Download presentation

Presentation is loading. Please wait.

1

Credit Derivatives

2

Credit Derivatives A credit derivative financial instrument

Allows participants to decouple credit risk from an asset and place it with another party

3

Credit Risk Credit risk is the risk of loss due to a Debtor's non-payment of a Loan or other line of Credit, either the Principal or Interest (Coupon) or both. To reduce or strip out Credit risk, Risk Manager may : Take Collateral Make loss provisions Actively manage the Credit Risk Exposure or use Credit Derivatives : Credit Default Swaps (CDS)

or both. To reduce or strip out Credit risk, Risk Manager may : Take Collateral. Make loss provisions. Actively manage the Credit Risk Exposure. or use Credit Derivatives : Credit Default Swaps (CDS)")

4

Credit Risk Downgrade Risk

- Rating agency reduces debtor’s credit rating - Reduces value of debt Default Risk - Loan not repaid in full - Future cash flows not certain

5

Rating Agencies Risk is measured by rating agencies - Moody’s - S&P

- Fitch Rating scales:

6

Types of Credit Derivatives

Credit Default Swap (almost 90% of all transactions) Dynamic Credit Default Swap Credit intermediation Swap Basket Credit Default Swap Total Rate of Return Swap Credit (spread) Option Downgrade Option Collateralized Instrument Credit-linked Note Synthetic Collateralized Debt Obligation

Dynamic Credit Default Swap. Credit intermediation Swap. Basket Credit Default Swap. Total Rate of Return Swap. Credit (spread) Option. Downgrade Option. Collateralized Instrument. Credit-linked Note. Synthetic Collateralized Debt Obligation.")

7

Credit Default Swaps CDS

7

8

First CDS introduced in 1995 by JP Morgan in an attempt to free up all that capital they were obliged, by federal law, to keep in reserve in case any of their loans went ‘bad’. Estimated Size of the CDS market (Q1 2008): USD 65 trillion Global GDP: USD 55 trillion (2007,IMF)

: USD 65 trillion. Global GDP: USD 55 trillion (2007,IMF)")

9

Characteristics of Credit Default Swaps

Market of CDS is divided in three sectors: Corporates Bank credits Emerging markets sovereign OTC agreement (privately negotiated transactions) CDS ranges in maturity from one to ten years Five year maturity is the most frequently traded CDS provides protection only against previously agreed upon credit events

CDS ranges in maturity from one to ten years. Five year maturity is the most frequently traded. CDS provides protection only against previously agreed upon credit events.")

10

Credit Events According to ISDA 2003 Master Agreement Bankruptcy

(insolvency or inability to pay its debts) Failure to pay (principal or interest) Debt Restructuring (change in the terms of the debt that are adverse for creditors) Repayment Acceleration on Default Repudiation (sovereign only – indication that a debt is no longer valid) One of this event has to have happened on the reference entity in order a CDS payment to be made

Failure to pay. (principal or interest) Debt Restructuring. (change in the terms of the debt that are adverse for creditors) Repayment Acceleration on Default. Repudiation. (sovereign only – indication that a debt is no longer valid) One of this event has to have happened on the reference entity in order a CDS payment to be made.")

11

What is a single CDS Bilateral contract

Protection buyer pays premium to protection seller Protection seller contingent payment upon default of reference asset One party usually owns the Reference asset Otherwise: transaction does not involve credit exposure speculation on behalf of both parties Premium paid is known CDS Spread

12

Reference Asset Bank loan Corporate debt Trade receivables

Emerging market debt Convertible securities Credit exposures from other derivatives

13

CDS Spread Quoted in Basis Points per annum Paid periodically

If corporate quarterly sovereign monthly Credit Spread =Default probability x (1-recovery rate) Premium = notional amount x CDS spread p.a.

Premium = notional amount x CDS spread p.a.")

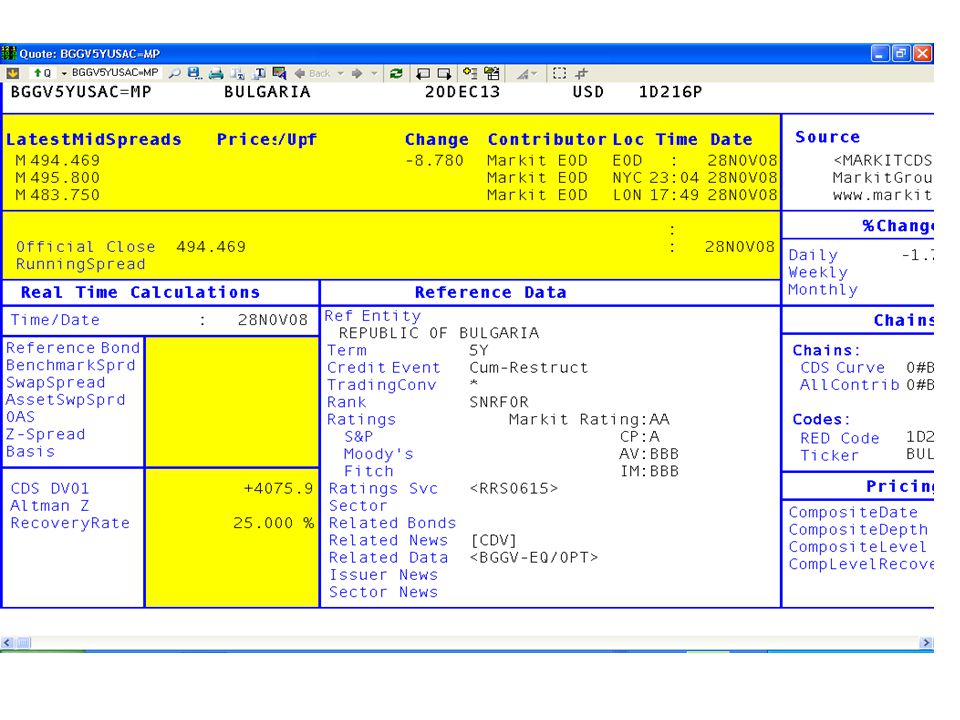

15

Example on Premium of Bulgarian 5Y CDS

Notional amount = USD10,000,000 Spread= 494 b.p. Premium = notional amount x CDS spread = 10,000,000 x = 494,000 p.a.

16

Payoff from CDS The payoff can be defined in terms of

Physical delivery of the reference asset delivery of the Defaulted Bond for the Par value (no later than 30 days after the credit event) or Cash Settlement pays the Protection Buyer the difference between the Par value and (real) Recovery value of the Bond (within 5 days of the credit event) Settlement terms of a CDS are determined when the CDS contract is written

or. Cash Settlement. pays the Protection Buyer the difference between the Par value and (real) Recovery value of the Bond (within 5 days of the credit event) Settlement terms of a CDS are determined when the CDS contract is written.")

17

Buyers and sellers of protection

18

Cash Settlement Example Payoff from a Credit Default Swap

Bank A holds a corporate bond issued by C Reference asset Bond C, maturing in two years

19

Cash Settlement Example Payoff from a Credit Default Swap

To reduce credit risk: Bank A enters in two year CDS with Bank B, with notional amount 10 millions (protection buyer) Bank B contingent payment to A in the event of default of reference asset C (protection seller)

Bank B contingent payment to A in the event of default of reference asset C (protection seller)")

20

Cash Settlement Example Payoff from a Credit Default Swap

Bank A pays periodically the premium to Bank B CDS on C is quoted 52 bps (per annum) Premium= notional Amount x CDS spread = 10,000,000 x = 52,000

Premium= notional Amount x CDS spread. = 10,000,000 x = 52,000.")

21

Cash Settlement Example Payoff from a Credit Default Swap

After one year: C defaults on the bond by declaring bankruptcy Market value falls to 48.63% of its par value because Market expectation is that C will only be able to pay back 48.63% of total outstanding

22

Cash Settlement Example Payoff from a Credit Default Swap

The payoff on default will be calculated as follow Notional principal x Par Value – Market Value

23

Cash Settlement Example Payoff from a Credit Default Swap

Bank B makes payment to Bank A USD 10,000,000 x (100–48.63)/100 =USD 5,137,000

/100 =USD 5,137,000.")

24

Cash Settlement Example Payoff from a Credit Default Swap

Net effect CDS allowed Bank A to insulate itself from credit risk by holding the risky bond C The payoff from sale of reference asset: USD 10,000,000 x = 4,863,000

25

Cash Settlement Example Payoff from a Credit Default Swap

Bank A receives the recovery rate from the sale of the underlying reference asset USD 4,863,000 and payoff of USD 5,137,000 from Bank B Total 10,000,000 Bank B acquired the credit risk of holding the bond without actually holding it in return for receiving the premium from BankA

26

Use of CDS Hedging Protection buyer owns the underlying credit asset

Speculation Protection buyer does not have to own the underlying asset

27

Hedging CDS manage the credit risk

Protection buyer hedge their exposure by entering into CDS contract IF reference asset defaults the proceeds from CDS will cancel out the losses on the underlying Protection buyer will have lost only the payments over that time IF reference asset does not default protection buyer makes the payments reducing investments returns but eliminates the risk of loss due to reference entity defaults

28

Speculation Investor speculates on changes in an entity’s credit quality If credit worthiness declines => CDS spread will increase If credit worthiness increases => CDS spread will decline Example: a hedge fund believes an Entity will default soon buys protection

29

Speculation IF reference asset defaults

Protection buyer will have paid the premium but will receive from the protection seller the notional amount making a profit. IF reference asset does not default CDS contract will run for whole duration without any return

30

Speculation The hedge fund could liquidate its position after a certain period of time lock in its gains or losses IF reference asset is more likely to default => CDS Spread widens So, hedge fund sells protection for the rest of CDS duration at a higher rate => makes profit (given that reference asset does not default during this time) IF reference asset is much less likely to default => CDS spread tightens So, hedge fund again sells protection for the rest of CDS duration in order to eliminate the loss that would have occurred

IF reference asset is much less likely to default => CDS spread tightens. So, hedge fund again sells protection for the rest of CDS duration in order to eliminate the loss that would have occurred.")

Similar presentations

is a contract in which a buyer pays a payment to a seller to take on the credit.>")