Download presentation

1

Slide Show #14 AGEC 430 Macroeconomics of Agriculture Spring 2010

2

Handout #23 Supplemental Slides enhancing this slide show. I will point to specific text from Handout #23 at the end of this show

3

Measures of Liquidity Current ratio 1. Current ratio: Current assets divided by current liabilities. Demonstrates ability to cover scheduled current liabilities for the coming year out current assets and still have “cash” left over. exceed 1.0 Should exceed 1.0 to be technically liquid. Some firms fail despite exceeding this hurdle.

4

Measures of Liquidity Current ratio 1. Current ratio: Current assets divided by current liabilities. Demonstrates ability to cover scheduled current liabilities for the coming year out current assets and still have “cash” left over. exceed 1.0 Should exceed 1.0 to be technically liquid. Some firms fail despite exceeding this hurdle. Working capital 2. Working capital: Current assets minus current liabilities. Expresses liquidity in dollars rather than ratio. Should be positive. Cash is King!

5

Liquidity Trends Survived Failed Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

6

Liquidity Trends Survived Failed Minimum Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

7

Survived Failed Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research Liquidity Trends

8

Measures of Solvency Debt ratio 1. Debt ratio: Total debt divided by total assets. Demonstrates ability to liquidate the firm, cover all liabilities out of all assets, and still have “cash” left over. not exceed 0.50 Should not exceed 0.50 to minimize financial risk exposure. Some firms fail however at lower levels.

9

Measures of Solvency Debt ratio 1. Debt ratio: Total debt divided by total assets. Demonstrates ability to liquidate the firm, cover all liabilities out of all assets, and still have “cash” left over. not exceed 0.50 Should not exceed 0.50 to minimize financial risk exposure. Some firms fail however at lower levels. Leverage ratio 2. Leverage ratio: Total debt divided by equity or net worth. Often a credit standard in loan approval decisions. not exceed 1.0 Should not exceed 1.0 to minimize financial risk exposure. Effects of rising interest rates.

10

Solvency Trends Survived Failed Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

11

Solvency Trends Survived Failed Maximum Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

12

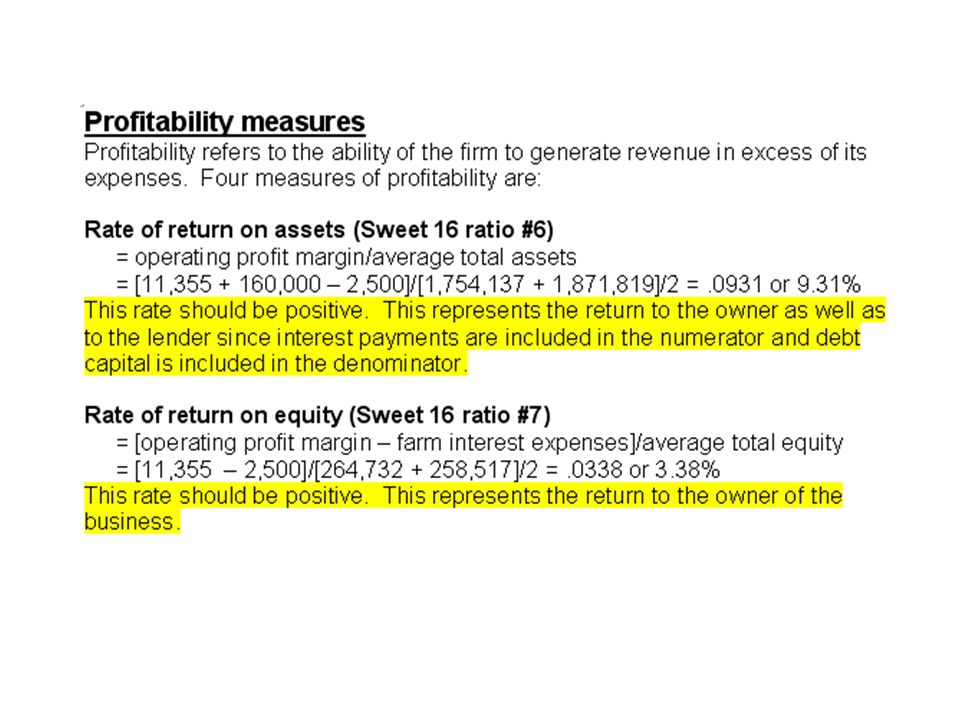

Measures of Profitability Rate of return on assets 1. Rate of return on assets: Net income plus interest divided by total assets. Demonstrates the after-tax return to the total capital invested in the firm. positive Should be positive; the higher the better.

13

Measures of Profitability Rate of return on assets 1. Rate of return on assets: Net income plus interest divided by total assets. Demonstrates the after-tax return to the total capital invested in the firm. positive Should be positive; the higher the better. Rate of return on equity 2. Rate of return on equity: Net income divided equity. Demonstrates the after-tax return on owner equity invested in the firm. positive Should be positive; the higher the better.

14

Profitability Trends Survived Failed Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

15

Profitability Trends Survived Failed Minimum Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

16

Measure of Debt Coverage Term Debt and Capital Lease Coverage Ratio 1. Term Debt and Capital Lease Coverage Ratio: Cash available from operations to cover scheduled payments (net income plus depreciation and interest payments less withdrawals) divided by scheduled principal and interest payments on term loans and capital leases. After provision for taxes and withdrawals. greater than 1.0 Should be greater than 1.0. Non-farm income often factored in by lenders.

divided by scheduled principal and interest payments on term loans and capital leases. After provision for taxes and withdrawals. greater than 1.0 Should be greater than 1.0. Non-farm income often factored in by lenders..")

17

Measure of Debt Coverage Term Debt and Capital Lease Coverage Ratio 1. Term Debt and Capital Lease Coverage Ratio: Cash available from operations to cover scheduled payments (net income plus depreciation and interest payments less withdrawals) divided by scheduled principal and interest payments on term loans and capital leases. After provision for taxes and withdrawals. greater than 1.0 Should be greater than 1.0. Non-farm income often factored in by lenders. Debt Burden Ratio 2. Debt Burden Ratio: Total debt outstanding divided by net income. Number of years required to retire total debt if net income remains constant and used entirely for this purpose low Should be low; the lower the better.

divided by scheduled principal and interest payments on term loans and capital leases. After provision for taxes and withdrawals. greater than 1.0 Should be greater than 1.0. Non-farm income often factored in by lenders. Debt Burden Ratio 2. Debt Burden Ratio: Total debt outstanding divided by net income. Number of years required to retire total debt if net income remains constant and used entirely for this purpose low Should be low; the lower the better..")

18

Debt Repayment Capacity Survived Failed Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research Inverse of debt burden ratio assuming use of depreciation allowances to retire debt.

19

Some Conclusions…. Indicators of growth/survival:Indicators of growth/survival: –Increasing liquidity –Increasing solvency –Increasing debt repayment capacity –Increasing profitability

20

Some Conclusions…. Indicators of potential failure:Indicators of potential failure: –Declining liquidity –Declining solvency –Decreasing debt repayment capacity –Decreasing profitability

21

Some Conclusions…. Indicators of growth/survival:Indicators of growth/survival: –Increasing liquidity –Increasing solvency –Increasing debt repayment capacity –Increasing profitability Indicators of potential failure:Indicators of potential failure: –Declining liquidity –Declining solvency –Decreasing debt repayment capacity –Decreasing profitability

22

Liquidity Trends Survived Failed Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

23

Liquidity Trends Survived Failed Minimum Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

24

Survived Failed Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research Liquidity Trends

25

Solvency Trends Survived Failed Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

26

Solvency Trends Survived Failed Maximum Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

27

Profitability Trends Survived Failed Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

28

Profitability Trends Survived Failed Minimum Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research

29

Debt Repayment Capacity Survived Failed Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research Inverse of debt burden ratio

30

Some Conclusions…. Indicators of growth/survival:Indicators of growth/survival: –Increasing liquidity –Increasing solvency –Increasing debt repayment capacity –Increasing profitability Indicators of potential failure:Indicators of potential failure: –Declining liquidity –Declining solvency –Decreasing debt repayment capacity –Decreasing profitability

31

Failed Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research Summary of Trends…

32

Failed Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research Summary of Trends…

33

Failed Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research Summary of Trends…

34

Failed Source: W. H. Beaver, “Financial Ratios and Predictors of Failure”, Journal of Accounting Research Summary of Trends…

35

#1:Historical Analysis A look backwards like the Beaver study. Comparison of current performance with past performance. Recommend doing this at the enterprise level as well as for the farm as a whole.

36

#1:Historical Analysis A look backwards like the Beaver study. Comparison of current performance with past performance. Recommend doing this at the enterprise level as well as for the farm as a whole. Why is ROA falling? Why is ROA falling?

37

#2:Comparative Analysis Comparing current performance with similar operations like the Beaver study. Your firm Benchmark

38

#2:Comparative Analysis Comparing current performance with similar operations like the Beaver study. Benchmark analysis at enterprise level when possible. Your firm Benchmark

39

#2:Comparative Analysis Comparing current performance with similar operations like the Beaver study. Benchmark analysis at enterprise level when possible. before it is too late Address reasons why your firm is performing more poorly than other comparable operations before it is too late. Your firm Benchmark

40

#2:Comparative Analysis Comparing current performance with similar operations like the Beaver study. Benchmark analysis at enterprise level when possible. before it is too late Address reasons why your firm is performing more poorly than other comparable operations before it is too late. Your firm Benchmark

41

#2:Comparative Analysis Comparing current performance with similar operations like the Beaver study. Benchmark analysis at enterprise level when possible. before it is too late Address reasons why your firm is performing more poorly than other comparable operations before it is too late. Your firm Benchmark

42

#2:Comparative Analysis Comparing current performance with similar operations like the Beaver study. Benchmark analysis at enterprise level when possible. before it is too late Address reasons why your firm is performing more poorly than other comparable operations before it is too late. Your firm Benchmark

43

#2:Comparative Analysis Comparing current performance with similar operations like the Beaver study. Benchmark analysis at enterprise level when possible. before it is too late Address reasons why your firm is performing more poorly than other comparable operations before it is too late. Your firm Benchmark

44

Presentation Model The model given to each presentation team will calculate these financial ratios for you. Your task will be to interpret these ratios for your business as conditions change in the Lower Slobovian economy.

45

Table appearing on one of the worksheets in the class model.

46

Four of the five graphs generated by the class model.

47

Impact of a tighter monetary policy…what do you see?

48

Weaker liquidity Weaker profitability Weaker debt coverage Weaker solvency Impact of a combination of tighter monetary and fiscal policy

49

Handout #23 Here is the text in this handout

50

Handout #23 contains an example income statement, balance sheet and cash flow information used to calculate these and other ratios.

54

Another measure is the debt burden ratio, or the ratio of debt outstanding to net cash income. The higher the ratio, the greater the stress on net cash income to retire debt outstanding.

2004 Prentice Hall, Inc. The Analysis of Financial Statements This chapter will develop tools and.>")