Download presentation

Presentation is loading. Please wait.

1

MI and the First-Time Homebuyer PRESENTED BY: Geoffrey Cooper, Director – Customer Solutions, MGIC Helping Renters Overcome Barriers to Homeownership

2

Mortgage Market and MI Trends Renters and First-Timers MI Cost Comparisons HFA Programs: Ideal for First-Time Home Buyers AGENDA Agenda

3

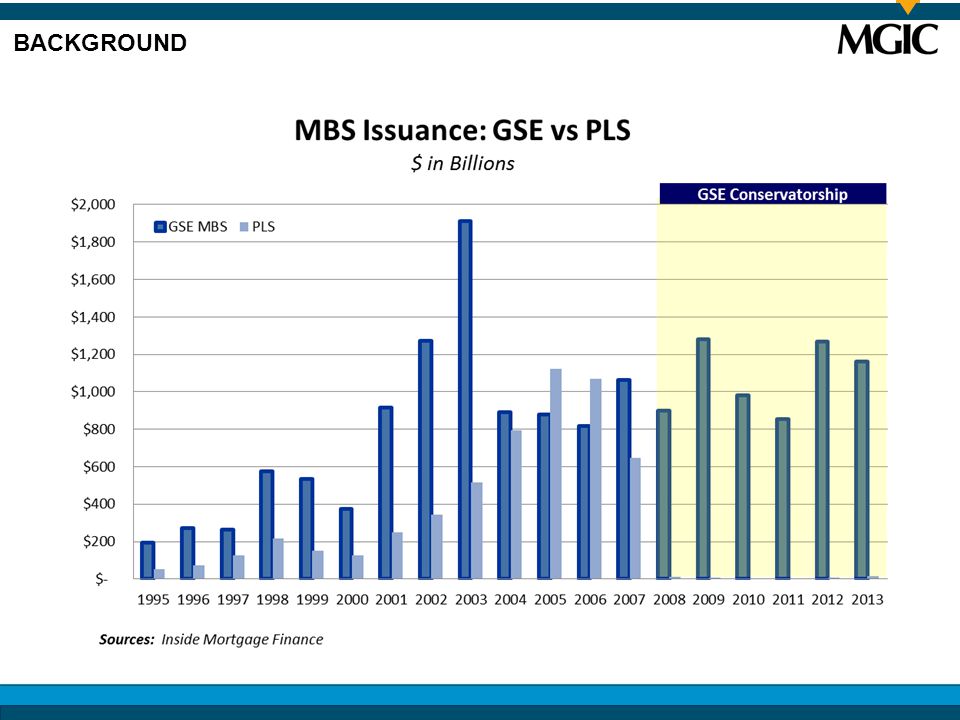

BACKGROUND

5

MI TRENDS

7

Old Habits Die Hard? MI TRENDS The Facts Tell a Different Story …

8

For the first time since 2007, more loans are being insured with MI than FHA MI TRENDS MI is On The Rise

9

MI Costs Less … … and is Cancellable MI TRENDS MI - Monthly (Standard Programs) MI - Monthly (HFAs, MyCommunity® and Home Possible®) FHA Upfront MIP0.00% 1.75% Renewal Rates:760 FICO 97% LTVNA0.57%96.5% LTV – 1.25% 95% LTV0.54%0.43%1.20% 90% LTV0.39%0.29%1.20% 85% LTV0.23%0.21%1.20% Note: FHA premiums increased effective April 9, 2012, HUD Mortgagee Letter 12-04. Scenario assumes 30-year fixed-rate mortgage. 0.77% less than FHA!

10

MI Costs Less … … and is Cancellable MI TRENDS MI - Monthly (Standard Programs) MI - Monthly (HFAs, MyCommunity® and Home Possible®) FHA Upfront MIP0.00% 1.75% Renewal Rates:680 FICO 97% LTVNA0.80%96.5% LTV – 1.25% 95% LTV0.89%0.67%1.20% 90% LTV0.57%0.39%1.20% 85% LTV0.33%0.29%1.20% Note: FHA premiums increased effective April 9, 2012, HUD Mortgagee Letter 12-04. Scenario assumes 30-year fixed-rate mortgage. 0.53% less than FHA!

11

MI Costs Less … … and is Cancellable MI TRENDS MI - Monthly (Standard Programs) MI - Monthly (HFAs, MyCommunity® and Home Possible®) FHA Upfront MIP0.00% 1.75% Renewal Rates:640 FICO 97% LTVNA0.94%96.5% LTV – 1.25% 95% LTV1.15%0.74%1.20% 90% LTV0.71%0.47%1.20% 85% LTV0.39%0.33%1.20% Note: FHA premiums increased effective April 9, 2012, HUD Mortgagee Letter 12-04. Scenario assumes 30-year fixed-rate mortgage. 0.46% less than FHA!

12

39% of First-Time Home Buyers used FHA financing in 2013, down from 56% in 2010 (National Association of Realtors) This means Conventional lending with MI has picked up among First-Time Home Buyers Fannie and Freddie loans with down payments of less than 20% require MI The use of First-Time Home Buyer programs, such as Fannie Mae’s MyCommunity®, Freddie Mac’s Home Possible®, and programs offered by Housing Finance Agencies are on the rise MI TRENDS First-Time Home Buyers Are a Major Driving Force Behind MI Growth

This means Conventional lending with MI has picked up among First-Time Home Buyers Fannie and Freddie loans with down payments of less than 20% require MI The use of First-Time Home Buyer programs, such as Fannie Mae’s MyCommunity®, Freddie Mac’s Home Possible®, and programs offered by Housing Finance Agencies are on the rise MI TRENDS First-Time Home Buyers Are a Major Driving Force Behind MI Growth")

13

RENTERS Source: National Association of Realtors Profile of Home Buyers and Sellers

14

Millennials Born between 1985-2003 (age 11-30) Children of Baby Boomers 28% of Nation’s population (88 million people) Gen Xers Born between 1965-1984 (age 30-49) 28% of Nation’s population (88 million people) RENTERS Who Are Today’s First-Time Home Buyers?

Children of Baby Boomers 28% of Nation’s population (88 million people) Gen Xers Born between (age 30-49) 28% of Nation’s population (88 million people) RENTERS Who Are Today’s First-Time Home Buyers")

15

RENTERS Millennials and Gen Xers hardest hit by Great Recession

16

RENTERS Source: Fannie Mae National Housing Survey Topic Analysis, May 2014 Young Renters Believe Buying a Home Will be Too Difficult For Them Right Now

17

Source: Fannie Mae National Housing Survey Topic Analysis, May 2014 RENTERS Young Renters See Credit, Lack of Savings, and Income as Primary Barriers to Buying Now

18

RENTERS

21

Source: Fannie Mae National Housing Survey Topic Analysis, May 2014 The Myth of the Renter Generation: Young Renters Want to Buy At Some Point

22

The Cost of Waiting: Purchasing Power Falls as Interest Rates Rise COST COMPARISONS 6.00% $1,109 $1,140$1,171$1,202$1,232 5.75%$1,082$1,112$1,142$1,172$1,202 5.50%$1,055$1,084$1,114$1,143$1,172 5.25%$1,028$1,056$1,086$1,114$1,142 5.00%$1,002$1,029$1,058$1,085$1,113 4.75%$976$1,003$1,031$1,057$1,084 4.50%$950$976$1,004$1,030$1,056 Purchase Price $180,000 $185,000 $190,000 $195,000 $200,000 MGIC Estimate includes P&I + MI payment, assuming 760 FICO and 5% down

23

Monthly Payment Comparison: 760 FICO, 95% LTV, Standard Coverage COST COMPARISONS Source: MGIC online calculator, https://content.mgic.com/calculators/servlet

24

Monthly Payment Comparison: 720 FICO, 95% LTV. Standard Coverage COST COMPARISONS Source: MGIC online calculator, https://content.mgic.com/calculators/servlet

25

Monthly Payment Comparison: 680 FICO, 95% LTV, Standard Coverage COST COMPARISONS Source: MGIC online calculator, https://content.mgic.com/calculators/servlet

26

Monthly Payment Comparison: 660 FICO, 95% LTV, Standard Coverage COST COMPARISONS Source: MGIC online calculator, https://content.mgic.com/calculators/servlet

27

Other Considerations: 660 FICO, 95% LTV, Standard Coverage COST COMPARISONS Source: MGIC online calculator, https://content.mgic.com/calculators/servlet Note: Monthly MI cancelled in Month 62 based on 3% annualized home price appreciation

28

Give Me the Lowest Cash-to-Close Option Available 720 FICO, HFA Preferred, Conventional 97% LTV vs. FHA 96.5% LTV HFAs Source: MGIC online calculator, https://content.mgic.com/calculators/servlet

29

97% LTV / 105% CLTV Reduced MI coverage Gifts and grants may be used to reduce borrower own funds required to close, subject to NM MFA requirements Best secondary market product available for overcoming the barriers to homeownership cited by renters HFAs HFA Preferred is Available Through New Mexico Mortgage Finance Authority

30

Geoffrey F. Cooper Director – Customer Solutions 414.347.2738 Geoff_cooper@mgic.com QUESTIONS?

Similar presentations

![Remove this text and place lender logo here [Name of Presenter] [Date Presented]](/15/4672282/big_thumb.jpg "Remove this text and place lender logo here [Name of Presenter] [Date Presented]>")