Download presentation

Presentation is loading. Please wait.

1

Secular trends in Gulf geo- economics Steffen Hertog Kuwait Professor, Sciences Po Second Franco-Singaporean conference on the impact of the Middle East on Southeast Asia and Europe

2

The next 40 minutes Setting the stage: Gulf and MENA growth trends MENA’s role in the global distribution of resources Trends in trade Trends in FDI Intra-regional power shifts in MENA –Comparing MENA oil state foreign policies Where are Sovereign Wealth Funds headed? Gulf public enterprises as international strategic actors

3

No other high-income region has grown as fast as the GCC (source: IIF)

")

4

The rest of MENA has also been growing faster than the rest of the world, but it does not matter much:

5

Intra-regional power shifts Intra-regional trade stagnates at around 10% of the total, but intra-regional investment has been booming –An estimated 60 billion $ of Gulf money was allocated in the wider MENA region 2002-2006 –Increasing role of FDI, including in new sectors like: Finance Manufacturing Telecoms and ICT –Increasingly proactive policy to solicit Gulf capital –Gulf capital as political capital in a region in which military assets have lost much of their value?

6

Still, the GCC remains a SMALL players on the global scene in terms of GDP (source: Deutsche Bank)

")

7

The Gulf matters for a different reason: Feedstock –Oil, but also –Gas –Petrochemicals –Other basic inputs for heavy industry Capital surpluses –SWFs, but also private overseas capital

10

Source: Gulf Investment House

11

Why the Gulf and Asia are emerging as tomorrow’s geo-economic axis: factor complementarity

12

Long-term trends in GCC exports (IMF DOTS)

")

13

Long-term trends in GCC imports (IMF DOTS)

")

14

Trade follows factors, but does investment? Despite much talk, only to some extent: Source: IIF Western markets remain deeper and more liquid Asia has its own capital resources

15

Will a large-scale shift of Gulf capital towards Asia happen? Not in the wake of the current credit crisis In the long run? Depends on –a) whether there are actually surpluses to allocate, which is determined by Scale of losses in the current crisis Domestic spending policies in the Gulf Long-term oil prices –b) Gulf investors’ appetite for risk –c) Asian opportunities, specifically China’s willingness to engage in quid-pro-quos of FDI vs. feedstock

whether there are actually surpluses to allocate, which is determined by Scale of losses in the current crisis Domestic spending policies in the Gulf Long-term oil prices –b) Gulf investors’ appetite for risk –c) Asian opportunities, specifically China’s willingness to engage in quid-pro-quos of FDI vs. feedstock.")

16

The geo-economics of Gulf oveseas capital: basic figures Gross official reserves of MENA have increased at a 5-year CAGR of 43.3% from $180 billion in 2003 to $1.087 trillion in 2008. Aggregate current account surpluses of the MENA economies: –estimated to reach $495 billion by end of 2008 –estimated to decline to $406 billion in 2009. 2009 might look at lot worse Sources: IIF, Deutsche

17

Is the GCC’s window of surpluses closing? (Source: Citi)

")

19

Gulf governments could run fiscal deficits next year already (Source: Citi)

")

20

(Source: Citi)

")

21

Relative importance of oil exporter SWFs likely to decline

22

Recent overseas capital trends: Further shift away from US$ assets after 2006 (50% of >900 billion $ allocated 2003 to 2008 went into non-US markets) But: flight to quality with the credit crisis –US-denominated assets have made a comeback, for the time being SWFs have burned their fingers with more speculative assets: losses of about 15% Low appetite for risk Together with lower surpluses, large-scale inflows into Asia unlikely

But: flight to quality with the credit crisis –US-denominated assets have made a comeback, for the time being SWFs have burned their fingers with more speculative assets: losses of about 15% Low appetite for risk Together with lower surpluses, large-scale inflows into Asia unlikely")

23

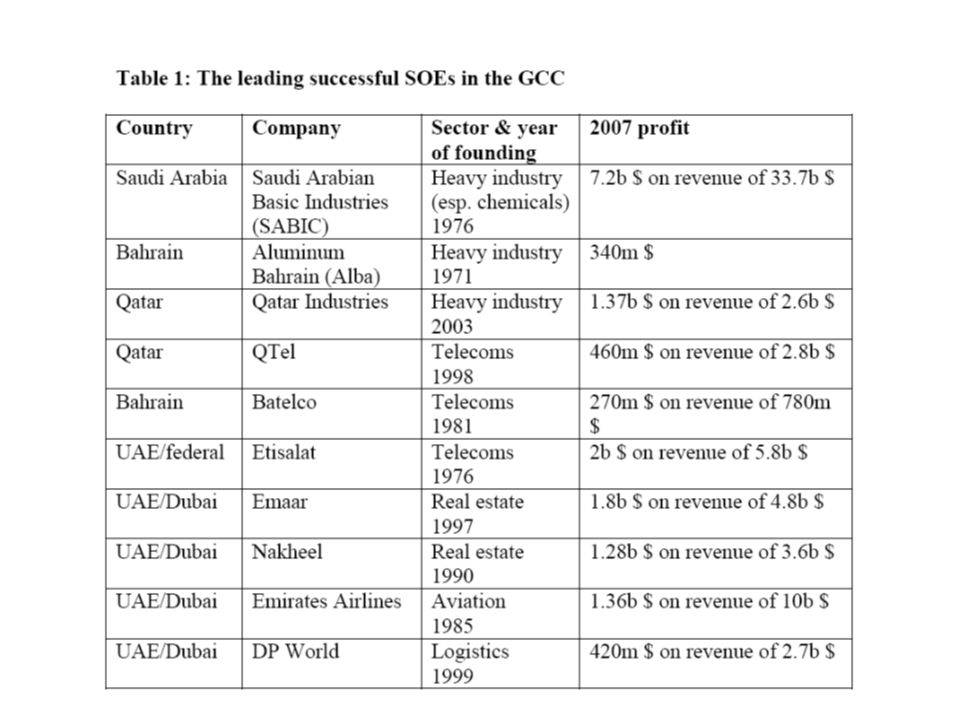

The new Gulf SOEs A new generation of large, multinational enterprises has emerged in the Gulf, most of which are state-owned Much more than SWFs, they have been aiming specifically at Asian markets –Tourism and real estate –Logistics –Heavy industry –Telecoms Large enough to make a substantial impact, small enough to thrive in niches Apart from trade, the burgeoning Gulf SOEs could emerge as the main economic link between the two regions

25

Gulf service exports: telecoms as new FDI niche

26

What about other oil states in the region? Iran, Libya, Algeria – (post-)populist, republican regimes – are likely to suffer more from the crisis than the Gulf states Smaller surpluses Worse fiscal management: –higher breakeven oil prices –higher inflation Less successful diversification policies (no successful SOEs e.g.) Worse public sector legacies Gulf crisis resilience is higher

populist, republican regimes – are likely to suffer more from the crisis than the Gulf states Smaller surpluses Worse fiscal management: –higher breakeven oil prices –higher inflation Less successful diversification policies (no successful SOEs e.g.) Worse public sector legacies Gulf crisis resilience is higher.")

27

Populist oil states have much smaller resources:

28

Linkages of economics and politics – are there security dimensions to the Gulf’s geo- economic repositioning? Not many! Gulf states want: –A calm environment and to depoliticize their economic relations as far as possible The calmer the Middle East is, the more powerful they are relative to other MENA states –Different from China (but similar to Singapore), their economic rise is not tied to any geo-political ambitions –They want multiple partners to increase interdependence But they have no alternative to the US security umbrella –Will China develop geo-strategic ambitions in the Gulf? Not any time soon…

, their economic rise is not tied to any geo-political ambitions –They want multiple partners to increase interdependence But they have no alternative to the US security umbrella –Will China develop geo-strategic ambitions in the Gulf. Not any time soon….")

Similar presentations