Download presentation

Presentation is loading. Please wait.

1

Financial Performance Measurement chapter 16

2

Foundations of Financial Performance Measurement OBJECTIVE 1: Describe the objectives, standards of comparison, sources of information, and compensation issues in measuring financial performance.

3

Exhibit 1: Selected Segment Information for Goodyear Tire & Rubber Company

4

Exhibit 2: Listing from Mergent’s Handbook of Dividend Achievers

7

Foundations of Financial Performance Measurement Financial performance measurement comprises all the techniques that users of financial statements employ to show relationships in an organization’s financial statements and to relate those relationships to the organization's financial objectives.

8

Foundations of Financial Performance Measurement Users of financial statements are classified as either internal or external. –Internal users include top managers who set and strive to achieve financial performance objectives, middle-level managers of business processes, and employee stockholders. –External users include creditors and investors wanting to assess how well managers accomplished their financial objectives and customers forming cooperative agreements with the company.

9

Foundations of Financial Performance Measurement Management is responsible for devising, executing, monitoring, and reporting on a complete financial plan for a business that focuses on the following: –Liquidity—ability to pay bills when due and to meet unexpected needs for cash –Profitability—ability to earn a satisfactory net income –Long-term solvency—ability to survive for many years

10

Foundations of Financial Performance Measurement Management is responsible for devising, executing, monitoring, and reporting on a complete financial plan for a business that focuses on the following: (cont.) –Cash flow adequacy—ability to generate sufficient cash through operating, investing, and financing activities –Market strength—ability to increase the wealth of owners

–Cash flow adequacy—ability to generate sufficient cash through operating, investing, and financing activities –Market strength—ability to increase the wealth of owners")

11

Foundations of Financial Performance Measurement Creditors and investors use financial statement analysis in two ways. –To judge past performance and current position –To judge future potential and the risk associated with it

12

Foundations of Financial Performance Measurement Decision makers judge performance in (at least) three ways. –Rule-of-thumb measures –Analysis of past performance –Comparison with industry norms (discuss limitations)

.")

13

Foundations of Financial Performance Measurement Source of Information –A company’s annual report provides a significant amount of information. –Interim financial statements may indicate recent changes in earnings.

14

Foundations of Financial Performance Measurement Incentive bonuses and stock options for top executives are typically based on the company's achievement of certain financial goals. For public companies, a compensation committee of independent directors must establish remuneration policy for top-level executives, and the components and criteria used must be reported to the SEC.

15

©2011 Cengage Learning All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

16

Tools and Techniques of Financial Analysis OBJECTIVE 2: Apply horizontal analysis, trend analysis, vertical analysis, and ratio analysis to financial statements.

17

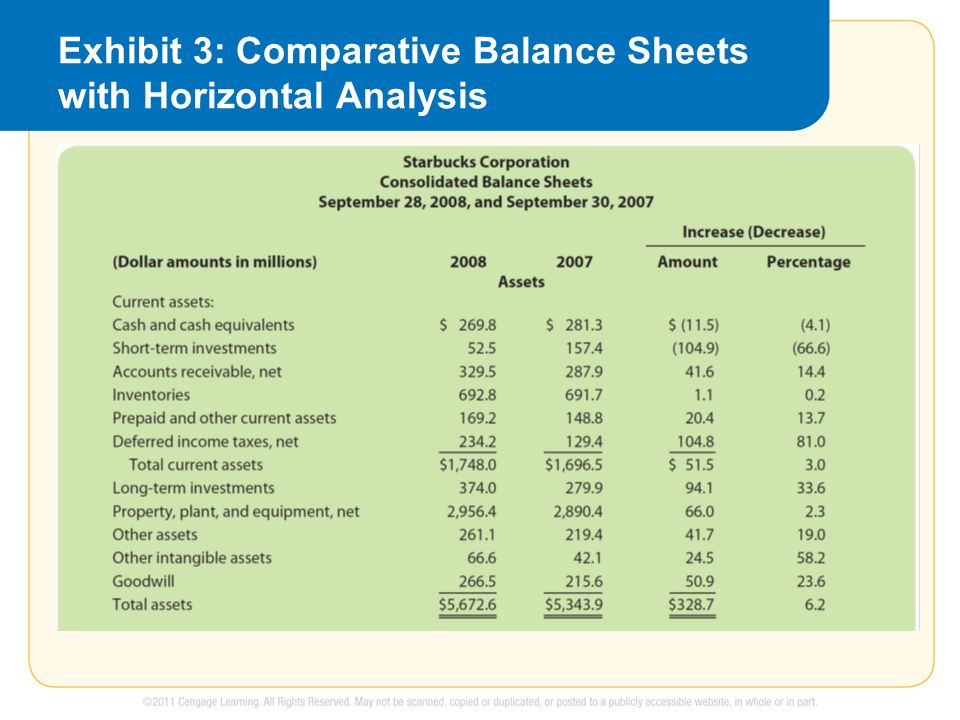

Exhibit 3: Comparative Balance Sheets with Horizontal Analysis

20

Exhibit 4: Comparative Income Statements with Horizontal Analysis

23

Exhibit 5: Trend Analysis

24

Figure 1: Graph of Trend Analysis Shown in Exhibit 5

25

Figure 2: Common-Size Balance Sheets Presented Graphically

26

Exhibit 6: Common-Size Balance Sheets

27

Figure 3: Common-Size Income Statements Presented Graphically

28

Exhibit 7: Common-Size Income Statements

29

Tools and Techniques of Financial Analysis Horizontal analysis shows absolute and percentage changes from one year to the next. –The first of the two years being considered is called the base year. –The percentage change is computed by dividing the amount of the change by the base year amount.

30

Tools and Techniques of Financial Analysis Trend analysis is an application of horizontal analysis over several consecutive years. –This approach uses an index number, with the base year set at 100 percent, against which changes in related items are measured.

31

Tools and Techniques of Financial Analysis Vertical analysis calculates percentage relationships within a single statement. –The result is a common-size statement. On a common-size balance sheet, total assets and total liabilities and equity in their respective areas of the balance sheet are labeled 100 percent. On a common-size income statement, net sales or net revenues are labeled 100 percent. Common-size statements can be presented in comparative form.

32

Tools and Techniques of Financial Analysis Ratio analysis shows meaningful relationships between financial statement components. –Ratios are useful in evaluating a company’s financial position and operations and in comparing financial data for several years or for several companies. –The primary purpose of ratios is to identify areas needing further investigation.

33

©2011 Cengage Learning All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

34

Comprehensive Illustration of Ratio Analysis OBJECTIVE 3: Apply ratio analysis to financial statements in a comprehensive evaluation of a company’s financial performance.

35

Figure 4: Starbucks’ Operating Cycle

36

Exhibit 8: Liquidity Ratios of Starbucks Corporation

38

Exhibit 9: Profitability Ratios of Starbucks Corporation

39

Exhibit 10: Long-Term Solvency Ratios of Starbucks Corporation

40

Exhibit 11: Cash Flow Adequacy Ratios of Starbucks Corporation

41

Exhibit 12: Market Strength Ratios of Starbucks Corporation

42

Comprehensive Illustration of Ratio Analysis Ratio analysis provides information about a company’s liquidity, profitability, long- term solvency, cash flow adequacy, and market strength.

43

Comprehensive Illustration of Ratio Analysis There are five major types of ratios. –Liquidity ratios Current ratio Quick ratio Receivable turnover Days’ sales uncollected Inventory turnover Average days’ inventory on hand Payables turnover Average days’ payable

44

Comprehensive Illustration of Ratio Analysis There are five major types of ratios. (cont.) –Profitability ratios Profit margin Asset turnover Return on assets Return on equity

–Profitability ratios Profit margin Asset turnover Return on assets Return on equity.")

45

Comprehensive Illustration of Ratio Analysis There are five major types of ratios. (cont.) –Long-term solvency ratios Debt to equity ratio Interest coverage ratio

–Long-term solvency ratios Debt to equity ratio Interest coverage ratio.")

46

Comprehensive Illustration of Ratio Analysis There are five major types of ratios. (cont.) –Cash flow adequacy ratios Cash flow yield Cash flows to sales Cash flows to assets Free cash flow

–Cash flow adequacy ratios Cash flow yield Cash flows to sales Cash flows to assets Free cash flow.")

47

Comprehensive Illustration of Ratio Analysis There are five major types of ratios. (cont.) –Market strength ratios Price/earnings ratio Dividends yield

–Market strength ratios Price/earnings ratio Dividends yield.")

48

©2011 Cengage Learning All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Similar presentations

2004 Prentice Hall, Inc. The Analysis of Financial Statements This chapter will develop tools and.>")