for a financial statement like people pose for a picture.

Similar presentations

>")

: Valuation techniques Dividend discount model, P/E ratio Need.>")