Download presentation

Presentation is loading. Please wait.

1

The Economic and Financial Outlook Darryl Gobbett Managing Director Chief Economist Representative and Adviser Prescott Securities Ltd AFSL 228894 Adelaide – Thursday, 5 June 2014 © Governance Institute of Australia

2

Any advice contained in this presentation is general advice based on the investment merits of the security or issuer alone without taking into account any person’s investment objectives, financial situation and particular needs. The information contained within this presentation was compiled by Prescott Securities Limited (PSL) and PSL provide no warranty regarding the accuracy or completeness of the information. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice by PSL. PSL assume no obligation to update this presentation after it has been presented. Except for any liability which by law cannot be excluded PSL, its Directors, employees and agents disclaim all liability (whether in negligence or otherwise) for any error, inaccuracy in, or omission from the information contained in this document or any loss or damage suffered by the recipient or any other person directly or indirectly through relying upon the information. Before making an investment decision based on such advice, the recipient must decide whether it is appropriate to his/her needs or seek specific professional advice. Should you consider the acquisition of a particular financial product as a result of the material contained, you should obtain a copy of and consider the Product Disclosure Statement for that product before making any decision. PSL may receive a fee for advice and/or the implementation of an investment decision. PSL and their representatives may have financial interests in some/any of the product(s) included within this presentation. Prescott Securities Limited (PSL) is the holder of an Australian Financial Services Licence No: 228894.

and PSL provide no warranty regarding the accuracy or completeness of the information. All opinions, conclusions, forecasts or recommendations are reasonably held at the time of compilation but are subject to change without notice by PSL. PSL assume no obligation to update this presentation after it has been presented. Except for any liability which by law cannot be excluded PSL, its Directors, employees and agents disclaim all liability (whether in negligence or otherwise) for any error, inaccuracy in, or omission from the information contained in this document or any loss or damage suffered by the recipient or any other person directly or indirectly through relying upon the information. Before making an investment decision based on such advice, the recipient must decide whether it is appropriate to his/her needs or seek specific professional advice. Should you consider the acquisition of a particular financial product as a result of the material contained, you should obtain a copy of and consider the Product Disclosure Statement for that product before making any decision. PSL may receive a fee for advice and/or the implementation of an investment decision. PSL and their representatives may have financial interests in some/any of the product(s) included within this presentation. Prescott Securities Limited (PSL) is the holder of an Australian Financial Services Licence No:")

3

World Outlook Improving But Bringing More Challenges 2014 will be 6 th year of growth globally Spending, Output and Profits higher than 2007 peaks Portugal, Ireland and Greece now accessing capital markets North America, China, Asia, Africa to grow strongly Europe and Japan still slow, Australia slowing Inflation alongside fears of Deflation Interest rates to stay low House and Commodity prices lifting Public Sector deficits shrinking Companies doing very well Profits, Cash flows, Balance sheets Another surge of change coming

4

The Big Issues and Trends Structural Change is accelerating The world is changing –Urbanisation, Increasing Wealth, Ageing –Second Rise of Asia –Freeing up of markets –Climate change –Technology, Innovation oImmediate and mobile infotainment and value exchange o3D printing; Drones to deliver parcels; driverless cars oNew energies oBiosciences: gene technologies, growing human spare parts oMeta data More researchers than ever before

5

Patents (PCT) Applied For, by Country of Applicant Source: Organisation for Economic Cooperation and Development (OECD.statextracts)

Applied For, by Country of Applicant Source: Organisation for Economic Cooperation and Development (OECD.statextracts)")

6

The Big Issues and Trends Structural Change is accelerating Issues specific to Australia –$A, –Costs –Change of Governments, Budget tightening –Demographics oAgeing and more immigrant population oWorkforce, Health, Spending, Investments Australian Households still saving We spent the mining boom before it arrived –Another one within a decade Tourism and Agricultural surges on their way

7

Global Growth and Inflation Divergences, Low inflation and Interest Rates Output Growth, Inflation Adjusted, % pa 20092010201120122013e2014F2015F United States -2.6+2.4+1.8+2.8+1.9+2.8+3.0 Japan -6.3+4.5-0.8+1.4+1.7+1.4+1.0 Euro Area -4.1+2.0+1.4-0.7-0.4+1.2+1.5 China +9.2+10.4+9.2+7.7 +7.5+7.3 India +6.8+10.1+6.8+3.2+4.4+5.4+6.4 Indonesia +5.7+6.2+6.5+6.2+5.3+5.5+6.0 ASEAN 5 +1.7+7.0+4.5+5.4+5.8+4.9+5.4 Brazil -0.6+7.5+2.7+1.0+2.3+1.8+2.7 World Output -0.5+5.1+3.8+3.1+3.0+3.6+3.9 Inflation: Advanced Emerging +0.1 +5.2 +1.5 +6.1 +2.7 +7.2 +2.0 +6.1 +1.4 +5.8 +1.5 +5.5 +1.6 +5.2 $US 6mnth LIBOR 1.1%0.5% 0.7%0.4%+0.4%+0.8% Source: IMF, World Economic Outlook April 2014

8

US Growth back to Pre GFC levels Household consumption, Housing, Business Investment, Exports

9

Budget Deficits falling in Most Major Economies

10

Federal Reserve Board Taper Decisions are good news Source: US Federal Reserve Board 18-19 March 2014 Projections of Federal Reserve Board Members and Federal Reserve Bank Presidents, Central Tendency 201420152016 Economic Growth (Real), % pa2.8 – 3.03.0 – 3.22.5 – 3.0 Unemployment rate %6.1 – 6.35.6 – 5.95.2 – 5.6 Consumer Inflation% pa1.5 – 1.61.5 – 2.01.7 – 2.0 Based on more certainty of growth. Cash rates staying at 0-0.25% well into 2015. Declining US Budget deficits - Cut supply of new Bonds to under monthly purchases. Longer term US interest rates lifted from mid 2012 in anticipation

11

Tapering well anticipated: US Interest Rates up since mid 2012 Now easing

12

USA Labour Market Lifting Slowly but on Right track Unemployment at 6.7% in April, cf 10% 2009, 4.4% 2007

13

Risks already apparent for Australian Gas and Coal Exporters, Farmers, Manufacturers. Manufacturing shifting back to USA. China is estimated to have a bigger resource than USA USA defence positioning US Fraccing Gas Surplus now recognised as Game Changer

14

* Birinyi and Associates, Wall Street Journal Market Data Centre, 28/4/2014 US Corporates continue to increase Profits and Cash Holdings US Company Profits at Record Levels (Dec Qtr 13) on National Accounts Basis March qtr likely weather related. Likely further rises in 2014 and 2015 For S&P500 companies, Forward Price to Earnings Ratio now 15.7* vs 16.4 trailing ave (since 1954) “Cash” held by Non-Financial Corporates Dec 2013: $US1,581.1 billion Up 13% yoy Dec 2007Dec 2013 Cash/ Market Value of Equities 7.2%7.4% Debt/Net Worth42.8%47.1%

Cash held by Non-Financial Corporates Dec 2013: $US1,581.1 billion Up 13% yoy Dec 2007Dec 2013 Cash/ Market Value of Equities 7.2%7.4% Debt/Net Worth42.8%47.1%.")

15

Further Growth in Earnings per Share into 2014/15 is forecast Source: Yardeni Research Inc, 28 April 2014

16

Forward P/Es OK for low Inflation and Interest Rate Outlook Source: Yardeni Research Inc, 28 April 2014

17

Europe a basket case but no longer in Crisis Breakup of Eurozone and demise of Euro$ no longer issues Populations generally in favour of keeping Euro & European Union together Germans realised low Euro$ helped their exports Greeks recognised risks of being cast out Concern is more with how the politicians messed up so badly Recent elections indicate the depth of feelin Integrity of Eurozone always more than economics and politics Real fear of return of nationalism and war Human and Economic costs of breakup are high and unknown Status of individual countries in break-up would drop even further –Compared with USA, China, India, Russia

18

Risks remain –Still significant differences on work and business practices, productivity, social support Contributing to horrendous unemployment, deflation –Banks under undercapitalised, Private and Public Degearing –Populations generally growing slowly and rapidly ageing Bright Points –Technologies, fashions, brands: What the Emerging economies want Capital goods, Design services, inputs to manufacturing High end consumer items: autos, airplanes, wine, foods, medicals Buy the company – eg Volvo, Saab, Jaguar, Lenovo, RM Williams, Smithfield Foods, –Services: Financial, Medical, Business, Tourism, Education –Property as a possible bolt-hole from Asia and Middle East Europe a basket case but no longer in Crisis

19

Overseas Monetary Policies very Stimulatory Aim is to Increase Inflation to 2% Cash Rates: Financial Repression European Central Bank 0.25%, Bank of England 0.5%, USA 0.25%, Japan 0% Keep retail deposit and loan interest rates very low: USA eg –Mortgages: 30 Year fixed 4.25%, variable 3.26%; New car loan 5 yr 2.86% –CMA 0.62% (>$50,000), 5 year CD 1.4%, 10 year Bonds 2.7% Quantitative Easing To continue in Europe and Japan. oBuying long term public and private debt oAdditional offset to Budget deficit reductions Pullback now in USA and UK with stronger economies

20

Growth Driven by Emerging Economies’ Urbanisation & Middle Class Households Major Changes for Humanity Coming Down Out of the Trees Fire Agriculture Urbanisation Ageing

21

Spending by the Global Middle Class $US billion, 2005 Purchasing Power Parity Exchange Rates Source: OECD Development Centre Working Paper No 285, The Emerging Middle Class in Developing Countries, Jan 2010

22

Global Motor Vehicle Market Production of all motor vehicles, million Motor vehicle fleet 2011 20062013Total, millionPer 1000 people China5.70822.11711585 USA11.98011.045253812 Japan10.8009.63075589 Germany5.7585.71852634 South Korea3.6994.52119379 India1.6273.8812218 Brazil2.5283.74050259 The Rest27.12326.648 Total69.22387.300 Source: www.oica.net, wikipedia.orgwww.oica.net

23

Other sectors growing with Rising Urban Middle Classes Food More, Greater Diversity, Better, More Western – More Meat, Edible Oils, Dairy, Alcohol, Sugar, More take away – McDonalds aims to increase China stores by 50% to 2000 in 2013 – Yum! Brands in China has 3,300 KFC & 651 Pizza Hut: aim is 20,000 Services Travel, Education, Children’s expenses, Communication and Entertainment, Health Care, Aged Care, Financial Services – Chinese tourists biggest spenders globally and in Australia in 2011/12: – Indians likely to be next largest – More living past work – Diseases of the West and the Aged – More outsourcing of aged care Buying up Overseas Businesses, Farms and Resources – Motor vehicles, Pork, Dairy, Wine, Sugar, etc etc Focus on Brands, Quality, Authenticity

24

Interest in Australian Dairies is not to sell us more Iced Coffee

29

$A now about right on current $US Commodity Prices

31

China’s Growth on Target at 7.5 - 8.0% pa, but changing Source: RBA Statement on Monetary Policy, May 2014 Spread benefits of growth Increasing wages Lift Value Add in Industry Rising consumption Better and more housing 10 million new homes pa Increased outbound tourism Better care for Aged Reduced pollution More Western & better quality food Reduced regulation Finance Trade

32

Source: China 2030, World Bank and Development Research Centre of the State Council, the People’s Republic of China, 2012

33

Some Indicative Numbers for China 2011 Constant value $US201020202025% change on 2010 GDP, $US billion7,29815,46220,594+182% Investment, $US billion3,3865,8767,414+119% Consumption, $US billion3,5479,27812,975+266% Consumption per Head $US2,6306,6509,200250% Sources: China 2030, World Bank and Development Research Centre of the State Council, the People’s Republic of China, 2012 International Monetary Fund, Prescott Securities Ltd

34

Directions of Chinese Reforms Some points from 3 rd Plenary Session of 18 th CPC Central Committee – Improve and develop socialism with Chinese characteristics oBuild law-based and service oriented government oModernise governing system 7 capabilities, Establish modern fiscal system – Set up Central Leading Team for comprehensively deepening reform oAccelerate reforms in education, employment, income distribution, social security, public health – Markets’ decisive role in allocating resources oPublic ownership remains dominant; More free trade zones, relax investment restrictions – Allow people living outside cities to equally participate in modernisation oChanges to residency system – Hukou oProperty rights for farmers; New agribusiness systems – Drawing red line for ecological protection – Relax one child policy

35

Provincial, State Owned Enterprises and City debts and guarantees High, but owed to each other. Very low personal mortgage debt. Very regionalised SOE, not national as in the USA Low Central Government budget deficits and debt Very high foreign currency reserves and real assets Revamp of income tax system to reduce reliance on property transactions Overbuilding Still another 300m people are planned to shift to urban centres by 2030 Rail and road system still only a fraction of that in the USA for 4X population Wages costs showing strong growth Necessary to boost consumption, reduce savings, limit social unrest Pollution and Ecological damage Remediation and prevention are now a big focus China Risks

36

The Budget and Commission of Audit Budget Deficits need to be cut: Not so much an issue now but will be chronic in the future Income Tax and Interest Expense burden impacts Sense of Entitlement needs to be wound back Personal Industrial Business State Governments Productivity and Flexibility constraints have to be reduced Risk of becoming the white trash of Asia

37

Focus of Policy: “…the Budget we announce tonight is the first word and not the last word on Budget repair. There is much work that still needs to be done.” Cut some entitlements, including in superannuation but main impacts are years out Increase taxes on high income earners Infrastructure Spending to build prosperity Seems to be underlying concerns about robustness of the Australian economy Dodged the Productivity issue, as have most Governments Dodged the reform of the tax system

38

Focus of Policy?: “…the Budget we announce tonight is the first word and not the last word on Budget repair. There is much work that still needs to be done.” Cut some entitlements, including in superannuation but main impacts are years out Increase taxes on high income earners Infrastructure Spending to build prosperity Seems to be underlying concerns about robustness of the Australian economy Dodged the Productivity issue, as have most Governments Dodged the reform of the tax system

39

12/13f13/14e14/15f15/16f16/17f17/18f Payments -% Growth -% of GDP 25.9 +11.8 25.3 +0.4 24.8 +2.8 24.7 +4.6 24.8 +5.2 24.8 Receipts -% Growth -% of GDP +6.2 23.1 +3.5 23.0 +6.1 23.6 +6.4 24.0 +6.4 24.4 +7.1 24.9 Cash Balance (Underlying) - $ billion -% of GDP -18.8 -1.2 -49.9 -3.1 -29.8 -1.8 -17.1 -10.6 -0.6 -2.8 -0.2 Source: Australian Government 2014/15 Budget Paper No. 1 Major Financial Projections

40

Main Revenue Items Cash Basis, $b and % change 12/1313/14e14/15e15/16e16/17p17/18p Individuals156.3 +5.7% 163.8 +4.8% 178.8 +9.2% 193.6 +8.3% 208.3 +7.6 223.7 +7.4 Companies, FBT, RRTs72.7 -0.3% 73.7 +1.4% 77.9 5.8% 82.2 +5.5% 87.1 +5.9% 91.7 +5.3% Superannuation7.7 +1.6% 6.5 -14.8% 7.7 +17.6% 10.4 +35.1% 11.3 +8.7 11.8 +4.7 Excises and Customs33.6 +3.2% 34.7 +3.5% 35.6 +2.6% 36.7 +3.1% 39.1 +6.4% 41.0 +4.8% Sales Taxes49.8 +5.8% 52.2 +4.9% 55.1 +5.6% 58.4 +6.0% 61.9 6.0% 65.3 5.6% Carbon Pricing Mechanism (2013/14 Budget est) 3.6 (+4.2) 7.2 (+6.3) 1.7 (+6.4) 0 (+4.6) All Taxes326.4341.6360.4385.3411.7437.6 Source: 2010/11 Federal Budget Paper No 1 Bracket and Super Creep Getting Worse Source: Australian Government 2014/15 Budget Paper No. 1

41

Not A Sustainable Personal Tax Situation

42

Company Tax Rates and Take also High Source:OECD.org /ctp/tax-policy/revenue-statistics-tables Company Tax as % of GDP

43

Main Expense Items Accrual Basis, $b 12/1313/14e14/15e15/16e16/17p17/18p General Public Services26.034.223.222.823.423.1 Defence21.122.824.225.225.727.6 Education28.529.729.630.231.832.8 Health61.364.566.968.271.874.9 Social Security and Welfare131.9140.6145.8149.3158.4169.6 General Revenue Assistance to State and Local Governments 51.553.257.160.563.967.3 Public Debt Interest12.513.514.716.117.217.9 Other49.856.853.358.861.662.2 Total382.6415.3414.8431.1453.8475.4 Source: 2010/11 Federal Budget Paper No 1 Source: Australian Government 2014/15 Budget Paper No. 1

44

% change, inflation adjusted (Italicised are PSL forecasts) 10/1111/1212/13e13/14f14/15f15/16f Household Consumption3.13.22.02.533.25 New Motor Vehicle Sales, m* 1.0011.031.101.131.21.25 Private Investment - Dwellings 3.0-3.6-0.13.57.55.5 No. of Private Dwellings Started (‘000)* 154141156165175185 - Non Dwell. Construction8.837.613.9-2.5-9.5-12.5 - Equipment310.1-4.3-9.5-27 Private Final Demand36.22.81.251.52 Public Final Demand3.42.3-1.31.751.51 Source: Australian Government 2014/15 Budget Paper No. 1 * PSL Forecasts The Australian Economy: The Federal Government’s Forecasts

* Non Dwell. Construction Equipment Private Final Demand Public Final Demand Source: Australian Government 2014/15 Budget Paper No. 1 * PSL Forecasts The Australian Economy: The Federal Government’s Forecasts.")

45

Consumer & Business Confidence Heading in Different Directions

46

Net Worth Improving But Households Likely to stay Big Savers Source: RBA Chartpack June 2014

47

Private Investment Expected To Fall But Likely Less Dire Gross Investment by Major Industry Sector, $b, Current $ 2010/1111/1212/1313/14 5 th Est 14/15 1 st Est Mining46.982.094.7102.474.2 Manufacturing12.313.29.48.96.3 Electricity, Gas & Water6.25.4 5.95.0 Construction5.44.74.23.31.7 Wholesale & Retail Trade7.47.57.38.16.5 Transport, Post & Warehousing11.613.710.711.68.4 Rental, Hiring & Real Estate11.910.59.110.19.0 Other17.617.924.116.813.7 Total119.3154.8168.2167.1124.9 (121 – 156) Source: ABS 5625.0 Private New Capital Expenditure and Expected Expenditure, Australia, Dec 2013

Source: ABS Private New Capital Expenditure and Expected Expenditure, Australia, Dec 2013")

48

The Australian Economy: The Federal Government’s Forecasts 10/1111/1212/13 e 13/14f14/15f15/16f Employment, % change to June qtr2.20.51.20.751.5 Unemployment Rate, % June qtr4.95.255.666.25 Labour Force Participation Rate, % June qtr 65.56565.164.7564.5 Household Savings Ratio, % June qtr, trend 11.411.510.510 (PSL) 9 (PSL) 9 (PSL) Source: Australian Government 2014/15 Budget Paper No. 1

49

The Australian Economy: The Federal Government’s Forecasts % change, inflation adjusted 10/1111/1212/13e13/14f14/15f15/16f Exports0.24.765.5 7 Imports10.411.80.5-322.5 -Net Contribution to Growth -2-1.31.21.7511.25 Gross Domestic Product 2.03.42.62.752.53 Nominal GDP8.352.5434.75 Source: Australian Government 2014/15 Budget Paper No. 1

50

The Australian Economy: The Federal Government’s Forecasts 10/1111/12f12/13e13/14f14/15f15/16f Consumer Prices, % change to June qtr3.61.22.43.252.252.5 Wage Price Index, % change to June qtr3.83.72.92.7533 Terms of Trade, % change+20.6+0.4-9.8-5-6.75-1.75 Current Account Deficit -$billion -% of GDP 33.0 2.4 44.3 2.7 55.3 3.6 51.5 3.25 65 4 64 3.75 Source: Australian Government 2014/15 Budget Paper No. 1

51

RBA Forecasts for Inflation and Growth: - $A higher than earlier expected - Inflation in the 2-3% range Source: RBA Statement on Monetary Policy, May 2010 Source: RBA May 2014 Statement on Monetary Policy

52

Domestic Inflation and Wages Slowing, $A to again dampen Imported Inflation Source: RBA Chartpack June 2014

53

Markets See Cash Rates on Hold to 2016

54

Longer Term Rates likely near cycle lows

55

Australian Share Prices & Profits Australian Profits Rising but Investors stay Cautious

56

Forward Price/Earnings Ratios Up since May 2013 but Improved Earnings Outlook AustraliaLate 80s Now Dividend Yields4 - 5%4.3% Inflation7–8%2-3% 10 Year Govt Bonds12–13%4 - 4.25% Source: RBA Chart Pack June 2014

57

Summary Global Share markets should move higher in 2014 Profits growing strongly, huge cash holdings US and European companies still technological leaders New economies seeking brands and technologies Emerging market turmoil will be short term and corralled Western banks well capitalised and system liquidity is high Financial markets regulation still poor, greed has not gone away Interest rates remaining very low as Authorities err on side of caution Australian share markets should also move higher Investors still seeking income: Equities have attractions of franking credits Retiring Baby Boomers will strengthen the demand for income generating equities Cash Interest rates on hold at 2.5% but yield curve steepening Broader economy to lift through 2014/15: Housing, Private Consumption, Public investment Commodity prices should keep rising as global economy lifts $A around $US0.90 - $US0.95 Continued rapid change makes stock selection very important

58

Some Issues for South Australia Small, Regional Economy: 1.67 million people Smaller than Western Sydney or Brisbane Irrelevant nationally, Federal Focus elsewhere Population older & ageing faster, sicker, less educated – Housing, retail, tax base, attitudes, national representation No Exports, No growth Industry structure still adapting from 1960s, skills shortages High $A, More international competition Restricted public finances Low per capita income, slower population growth Large Public Sector, High Deficits & Growing Debt Likely less support from Federal Govt Don’t criticise the Government

59

Where we are headed

60

Metropolitan Home Prices Flat, Activity Up Auction clearance rates March 2014 63% Jan-Feb 2014 51% March 2013 55% Jan- Feb 2013 58% For 2014 Employment flat, population to grow Interest Rates on hold to higher Vacancy rates should steady High land costs continue Funding constraints to ease further Dominance of the big banks impacting competition First Home Buyer Affordability and overall confidence are the big issues

61

Building Activity Starting to Recover

62

Food Turnover

63

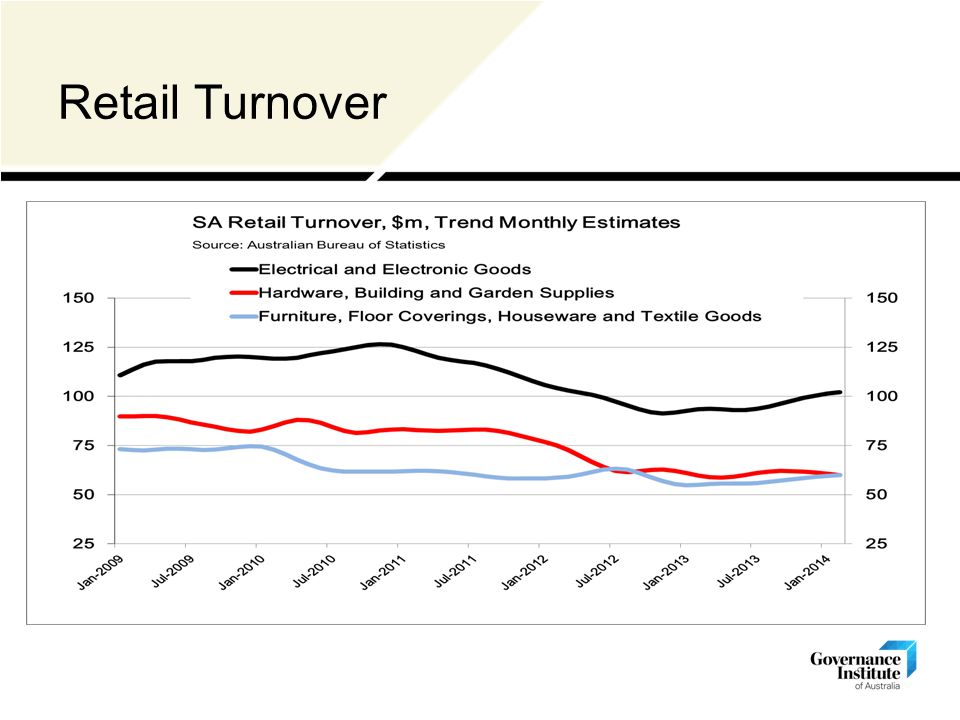

Retail Turnover

67

SA New Motor Vehicle Sales

68

Business Confidence Down post elections Sensis Small and Medium Business Index, March qtr 2014

69

But Individual Expectations in SA Improving? Sensis Small and Medium Business Index, March qtr 2014

70

Economic Forecasts: South Australia

71

South Australian Growth: Where? Gross Value Added, ABS Cat 5220.0

72

Business, Credit and Governance Issues Asian Middle Class Urbanisation offers opportunities of a scale not seen before – Quantitatively and Qualitatively – Issues of Skills, Infrastructure, Regulation, Costs Ageing issues Accelerating change means Demand and Revenue trends across sectors and businesses will remain very mixed Tax and Public sector charges high in SA for the foreseeable future Public sector “restraint” not enough to sufficiently reduce high deficits SA ALP Government support for small business is shrinking – Needs change of focus – Increased support and/or reduced costs for local and small business – Recognise State’s role in export infrastructure The Liberals are not a small G government party Federal/State relationship changes will likely be adverse Poor Productivity performance is a big challenge

73

Multifactor Productivity Growth Selected Countries and Regions, Average annual growth rates, % Sources: The Conference Board Total Economy Database TM Peter Harris, Chairman of the Productivity Commission, Speech to the May 2014 Conference of the Stock Brokers Association of Australia, Melbourne, Australia

74

Likely facing Slower Growth in Living Standards Source: Australian Government 2014/15 Budget Paper No. 1

75

The changing world at a faster paces offers many and big opportunities for adaptive businesses: – Industries are Changing, Emerging, Disappearing – Big established names being challenged and destroyed – Labour and Government driven costs/regulatory load need to be worked around – Staff shortages, Turnover and Expectations are all increasing – Be prepared to have various working relationships – Being adaptable is likely to be more important than having a detailed plan – Getting the Productivity challenge right will be a big advantage Business, Credit and Governance Issues

76

Keep up with Prescott Securities at www.prescottsecurities.com.au @PrescottSec @DarrylGobbett @AndrewSterzl @TravisAdamsCFA http://www.youtube.com/PrescottSecurities

77

Prescott Securities Limited 245 Fullarton Road Eastwood SA 5063 prescottsecurities.com.au Thank You

78

© Governance Institute of Australia

Similar presentations