Download presentation

Presentation is loading. Please wait.

1

With the financial support of Policies and price incentives for the rice sector in eight MAFAP pilot countries

2

Scope of the analysis 8 countries: Burkina Faso, Ghana, Kenya, Mali, Mozambique, Nigeria, Tanzania, Uganda Rice price incentives measured at two levels of the value chain: farmers and wholesalers/traders Period of analysis 2005-2010

3

Outline Commodity context Policy decisions and measures affecting the rice sector in the eight pilot countries Results of the price incentives analysis Key findings Recommendations

4

Average paddy rice production and production per capita in MAFAP countries (2005-10, million MT) Source: FAOSTAT, Food Balance Sheets

Source: FAOSTAT, Food Balance Sheets")

5

Average human consumption of rice in MAFAP countries, 2005-2009 Source: FAOSTAT, Food Balance Sheets

6

Trends in production, area and yields (2005-2010) Source: FAOSTAT, MAFAP calculations

Source: FAOSTAT, MAFAP calculations")

7

Imports as a share of domestic supply (2005-2010)

")

8

Policy context in the 8 countries Type of strategy/policyCountries CARD StrategyAll countries Input subsidies (not direct impact on prices) All except Uganda and Tanzania Price stabilization mechanisms (buffer stocks) All except Uganda and Mozambique Government charges (fees and levies)All countries Direct price interventionsMali and Burkina Faso Trade policies (PTAs; other non-tariff charges) All countries (WAEMU and ECOWAS; COMESA, EAC; SADC)

All except Uganda and Tanzania Price stabilization mechanisms (buffer stocks) All except Uganda and Mozambique Government charges (fees and levies)All countries Direct price interventionsMali and Burkina Faso Trade policies (PTAs; other non-tariff charges) All countries (WAEMU and ECOWAS; COMESA, EAC; SADC)")

9

Estimates of tariffs and other ad valorem charges (%) 200520062007200820092010 Kenya27.827.5 37.3 Uganda75 Tanzania76.4 NA Mozambique7.5 Burkina Faso13.5 13.5, 3.53.5, 13.513.5 Mali2.512.5 12.5, 2.512.5 Ghana36.9 36.9, 16.916.9, 36.936.9 Nigeria101.5 110.5110.5, 31.531.5

Kenya Uganda75 Tanzania76.4 NA Mozambique7.5 Burkina Faso , , Mali , Ghana , , Nigeria ,")

10

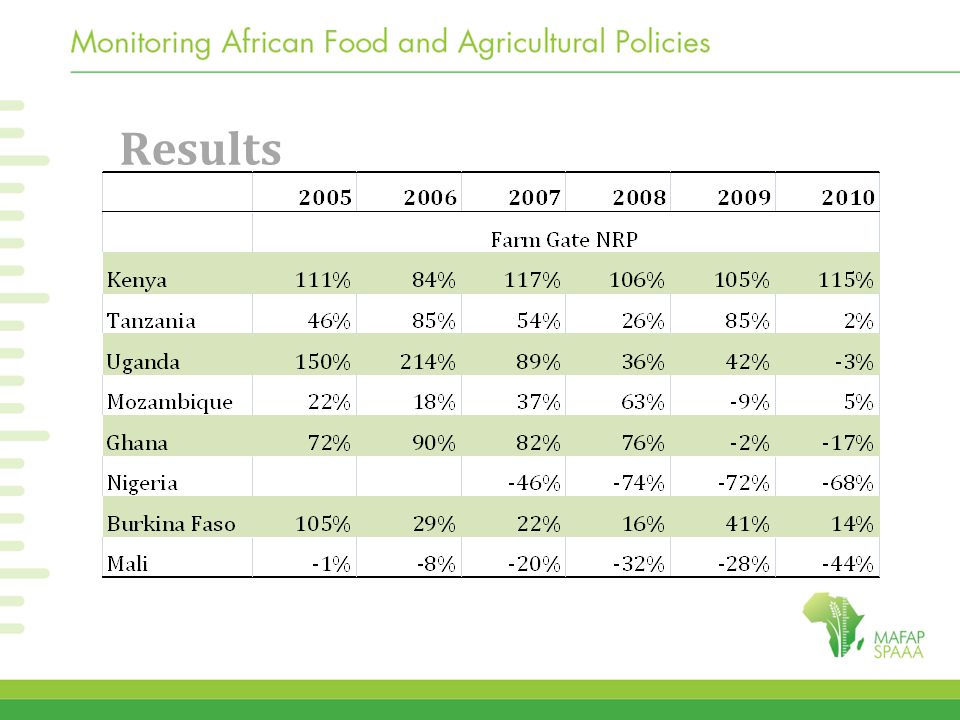

Results

12

Observed against expected NRPs WHOLESALEFARM GATE

13

KEY FINDINGS strong price incentives at the wholesale level in all countries due to high tariffs and high market access costs between the border and wholesale markets consumers commonly pay higher prices (despite policy objectives in favor of consumers) farmers receive lower prices than those expected in free, competitive markets with no policy interference

farmers receive lower prices than those expected in free, competitive markets with no policy interference")

14

Key findings Market access costs affecting farm prices are similar for a wide range of policy frameworks (fees and compliance costs at road check points, ports and markets, disadvantage of small scale farmers in price negotiation); Even when import tariffs are in place, these are less effective for farmers than they should be due to imperfect price transmission

; Even when import tariffs are in place, these are less effective for farmers than they should be due to imperfect price transmission")

15

Way forward Expand agricultural sector analysis in Africa from traditional policy focus towards the functioning of commodity value chains Design interventions aimed at minimizing access costs to increase price transmission to farmers, while reducing prices for consumers How to bridge the gap?

16

THANK YOU!

17

Farm gate and wholesale prices for local rice in Ghana (GhÇ/100Kg)

")

Similar presentations

Food and Agriculture Organization of the United Nations How did international price movements affect.>")

Food and Agriculture Organization of the United Nations National rice policies in Asia David Dawe Agricultural.>")