Download presentation

1

Public Television Strategic Investment Scenarios Digital Distribution Implementation Initiative NETA 2003 Conference San Antonio, January 9, 2003

2

Participants Work scope involved both radio and television scenarios. The latter covered in this report.

3

Core Working Group & CPB Ed Caleca, PBS Jeff Clarke, KQED Dennis Haarsager, KWSU, NW Public Radio (DDII consultant) Byron Knight, Wisconsin David Liroff, WGBH Pete Loewenstein, NPR André Mendes, PBS Jim Paluzzi, Boise State Radio Ted Coltman, CPB Andy Russell, CPB Doug Weiss, CPB Alison White, CPB R/TVRadio TelevisionCivilian

Byron Knight, Wisconsin David Liroff, WGBH Pete Loewenstein, NPR André Mendes, PBS Jim Paluzzi, Boise State Radio Ted Coltman, CPB Andy Russell, CPB Doug Weiss, CPB Alison White, CPB R/TVRadio TelevisionCivilian")

4

Multidiscipline Experts Group Jon Abbott, WGBH Brenda Barnes, KUSC Rod Bates, Nebraska Joe Campbell, KAET Scott Chaffin, KUED Beth Courtney, Louisiana Vinnie Curren, WXPN Tom DuVal, WMRA Tim Emmons, Northern Public Radio Fred Esplin, U. of Utah Glenn Fisher, KTCA Jack Galmiche, Oregon John King, Vermont Ted Krichels, WPSX Jon McTaggart, Minnesota Public Radio Paige Meriwether, KUED Steve Meuche, WKAR Peter Morrill, Idaho Meg OHara, WNET

5

Multidiscipline Experts Group Maynard Orme, Oregon Allan Pizzato, Alabama Lou Pugliese, onCourse Don Rinker, Alaska Meg Sakellarides, Connecticut Bert Schmidt, WVPT Jonathan Taplin, Intertainer Kate Tempelmeyer, Nebraska Tom Thomas, SRG Mike Tondreau, Oregon David Wolff, Fathom Art Zygielbaum, Nebraska

6

Current Environmental Scan

7

Public Broadcasting Today Everyone is baking their own cookies Hail Mary method of funding depreciation Usage strong compared to other public service providers, not so (TV) compared to other broadcasters Policy support of pubcasting less assured Our esteem is an asset that can be leveraged or squandered Other public service entrants entering electronic media

compared to other broadcasters Policy support of pubcasting less assured Our esteem is an asset that can be leveraged or squandered Other public service entrants entering electronic media")

8

The Electronic Media Today Conglomerates dominate ownership and control diverse distribution outlets, with both horizontal and vertical operations and pricing advantages Users are beginning to take control of when they access programming Subscriber-based economic models (e.g., HBO) are competing with ad-supported ones

are competing with ad-supported ones")

9

Television Today Cable/DBS are gatekeepers for the main receiver in 85% of homes Cable/DBS increasingly deliver original progr. Cable/DBS focus is on quantity vs. quality Non-broadcast channels are on threshold of overtaking broadcast channels in viewing Television advertising may erode as cable & DBS develop greater advertising options No federal support for multicast; no active support for non-HD models

10

Diverging Fortunes of Public R/TV Terrestrial digital transition is mandatory for TV, voluntary for radio Content production entities are generally licensee based (with major exception of NPR) Public TV viewing and number of members is steadily declining, while public radio listening and memberships have increased Public radio players have explored alternative distribution platforms to a greater degree than have PTVs

Public TV viewing and number of members is steadily declining, while public radio listening and memberships have increased Public radio players have explored alternative distribution platforms to a greater degree than have PTVs")

11

Five-Year Horizon Most Probable Outcomes

12

Television In Five Years Terrestrial will be of minor consequence as last-mile distribution to mass audiences Viewers will choose from incr. customized, personalized programming options Revenues from other than spot advertising will become significant and competitive Must convince replaces must carry; some stations will be shut out of cable/DBS

13

Television In Five Years Erosion of audience and revenue threaten existence of many licensees; may be fewer licensees A variety of technologies, wired and wireless, to compete for delivery of services Audiences will still value storytelling, but truly compelling content will continue to be scarce First stations in the new mobile video/multimedia service will begin operation

14

Five-Year Horizon Plausible But Less Probable Outcomes – Wins and Losses

15

Unexpected Wins DTV killer application – content or service – that accelerates adoption DTV universal set-top box works with a wide variety of digital services, including DTT New broadcast models (rich media, mobile) prove economically viable

prove economically viable")

16

Closet of Our Anxieties DTV DOA with stranded $1B+ investment; diminished credibility with funders No federal funding for public TV NGIS – capabilities drastically reduced Early surrender of analog spectrum Continued reduction of funding for public broadcasting

17

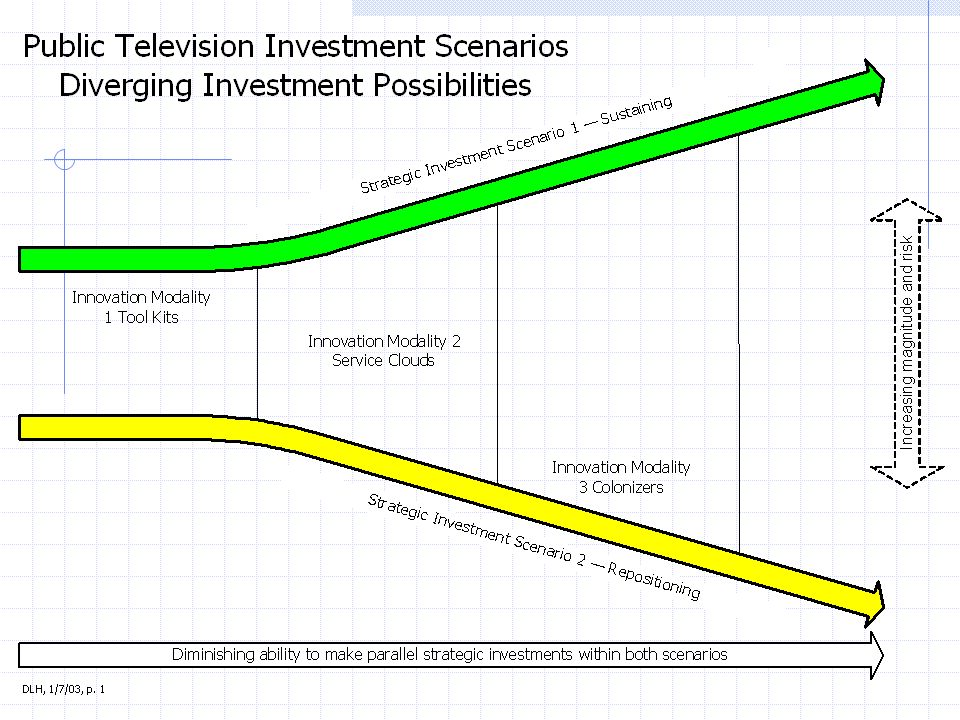

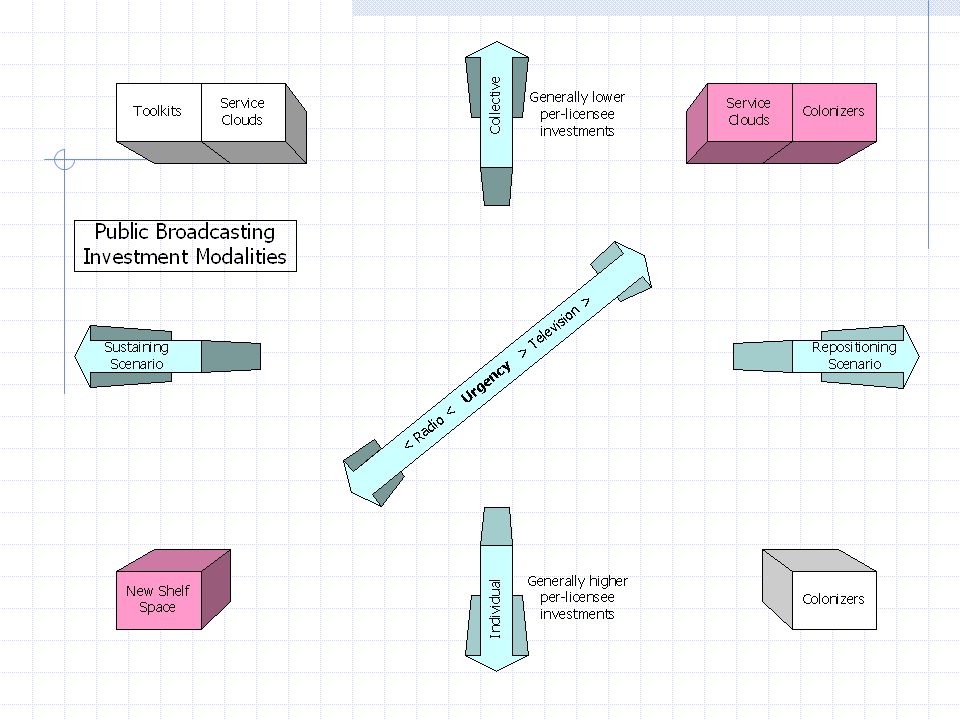

Strategic Investment Scenarios Investments may be individual or collective

18

Collective Investment Modalities Toolkits – activities or tools licensees can use to achieve best practices without need for collaboration Service Clouds – stations outsource significant activities created for specialized purposes Colonizers – efforts to operate public broadcasting mission elements independently with or without station involvement

19

Scenario 1 – Sustaining Make strategic investments in initiatives that sustain the legacy (broadcasting) business Tends to maintain operational independence Preserves as much gross tonnage of public service as possible, at least in near term; lengthening the glide path High investments in toolkits, somewhat lower investments in service clouds, little in colonizers

business Tends to maintain operational independence Preserves as much gross tonnage of public service as possible, at least in near term; lengthening the glide path High investments in toolkits, somewhat lower investments in service clouds, little in colonizers")

20

Scenario 2 – Repositioning Make strategic investments in initiatives that reposition public television in new directions consistent with historic mission Capacity and scale created at collective level Emphasis on editorial (programming) rather than operational independence Accepts the current glide path but creates new climb paths Increased investments in service clouds and colonizers

rather than operational independence Accepts the current glide path but creates new climb paths Increased investments in service clouds and colonizers")

24

Provocations From the consultant…

25

Television Provocations Form virtual broadcast groups, digital distribution companies that operate key functions of current stations across markets Provide elective, centralized station operations services through PBS Create public service digital condominium association with other state, national and international advanced networks Task system economics panel with devising strategies to redeploy [insert ambitious amount here] to priorities

![Television Provocations Form virtual broadcast groups, digital distribution companies that operate key functions of current stations across markets Provide elective, centralized station operations services through PBS Create public service digital condominium association with other state, national and international advanced networks Task system economics panel with devising strategies to redeploy [insert ambitious amount here] to priorities](http://images.slideplayer.com/1/678233/slides/slide_25.jpg "Television Provocations Form virtual broadcast groups, digital distribution companies that operate key functions of current stations across markets Provide elective, centralized station operations services through PBS Create public service digital condominium association with other state, national and international advanced networks Task system economics panel with devising strategies to redeploy [insert ambitious amount here] to priorities")

26

Virtual Broadcast Groups Repositioning service clouds Provides competitive (to commercial group stations) scale and cost savings Create common technical standards and best practices Licensees freed to concentrate on things not transparent to viewers, on building new constituency relationships, and fundraising Groups could aggregate for multiple reasons

scale and cost savings Create common technical standards and best practices Licensees freed to concentrate on things not transparent to viewers, on building new constituency relationships, and fundraising Groups could aggregate for multiple reasons")

27

PBS Station Operations Services Repositioning Service Cloud Provides similar functions to VBGs, though perhaps more oriented toward technical ops Natural extension of NGIS role and mission Services could also be provided with VBG affiliates

28

Digital Condominium Association Builds on blossoming relationships with Internet2 and affiliated state networks (e.g., IA, MI, TX, WA) Scale saves substantial dollars on capacity Enables public television to serve emerging communications needs of education, libraries, museums, et al. Multiplies political capital for interconnection Peering provides collaborative environment for all condo residents – the pool

29

Redeploy $ To Key Priorities Wide agreement on unnecessary expenditures at your station (not mine) Unnecessary = expenditures transparent to our viewers Perhaps we really can afford our service priorities Set an ambitious goal and task a panel with the task of identifying where and how – with proceeds redeployed to programming, capital needs and repositioning colonizer investments

Unnecessary = expenditures transparent to our viewers Perhaps we really can afford our service priorities Set an ambitious goal and task a panel with the task of identifying where and how – with proceeds redeployed to programming, capital needs and repositioning colonizer investments")

30

DDII Scenarios Documents www.technology360.com Scroll to Documents

31

Contact Information Dennis L. Haarsager, DDII Consultant 1019 Border Ln., Moscow, ID 83843-8737 208.892.9445 | e-fax 206.770.6100 haarsager@moscow.com Associate Vice President, Educational Telecommunications & Technology, Washington State University Box 642530, Pullman WA, 99164-2530 509.335.6530 | e-fax 888.455.1070 | haarsager@wsu.edu

>")