Download presentation

Presentation is loading. Please wait.

1

A strategy to leave more to your heirs at death

Annuity Maximization Today we’re talking about North American’s newest product, the Custom TermGUL

2

Disclosures These disclosures apply to this presentation in its entirety

Custom GrowthCV is issued on policy form series LS166; Custom Guarantee is issued on policy form series LS163A, Premium Guarantee Rider is issued on form series LR452; Accelerated Benefit Endorsement is issued on form series LR352A, Chronic Illness Accelerated Benefit Rider (In Minnesota, Accelerated Benefit Rider for Continuous Confinement) is issued on form series LR450A, or state variation by North American Company for Life and Health Insurance, Executive Office: Chicago, IL Products, features or riders, endorsements or issues ages may not be available in all jurisdictions. Limitations or restrictions may apply. If the policyowner terminates the No Lapse Guarantee period, significantly higher premiums may be necessary to keep the policy in force. Paying a premium that is equal to, but not greater than, the No Lapse Guarantee Premium will keep the policy in force during the No Lapse Guarantee Period but may result in a negative or zero policy fund. By paying only the premium required to satisfy the no-lapse guarantee, the policyowner may be forgoing the advantage of building significant cash value. North American nor its agent give legal or tax advice. Please advise your customers to consult with and rely on a qualified legal or tax advisor before entering into or paying additional premiums with respect to such arrangements. In some situations loans and withdrawals may be subject to federal taxes. North American does not give tax or legal advice. Clients should be instructed to consult with and rely on their own tax advisor or attorney for advice on their specific situation. Snapshots from Illustrations are for example purposes only and do not represent the full Illustrations.

is issued on form series LR450A, or state variation by North American Company for Life and Health Insurance, Executive Office: Chicago, IL Products, features or riders, endorsements or issues ages may not be available in all jurisdictions. Limitations or restrictions may apply. If the policyowner terminates the No Lapse Guarantee period, significantly higher premiums may be necessary to keep the policy in force. Paying a premium that is equal to, but not greater than, the No Lapse Guarantee Premium will keep the policy in force during the No Lapse Guarantee Period but may result in a negative or zero policy fund. By paying only the premium required to satisfy the no-lapse guarantee, the policyowner may be forgoing the advantage of building significant cash value. North American nor its agent give legal or tax advice. Please advise your customers to consult with and rely on a qualified legal or tax advisor before entering into or paying additional premiums with respect to such arrangements. In some situations loans and withdrawals may be subject to federal taxes. North American does not give tax or legal advice. Clients should be instructed to consult with and rely on their own tax advisor or attorney for advice on their specific situation. Snapshots from Illustrations are for example purposes only and do not represent the full Illustrations.")

3

Scenario Many clients don’t plan to spend down all their assets

Leaving money to heirs is a common goal A great deal of assets are currently held in annuities

4

Annuities at death Subject to income taxes Subject to estate taxes

Diminished amount passed to client’s heirs

5

Considerations Annuity Income & Estate Taxable at death

RMDs at 70 ½ for qualified funds Life Insurance Income Tax free at death* ILIT or outside ownership avoids estate tax No RMDs

6

Annuity Maximization Leverage assets currently in an annuity policy into a greater benefit for heirs at death using life insurance. Deferred annuities are not recommended for wealth transfer while life insurance is designed to be an effective wealth transfer vehicle.

7

Some Considerations Taxes Moving Funds

Irrevocable Life Insurance Trust (ILIT) Client objective

Client objective.")

8

Taxes Income Tax (Federal and State) Estate Tax (Federal and State)

Client may have personal opinion as to the future of income and estate tax rates To make a technically robust example, I think you’ll lead your audience away from your main point. Here’s how I’d suggest presenting it to your audience: Say you have a decedent who owned a $1 million deferred annuity at death. The decedent’s estate is in the 45% estate tax bracket, and the 28% income tax bracket. Let’s ignore other moving parts—such as state death taxes, special estate expenses and other estate tax nuances to keep the example simple. The decedent had a $500,000 basis in the annuity, so there’s $500,000 of gain inherent in it. Let’s also say that one of the decedent’s kids is the sole beneficiary of the annuity, and he plans to cash it out right away. The rules say that the estate tax is calculated first. On a $1 million annuity, the marginal estate tax in a taxable estate is $450,000, based on current rules. $225,000 of that tax is allocated to the basis part of the annuity, and the other $225,000 is allocated to the income part—the IRD part. (Tom, this is different from the way I described it to you on the phone.) When the beneficiary cashes out of the annuity, his gross taxable income would be calculated by taking the $1 million value, and subtracting the decedent’s $500,000 basis. That leaves a gross gain of $500,000. The taxable gain is calculated by taking the gross gain of $500,000, and subtracting the estate tax attributable to that gain. We calculated that earlier to be $225,000. So the calculation is $500,000 of gross gain minus the $225,000 estate tax deduction, leaving $275,000 income taxable. At a 28% tax rate, that means $77,000 in income tax.

When the beneficiary cashes out of the annuity, his gross taxable income would be calculated by taking the $1 million value, and subtracting the decedent’s $500,000 basis. That leaves a gross gain of $500,000. The taxable gain is calculated by taking the gross gain of $500,000, and subtracting the estate tax attributable to that gain. We calculated that earlier to be $225,000. So the calculation is $500,000 of gross gain minus the $225,000 estate tax deduction, leaving $275,000 income taxable. At a 28% tax rate, that means $77,000 in income tax.")

9

Moving funds Lump sum Free withdrawals Annuitize Implications:

Lifetime Short Implications: Taxes, Surrender Charges, Insurance performance Lump sum may be of interest if the client wants maximum amount to the life policy as soon as possible which may purchase a larger amount of coverage. The client may also want to capitalize on the current income tax and/or gift tax rate. The withdrawal approach may be beneficial because it allows the annuity holder to maintain control of the asset in case of an emergency. However they have given up the guarantee of an income stream for that control. Annuitization is a common approach using either a lifetime income stream or a short time-frame. Lifetime may sometimes purchase more coverage and would be most likely to be within annual gifting limits. A short timeframe could be advantageous if the goal is to complete the move quickly and the life policy can take advantage of quicker premium funding.

10

Irrevocable Life Insurance Trust (ILIT)?

Estate Tax Planning Control Funding Annual gift exemption ($13,000 in 2009) Lifetime gift credit OR could own by children/grandchildren

Lifetime gift credit. OR could own by children/grandchildren.")

11

Two types of clients Death benefit objective to estate building

Estate Taxable Non-estate taxable Access to cash value a primary goal

12

Client Type 1 – Death Benefit Objective Estate Taxable

Irrevocable Life Insurance Trust (ILIT) Gifting limit Lifetime exclusion Custom Guarantee Maximizing guaranteed death benefit to heirs

Gifting limit. Lifetime exclusion. Custom Guarantee. Maximizing guaranteed death benefit to heirs.")

13

Case Study Mr. Big Estate

$250,000 annuity ($125,00 basis) Significant estate size Top tax bracket No need of funds Goal: Maximize estate size for heirs

Significant estate size. Top tax bracket. No need of funds. Goal: Maximize estate size for heirs.")

14

Case Study Mr. Big Estate

Policy owned by ILIT Funding options (net after 30% combined fed & state tax) Lifetime SPIA: $16,111/yr 10-pay SPIA: $24,931/yr Lump sum: $212,500 Guaranteed death benefit purchased: Lifetime SPIA = $654,151 10-pay SPIA = $572,743 Lump Sum = $637,473 Looked at many funding options including Single pay, 10 pay, and lifetime SPIA. For this client, lifetime SPIA resulted in best solution. Age 65 Male, Standard rate class, Guaranteed DB to age 100

Lifetime SPIA: $16,111/yr. 10-pay SPIA: $24,931/yr. Lump sum: $212,500. Guaranteed death benefit purchased: Lifetime SPIA = $654, pay SPIA = $572,743. Lump Sum = $637,473. Looked at many funding options including Single pay, 10 pay, and lifetime SPIA. For this client, lifetime SPIA resulted in best solution. Age 65 Male, Standard rate class, Guaranteed DB to age 100.")

15

Case Study Mr. Big Estate

Selected Solution is Lifetime SPIA $16,111/yr after taxes $13,000/yr used of annual gift exemption Balance of $3,111/yr lifetime gift exclusion Future gifting limits indexed for inflation Death Benefit of $654,151 Looked at many funding options including Single pay, 10 pay, and lifetime SPIA. For this client, lifetime SPIA resulted in best solution. Age 65 Male, Standard rate class, Guaranteed DB to age 100

16

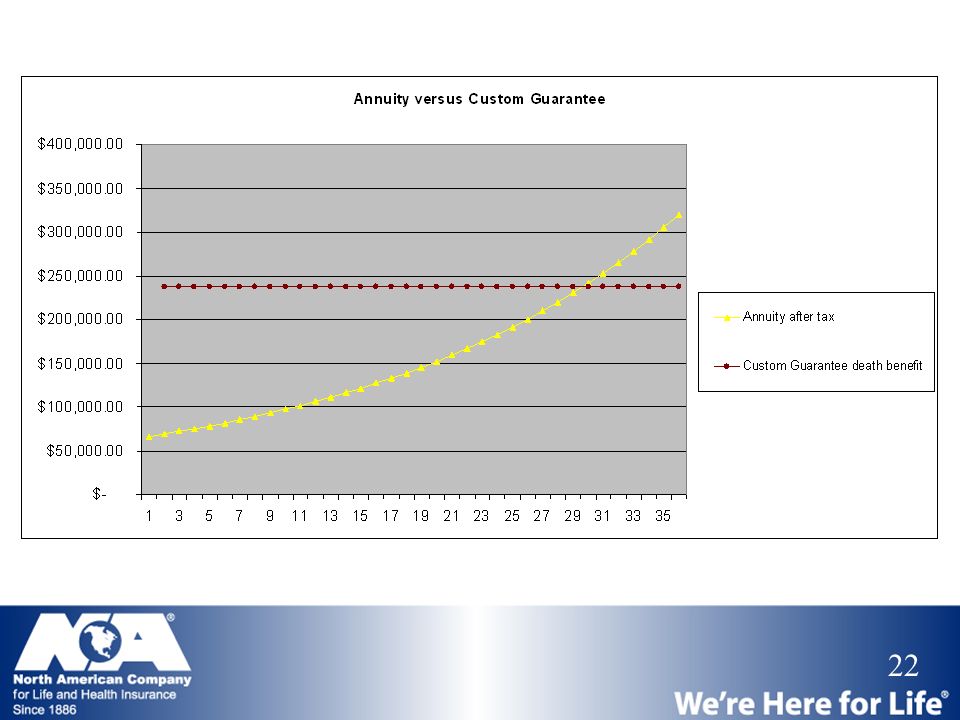

Maximum guaranteed coverage

The illustration really says it all. We’ve turned a taxable $250,000 annuity into a tax free death benefit of over $650,000. The death benefit is guaranteed to age 100. Partial illustration shown. Age 65 Male, Standard rate class, Guaranteed DB to age 100 The information presented is hypothetical and not intended to project investment results. Illustration is not complete unless all pages are included.

17

Our 65 year old male would have to live to age 100 to match what the Custom Guarantee can deliver to his heirs immediately. Use Insmark to show how competitive the return of this death benefit is. The 20 year IRR on this example is 6.35% INCOME TAX FREE! Assumes income tax rate of 30% and estate tax rate of 45%. Annuity rate 5%

18

Client Type 1 – Death Benefit Objective No Estate Taxes

Individually owned Custom Guarantee Maximizing guaranteed death benefit to heirs

19

Case Study Mrs. Next Door

$75,000 annuity ($40,000 basis) No expected estate taxes No need for funds Goal: Maximize benefit for heirs

No expected estate taxes. No need for funds. Goal: Maximize benefit for heirs.")

20

Case Study Mrs. Next Door

Policy owned individually Funding options (net after 25% combined fed & state tax) Lifetime SPIA: $4,730/yr 5-pay SPIA: $14,025/yr Lump sum: $66,250 Guaranteed death benefit purchased: Lifetime SPIA = $237,513 5-pay SPIA = $219,140 Lump Sum = $232,382 Looked at many funding options including Single pay, 10 pay, and lifetime SPIA. For this client, lifetime SPIA resulted in best solution. Age 65 Male, Standard rate class, Guaranteed DB to age 100

Lifetime SPIA: $4,730/yr. 5-pay SPIA: $14,025/yr. Lump sum: $66,250. Guaranteed death benefit purchased: Lifetime SPIA = $237, pay SPIA = $219,140. Lump Sum = $232,382. Looked at many funding options including Single pay, 10 pay, and lifetime SPIA. For this client, lifetime SPIA resulted in best solution. Age 65 Male, Standard rate class, Guaranteed DB to age 100.")

21

Maximum guaranteed coverage

The information presented is hypothetical and not intended to project investment results. Illustration is not complete unless all pages are included.

23

Custom Guarantee Advantages

Competitive price guarantee up to 100 20% table ratings Strong in a variety of funding methods Extra effective age 60+ Life policy can be funded directly from SPIA

24

Client #2 – Access to cash value goal

Desire cash value Access to value Growth in value Death benefit for heirs Custom GrowthCV Waiver of surrender charge rider for early cash value Interest rate and premium bonuses for cash value growth

25

Case Study Mrs. Next Door

$75,000 annuity ($40,000 basis) Money not needed now, but retained access desired No expected estate taxes Goal: Leave as much to children as possible, but maintain control for unexpected needs.

Money not needed now, but retained access desired. No expected estate taxes. Goal: Leave as much to children as possible, but maintain control for unexpected needs.")

26

Case Study Mrs. Next Door

Individually owned Seeking access to cash value Avoid lump sum causing Modified Endowment Contract Quickly fund to provide fast access to cash 5-pay annuitization $14,025/yr after tax (25% tax rate) $171,493 death benefit (minimum non-MEC) Looked at many funding options including Single pay, 10 pay, and lifetime SPIA. For this client, lifetime SPIA resulted in best solution. Age 65 Female, Standard rate class, Solve for $75,000 at age 100

$171,493 death benefit (minimum non-MEC) Looked at many funding options including Single pay, 10 pay, and lifetime SPIA. For this client, lifetime SPIA resulted in best solution. Age 65 Female, Standard rate class, Solve for $75,000 at age 100.")

27

Waiver of surrender charge with table shaving

Chronic Illness Accelerated Benefit Rider Early cash value Interest rate & premium bonuses Cash value growth The illustration really says it all. We’ve turned a taxable $250,000 annuity into a tax free death benefit of over $650,000. The death benefit is guaranteed to age 100. Potentially growing death benefit Partial illustration shown. Age 65 Female, Standard rate class, Minimum face amount to meet 7pay test The information presented is hypothetical and not intended to project investment results. Illustration is not complete unless all pages are included.

28

What I did here was solving for minimum DB to avoid MEC status using the CVAT version. The cash value is projected to grow at such a rate that death benefit reaches the corridor and grows accordingly. Look how nicely that matches our assumed annuity returns!

29

Custom GrowthCV Advantages

Leverage assets with death benefit Use Cash Value Accumulation Test to get quicker rising death benefit with cash value Waiver of Surrender charge rider with table Shaving Designed for cash value Interest Rate bonus Premium bonus Chronic Illness Accelerated Benefit Rider Life policy can be funded directly from SPIA

30

North American Provides:

TWO competitive solutions for Annuity Maximization

31

North American: More sales opportunities

Custom Guarantee For the death benefit objective Annuity Maximizer High death benefit coverage guaranteed up to age 120 Custom GrowthCV For the cash value objective Annuity Maximizer Waiver of surrender charge rider for quicker access to cash value and table shaving

32

Sales Support 800-800-3656, ext. 10411 salessupport@nacolah.com

If you have additional questions, please call Sales Support at …

Similar presentations

For Broker/Dealer use only – Not for use with the public. Retirement readiness with the 3-7-5 strategy Re-Engineering Retirement SM.>")