Download presentation

Presentation is loading. Please wait.

1

Business Finance 4228/7225 Advanced Investment Analysis The Stock Market Summer 2013 Sector Team Neil Patel Jeffrey Mulac Srinath Potlapalli Summer 2013 Sector Team Neil Patel Jeffrey Mulac Srinath Potlapalli

2

Overview

3

IT Sector Weight SIM vs S&P 500 As of 5/31/2013

4

IT Sector – Industry Classification Broadly Classified into Application Software - MS Office, Accounting and Financial Software, CAD/CAM/CAE Software, ERP Software etc. Communications Equipment – Telephone, Radio, Pager, Intercom and Automated Voice Answering System etc. Computer Hardware – Computer CPU, Monitor, Keyboard, Mouse, Monitor, Printer and Wireless Router etc. Semiconductor Equipment – Laser Scanning, Microscope Systems, X-ray and CT Inspection. Semiconductors – Microprocessors, SOC, Ics and Transistors. System Software – MS Windows OS, Linux OS, RDBMS, Mobile Device OS, Antivirus Software. Broadly Classified into Application Software - MS Office, Accounting and Financial Software, CAD/CAM/CAE Software, ERP Software etc. Communications Equipment – Telephone, Radio, Pager, Intercom and Automated Voice Answering System etc. Computer Hardware – Computer CPU, Monitor, Keyboard, Mouse, Monitor, Printer and Wireless Router etc. Semiconductor Equipment – Laser Scanning, Microscope Systems, X-ray and CT Inspection. Semiconductors – Microprocessors, SOC, Ics and Transistors. System Software – MS Windows OS, Linux OS, RDBMS, Mobile Device OS, Antivirus Software.

5

Five Largest IT Companies CompanyIndustryMarket Cap Ticker/Share Price Apple IncHardware/Electronic Equipment $391.81bAAPL/$417.42 Google IncInternet Software & Services $296.43bGOOG/$893.49 Microsoft CorpSystems Software/ Application Software $285.69bMSFT/$34.21 IBM CorpIT Consulting & Services$216.14bIBM/$194.93 Oracle CorpSystem Software/ Application Software $144.43bORCL/$31.19 As of July 05 2013, IT sector has performed + 7.68% YTD + 2.09% QTD Share price and market cap as of Jul 5,2013

6

Business Analysis

7

Phase of the life cycle (Information Technology): Inception around Word War II(1946). Significant growth followed in1980’s. Corporate IT Expansion took off in 1990’s. IT sector is highly cyclical. Nevertheless this sector adds value to the businesses and consumers alike and attracts significant investment allocations from Corporations and Government. We consider IT sector is in Growth to Mature phase. IT Sector remains ahead of Market in terms of Risk and Return premium. Information Technology IT Sector is mature but constantly growing with innovation

8

Business Analysis IndustryClassification by Business Cycle Communication Equipment Growth but cyclical and irregular. Manufacturing is impacted by foreign markets. Computer HardwarePC Hardware industry is in mature phase and is declining. Smartphone/Mobile devices/Tablets industry is in growth phase and is cyclical. Server hardware is in growth due to demand in cloud computing and data centers. Systems SoftwareGrowing with big data and cloud markets as drivers. IT Consulting and Services Mature and cyclical. It’s a globally driven industry. Internet Software and Service High growth and cyclical. Semiconductor Equipment Mature and cyclical. SemiconductorsMature and cyclical.

9

Business Analysis External factors: Global demand and business cycles, business process outsourcing, government regulations, market volatility, corporate spending, consumer spending and economic trends such as interest rates. The user and geography: Corporations and government sector, varied consumer demographics, developed economies, emerging markets. Input/output analysis: Significantly interlinked global economic system. IT sector can be significantly impacted by global resource supply and global product demand. IT industries such as hardware and semiconductors that are heavily dependent on global manufacturing resources are impacted. New capacity and global supply: Capacity demand in - server/cloud markets, online retailing, Internet software services, wireless networks. Global supply concentrated in manufacturing, software human resources and knowledge capital, manufacture of mobile device/smartphone sector. External factors: Global demand and business cycles, business process outsourcing, government regulations, market volatility, corporate spending, consumer spending and economic trends such as interest rates. The user and geography: Corporations and government sector, varied consumer demographics, developed economies, emerging markets. Input/output analysis: Significantly interlinked global economic system. IT sector can be significantly impacted by global resource supply and global product demand. IT industries such as hardware and semiconductors that are heavily dependent on global manufacturing resources are impacted. New capacity and global supply: Capacity demand in - server/cloud markets, online retailing, Internet software services, wireless networks. Global supply concentrated in manufacturing, software human resources and knowledge capital, manufacture of mobile device/smartphone sector.

10

Business Analysis Profitability and Pricing Higher profit margins are due to : Growing sector of mobile devices, tablets and smartphones. Data center servers and Cloud computing software markets. Software Services such as big data and BI Analytics. Mergers and Acquisitions activities. Pressure on profits and pricing power due to: Maturity in Semiconductor industry and electronic components, goods and services. Conglomerates. Ex: HP. Volatility of demand in emerging markets. IP rights infringement in global IT industry. Competition and price pressure from foreign manufacturing goods and software services. Higher R&D costs and manufacturing costs. IT consolidation. Higher profit margins are due to : Growing sector of mobile devices, tablets and smartphones. Data center servers and Cloud computing software markets. Software Services such as big data and BI Analytics. Mergers and Acquisitions activities. Pressure on profits and pricing power due to: Maturity in Semiconductor industry and electronic components, goods and services. Conglomerates. Ex: HP. Volatility of demand in emerging markets. IP rights infringement in global IT industry. Competition and price pressure from foreign manufacturing goods and software services. Higher R&D costs and manufacturing costs. IT consolidation.

11

Business Analysis Porters Five Force Analysis

12

Economic Analysis

13

CPI Index

14

Real GDP

15

Disposable Income

16

Durables

17

Computer Spending

18

Capital Spending

19

S&P 500

20

Key Drivers Real GDP Durables Capital Spending Consumer Spending

21

Financial Analysis

22

Information Technology Sector 5 yr historical growth = 8% Last Qtr = 4% Last 12 Mths = 5% Q1 2012 to Q1 2013 = 4.4% Steady growth Qtr to Qtr and YoY

23

Information Technology Sector 5 yr historical growth = 18% Last Qtr = (1%) Last 12 Mths = 3% Long term Future Growth = 13% Q1 2012 to Q1 2013 = (1.1%) Cyclical sector, positive outlook

Last 12 Mths = 3% Long term Future Growth = 13% Q to Q = (1.1%) Cyclical sector, positive outlook")

24

Information Technology Sector

25

Computer Hardware (AAPL)

")

26

Internet Software & Svcs (GOOG)

")

27

IT Consulting Services (IBM)

")

28

System Software (MSFT & ORCL)

")

29

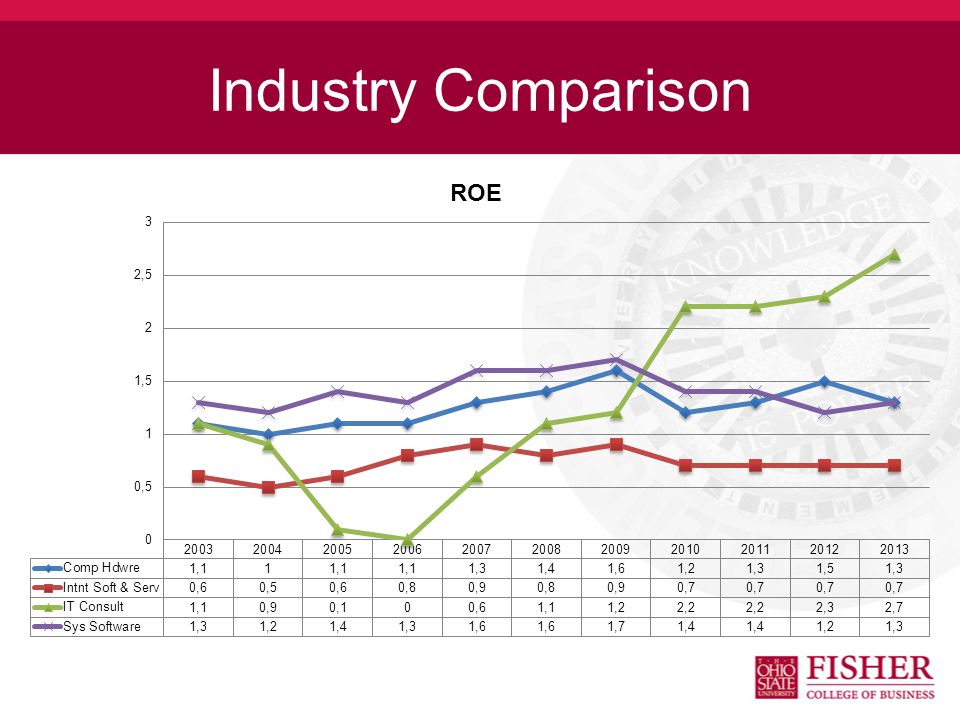

Industry Comparison

32

Valuation Analysis

33

Absolute Valuation IT sector is undervalued compared to its historical valuation P/E ratios are leaning towards historical lows

34

Relative Valuation IT sector is undervalued compared to the market when looking at P/E IT sector is lower than its historical median for every ratio (relatively at historical lows for P/E)

")

35

Valuation Differences between large companies within sector Apple undervalued? Google overvalued?

36

Recommendation

37

Overweight IT Sector in SIM portfolio by 100-200bps above S&P 500 weightage Positives: –IT Sector is underperforming the market by 7-8% YTD (buying opportunities) –Continued growth in the future –Improving economic conditions in the U.S. Risks: –Slowing growth in developing countries (mainly China and India) –Economic condition of Europe –Projected slowdown of government spending in U.S.

–Economic condition of Europe –Projected slowdown of government spending in U.S..")

38

Recommendation Overweight: –Application and systems software (big data software growing in demand) –Hardware (mobile sales continue to grow) –Internet software and services (cloud computing) Underweight: –PC semiconductors and equipment (decreasing demand) –PC hardware (decreasing demand) –IT consulting & services

–Hardware (mobile sales continue to grow) –Internet software and services (cloud computing) Underweight: –PC semiconductors and equipment (decreasing demand) –PC hardware (decreasing demand) –IT consulting & services")

39

Questions?

Similar presentations

Covering Analyst: Cameron Schwartz>")

Analysts: Chris Landqvist, Justin Pippitt, Kelli Coldiron & Wei Pi.>")

Bharath Chandrashekhar Daniel Kleeman Shalini Sivarajah Presented: April 10, 2014.>")

>")

Marc Reitter Siddhesh Sankulkar T E L E C O M S E C.>")