Download presentation

Presentation is loading. Please wait.

1

Dates for term tests Friday, February 07 Friday, March 07

2

The Moving Average Time series of order q, MA(q)

Let {xt|t T} be defined by the equation. where {ut|t T} denote a white noise time series with variance s2. Then {xt|t T} is called a Moving Average time series of order q. (denoted by MA(q))

)")

3

The mean value for an MA(q) time series

The autocovariance function for an MA(q) time series The autocorrelation function for an MA(q) time series

time series. The autocorrelation function for an MA(q) time series.")

4

Comment The autocorrelation function for an MA(q) time series “cuts off” to zero after lag q. q

time series cuts off to zero after lag q. q")

5

The Autoregressive Time series of order p, AR(p)

Let {xt|t T} be defined by the equation. where {ut|t T} is a white noise time series with variance s2. Then {xt|t T} is called a Autoregressive time series of order p. (denoted by AR(p))

)")

6

The mean value of a stationary AR(p) series

The Autocovariance function s(h) of a stationary AR(p) series Satisfies the equations:

of a stationary AR(p) series. Satisfies the equations:")

7

Satisfies the equations:

The Autocorrelation function r(h) of a stationary AR(p) series Satisfies the equations: with for h > p and

of a stationary AR(p) series. Satisfies the equations: with. for h > p. and.")

8

or: where r1, r2, … , rp are the roots of the polynomial and c1, c2, … , cp are determined by using the starting values of the sequence r(h).

.")

9

Conditions for stationarity

Autoregressive Time series of order p, AR(p)

")

10

For a AR(p) time series, consider the polynomial

with roots r1, r2 , … , rp then {xt|t T} is stationary if |ri| > 1 for all i. If |ri| < 1 for at least one i then {xt|t T} exhibits deterministic behaviour. If |ri| ≥ 1 and |ri| = 1 for at least one i then {xt|t T} exhibits non-stationary random behaviour.

11

since: and |r1 |>1, |r2 |>1, … , | rp | > 1 for a stationary AR(p) series then i.e. the autocorrelation function, r(h), of a stationary AR(p) series “tails off” to zero.

, of a stationary AR(p) series tails off to zero.")

12

Special Cases: The AR(1) time

Let {xt|t T} be defined by the equation.

13

Consider the polynomial

with root r1= 1/b1 {xt|t T} is stationary if |r1| > 1 or |b1| < 1 . If |ri| < 1 or |b1| > 1 then {xt|t T} exhibits deterministic behaviour. If |ri| = 1 or |b1| = 1 then {xt|t T} exhibits non-stationary random behaviour.

14

Special Cases: The AR(2) time

Let {xt|t T} be defined by the equation.

15

Consider the polynomial

where r1 and r2 are the roots of b(x) {xt|t T} is stationary if |r1| > 1 and |r2| > 1 . This is true if b1+b2 < 1 , b2 –b1 < 1 and b2 > -1. These inequalities define a triangular region for b1 and b2. If |ri| < 1 or |b1| > 1 then {xt|t T} exhibits deterministic behaviour. If |ri| ≤ 1 for i = 1,2 and |ri| = 1 for at least on i then {xt|t T} exhibits non-stationary random behaviour.

{xt|t T} is stationary if |r1| > 1 and |r2| > 1 . This is true if b1+b2 < 1 , b2 –b1 < 1 and b2 > -1. These inequalities define a triangular region for b1 and b2. If |ri| < 1 or |b1| > 1 then {xt|t T} exhibits deterministic behaviour. If |ri| ≤ 1 for i = 1,2 and |ri| = 1 for at least on i then {xt|t T} exhibits non-stationary random behaviour.")

16

Patterns of the ACF and PACF of AR(2) Time Series

In the shaded region the roots of the AR operator are complex b2

17

The Mixed Autoregressive Moving Average

Time Series of order p,q The ARMA(p,q) series

series.")

18

The Mixed Autoregressive Moving Average Time Series of order p, ARMA(p,q)

Let b1, b2, … bp , a1, a2, … ap , d denote p + q +1 numbers (parameters). Let {ut|t T} denote a white noise time series with variance s2. independent mean 0, variance s2. Let {xt|t T} be defined by the equation. Then {xt|t T} is called a Mixed Autoregressive- Moving Average time series - ARMA(p,q) series.

. Let {ut|t T} denote a white noise time series with variance s2. independent. mean 0, variance s2. Let {xt|t T} be defined by the equation. Then {xt|t T} is called a Mixed Autoregressive- Moving Average time series - ARMA(p,q) series.")

19

Mean value, variance, autocovariance function, autocorrelation function of an ARMA(p,q) series

series")

20

Similar to an AR(p) time series, for certain values of the parameters b1, …, bp an ARMA(p,q) time series may not be stationary. An ARMA(p,q) time series is stationary if the roots (r1, r2, … , rp ) of the polynomial b(x) = 1 – b1x – b2x2 - … - bp xp satisfy | ri| > 1 for all i.

time series is stationary if the roots (r1, r2, … , rp ) of the polynomial. b(x) = 1 – b1x – b2x2 - … - bp xp. satisfy | ri| > 1 for all i.")

21

Assume that the ARMA(p,q) time series {xt|t T} is stationary:

Let m = E(xt). Then or

. Then. or.")

22

The Autocovariance function, s(h), of a stationary mixed autoregressive-moving average time series

{xt|t T} be determined by the equation: Thus

23

Hence

25

We need to calculate:

27

h sux(h) -1 -2 -3

")

28

The autocovariance function s(h) satisfies:

For h = 0, 1. … , q: for h > q:

29

We then use the first (p + 1) equations to determine:

s(0), s(1), s(2), … , s(p) We use the subsequent equations to determine: s(h) for h > p.

, s(1), s(2), … , s(p) We use the subsequent equations to determine: s(h) for h > p.")

30

Example:The autocovariance function, s(h), for an ARMA(1,1) time series:

For h = 0, 1: or for h > 1:

31

Substituting s(0) into the second equation we get:

or Substituting s(1) into the first equation we get:

into the first equation we get:")

32

for h > 1:

33

The Backshift Operator B

34

Consider the time series {xt : t T} and Let M denote the linear space spanned by the set of random variables {xt : t T} (i.e. all linear combinations of elements of {xt : t T} and their limits in mean square). M is a vector space Let B be an operator on M defined by: Bxt = xt-1. B is called the backshift operator.

. M is a vector space. Let B be an operator on M defined by: Bxt = xt-1. B is called the backshift operator.")

35

Note: We can also define the operator Bk with

Bkxt = B(B(...Bxt)) = xt-k. The polynomial operator p(B) = c0I + c1B + c2B ckBk can also be defined by the equation. p(B)xt = (c0I + c1B + c2B ckBk)xt . = c0Ixt + c1Bxt + c2B2xt ckBkxt = c0xt + c1xt-1 + c2xt ckxt-k

) = xt-k. The polynomial operator. p(B) = c0I + c1B + c2B ckBk. can also be defined by the equation. p(B)xt = (c0I + c1B + c2B ckBk)xt . = c0Ixt + c1Bxt + c2B2xt ckBkxt. = c0xt + c1xt-1 + c2xt ckxt-k.")

36

The power series operator p(B) = c0I + c1B + c2B2 + ...

can also be defined by the equation. p(B)xt = (c0I + c1B + c2B )xt = c0Ixt + c1Bxt + c2B2xt + ... = c0xt + c1xt-1 + c2xt If p(B) = c0I + c1B + c2B and q(B) = b0I + b1B + b2B are such that p(B)q(B) = I i.e. p(B)q(B)xt = Ixt = xt than q(B) is denoted by [p(B)]-1.

xt = (c0I + c1B + c2B )xt. = c0Ixt + c1Bxt + c2B2xt = c0xt + c1xt-1 + c2xt If p(B) = c0I + c1B + c2B and q(B) = b0I + b1B + b2B are such that. p(B)q(B) = I. i.e. p(B)q(B)xt = Ixt = xt. than q(B) is denoted by [p(B)]-1.")

37

Other operators closely related to B:

F = B-1 ,the forward shift operator, defined by Fxt = B-1xt = xt+1 and D = I - B ,the first difference operator, defined by Dxt = (I - B)xt = xt - xt-1 .

xt = xt - xt-1 .")

38

The Equation for a MA(q) time series

xt= a0ut + a1ut-1 +a2ut aqut-q + m can be written xt= a(B) ut + m where a(B) = a0I + a1B +a2B aqBq

ut + m. where. a(B) = a0I + a1B +a2B aqBq.")

39

The Equation for a AR(p) time series

xt= b1xt-1 +b2xt bpxt-p + d + ut can be written b(B) xt= d + ut where b(B) = I - b1B - b2B bpBp

xt= d + ut. where. b(B) = I - b1B - b2B bpBp.")

40

The Equation for a ARMA(p,q) time series

xt= b1xt-1 +b2xt bpxt-p + d + ut + a1ut-1 +a2ut aqut-q can be written b(B) xt= a(B) ut + d where a(B) = a0I + a1B +a2B aqBq and b(B) = I - b1B - b2B bpBp

xt= a(B) ut + d. where. a(B) = a0I + a1B +a2B aqBq. and. b(B) = I - b1B - b2B bpBp.")

41

Some comments about the Backshift operator B

It is a useful notational device, allowing us to write the equations for MA(q), AR(p) and ARMA(p, q) in a very compact form; It is also useful for making certain computations related to the time series described above;

, AR(p) and ARMA(p, q) in a very compact form; It is also useful for making certain computations related to the time series described above;")

42

The partial autocorrelation function

A useful tool in time series analysis

43

The partial autocorrelation function

Recall that the autocorrelation function of an AR(p) process satisfies the equation: rx(h) = b1rx(h-1) + b2rx(h-2) bprx(h-p) For 1 ≤ h ≤ p these equations (Yule-Walker) become: rx(1) = b1 + b2rx(1) bprx(p-1) rx(2) = b1rx(1) + b bprx(p-2) ... rx(p) = b1rx(p-1)+ b2rx(p-2) bp.

process satisfies the equation: rx(h) = b1rx(h-1) + b2rx(h-2) bprx(h-p) For 1 ≤ h ≤ p these equations (Yule-Walker) become: rx(1) = b1 + b2rx(1) bprx(p-1) rx(2) = b1rx(1) + b bprx(p-2) ... rx(p) = b1rx(p-1)+ b2rx(p-2) bp.")

44

In matrix notation: These equations can be used to find b1, b2, … , bp, if the time series is known to be AR(p) and the autocorrelation rx(h)function is known.

and the autocorrelation rx(h)function is known.")

45

If the time series is not autoregressive the equations can still be used to solve for b1, b2, … , bp, for any value of p ≥ 1. In this case are the values that minimizes the mean square error:

46

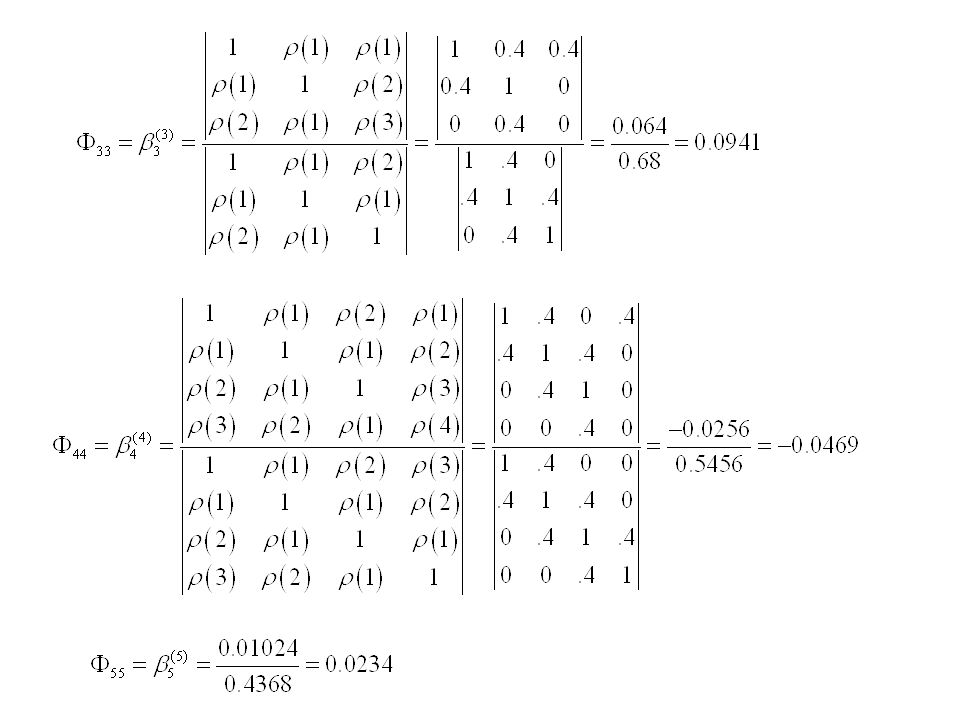

Definition: The partial auto correlation function at lag k is defined to be:

Using Cramer’s Rule

47

Comment: The partial auto correlation function, Fkk is determined from the auto correlation function, r(h) The partial auto correlation function at lag k, Fkk is the last auto-regressive parameter, if the series was assumed to be an AR(k) series. If the series is an AR(p) series then An AR(p) series is also an AR(k) series with k > p with the auto regressive parameters zero after p.

series. If the series is an AR(p) series then. An AR(p) series is also an AR(k) series with k > p with the auto regressive parameters zero after p.")

48

Some more comments: The partial autocorrelation function at lag k, Fkk, can be interpreted as a corrected autocorrelation between xt and xt-k conditioning on the intervening variables xt-1, xt-2, ... ,xt-k+1 . If the time series is an AR(p) time series than Fkk = 0 for k > p If the time series is an MA(q) time series than rx(h) = 0 for h > q

time series than. Fkk = 0 for k > p. If the time series is an MA(q) time series than. rx(h) = 0 for h > q.")

49

A General Recursive Formula for Autoregressive Parameters and the Partial Autocorrelation function (PACF)

")

50

Let denote the autoregressive parameters of order k satisfying the Yule Walker equations:

51

Then it can be shown that:

and

52

Proof: The Yule Walker equations:

53

In matrix form:

54

The equations for

55

and The matrix A reverses order

56

The equations may be written

Multiplying the first equations by or

57

Substituting this into the second equation

or and

58

Hence and or

59

Some Examples

60

Example 1: MA(1) time series

Suppose that {xt|t T} satisfies the following equation: xt = ut ut – 1 where {ut|t T} is white noise with s = 1.1. Find: The mean of the series, The variance of the series, The autocorrelation function. The partial autocorrelation function.

61

Solution Now {xt|t T} satisfies the following equation:

xt = ut ut – 1 Thus: The mean of the series, m = 12.0 The autocovariance function for an MA(1) is

is.")

62

Thus: The variance of the series, s(0) = and The autocorrelation function is:

= and The autocorrelation function is:")

63

The partial auto correlation function at lag k is defined to be:

Thus

65

Graph: Partial Autocorrelation function Fkk

66

Exercise: Use the recursive method to calculate Fkk

and

67

Exercise: Use the recursive method to calculate Fkk

and

68

Example 2: AR(2) time series

Suppose that {xt|t T} satisfies the following equation: xt = 0.4 xt – xt – ut where {ut|t T} is white noise with s = 2.1. Is the time series stationary? Find: The mean of the series, The variance of the series, The autocorrelation function. The partial autocorrelation function.

69

The mean of the series The autocorrelation function. Satisfies the Yule Walker equations

70

hence

71

the variance of the series

The partial autocorrelation function.

72

The partial autocorrelation function of an AR(p) time series “cuts off” after p.

time series cuts off after p.")

73

Example 3: ARMA(1, 2) time series

Suppose that {xt|t T} satisfies the following equation: xt = 0.4 xt – ut ut – ut – 2 where {ut|t T} is white noise with s = 1.6. Is the time series stationary? Find: The mean of the series, The variance of the series, The autocorrelation function. The partial autocorrelation function.

74

xt = 0.4 xt – ut ut – ut – 1 white noise std. dev,. s = 1.6. Is the time series stationary? b(x) = 1 – b1x = 1 – 0.4x has root r1 =1/0.4 =2.5 Since |r1| > 1, the time series is stationary Find: The mean of the series.

= 1 – b1x = 1 – 0.4x has root r1 =1/0.4 =2.5. Since |r1| > 1, the time series is stationary. Find: The mean of the series.")

75

The autocovariance function s(h) satisfies:

For h = 0, 1, 2 for h > q: i.e. For h = 0, 1, 2 for h > q:

76

etc. where

77

We use the first two equations to find s0 and s1

Then we use the third equation to find s2

78

The autocovariance, autocorrelation functions

79

Spectral Theory for a stationary time series

Similar presentations

models>")

,CE Instructor Dr. L. D. Behera Department of Electrical Engineering Indian institute.>")

We already know about the sample autocorrelation function (SAC): Properties: Not unbiased (since a ratio between two.>")

Material.>")