Download presentation

Presentation is loading. Please wait.

1

Wells Fargo Economics Navigating the Aftermath Scott Anderson, Ph.D. Vice President | Senior Economist U.S. Outlook Durango, Colorado Friday, January 8, 2010 © 2009 Wells Fargo Bank, N.A. All rights reserved.

2

11 The Great Recession of 2008 - 2009

3

2

4

3

5

4

6

5

7

6

8

7

9

88 Bank Credit Crisis: Not Out of the Woods Yet

10

9

11

10

12

11

13

12

14

13

15

14

16

15

17

16

18

17

19

18 Demand And Supply Factors Limit Credit Growth!

20

19 U.S. Growth Resumes in Q3

21

20

22

21

23

22

24

23

25

24

26

25 Housing Market Hits Bottom

27

26

28

27

29

28

30

29 The Fed Soothes the Financial Crisis – Focus Shifts to Exit Strategy

31

30

32

31 Liquidity Almost Back to Normal!

33

32

34

33 Fed Funds Increases Historically Lag Unemployment Peak Peak Unemployment Rate First Fed Funds Rate Increase Months Lag May-759.0%Apr-7611 Dec-8210.8%May-835 Jun-927.8%Feb-9420 Jul-036.2%Jun-0411 Avg. Lag11.8

35

34

36

35 Fiscal Stimulus a Major Factor

37

36

38

37 Worries Grow Over Government Deficits and Debt

39

38 Large Downside Risks Remain

40

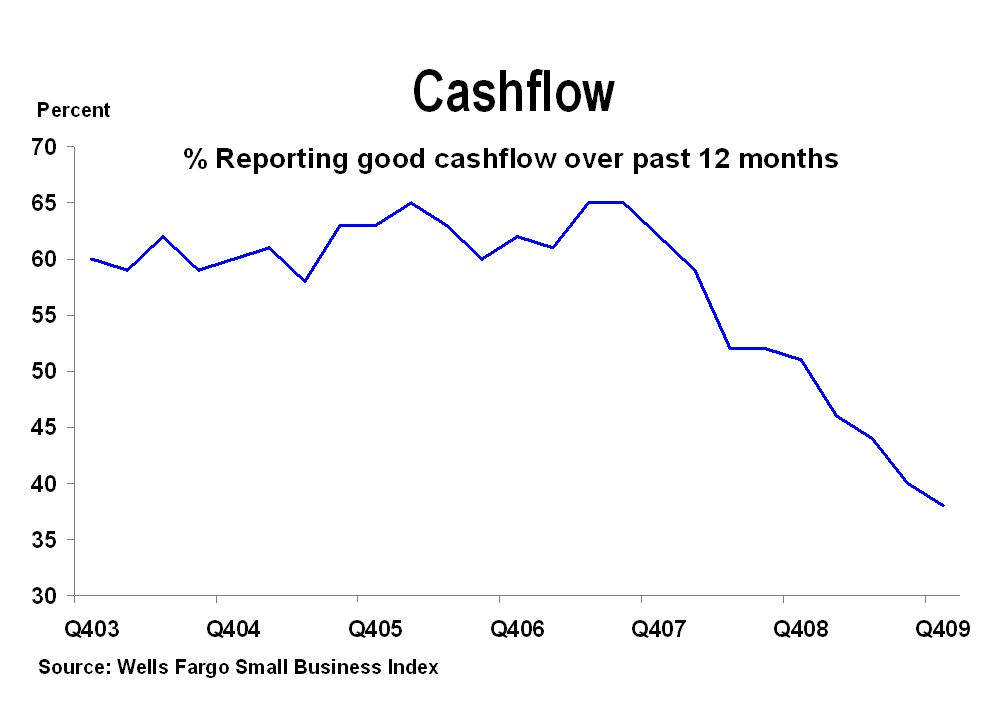

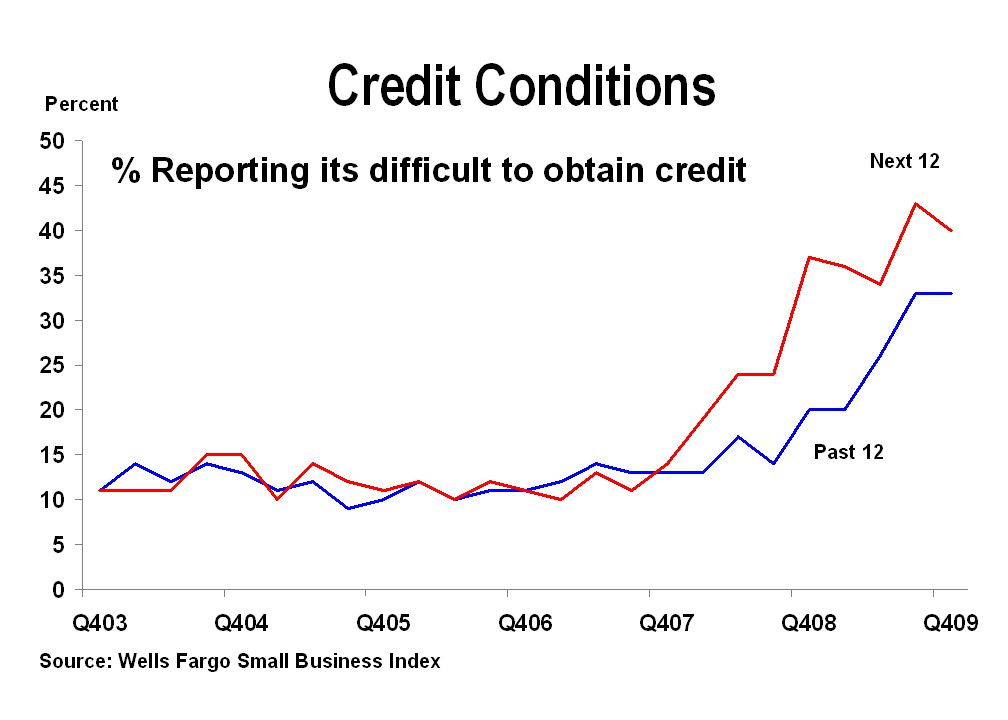

Small Business Current Conditions Revenues weaken further in Q4 Financial situation worsens Cash-flow remains poor Capital spending still weak, cutting slows Employment conditions worsen in Q4 Credit becomes more difficult to obtain

43

42

46

45

47

46

48

47 Growth in Year Following End of Recessions Average Increase* Outlook 2010 Real GDP5.8%2.8% Industrial Production9.6%6.4% Housing Starts20.3%36.2% Corporate Profits30.4%18.1% S&P 50014.1%5.2% * Past nine recessions

Similar presentations