Download presentation

Presentation is loading. Please wait.

2

LOGO 2010 to 2011

4

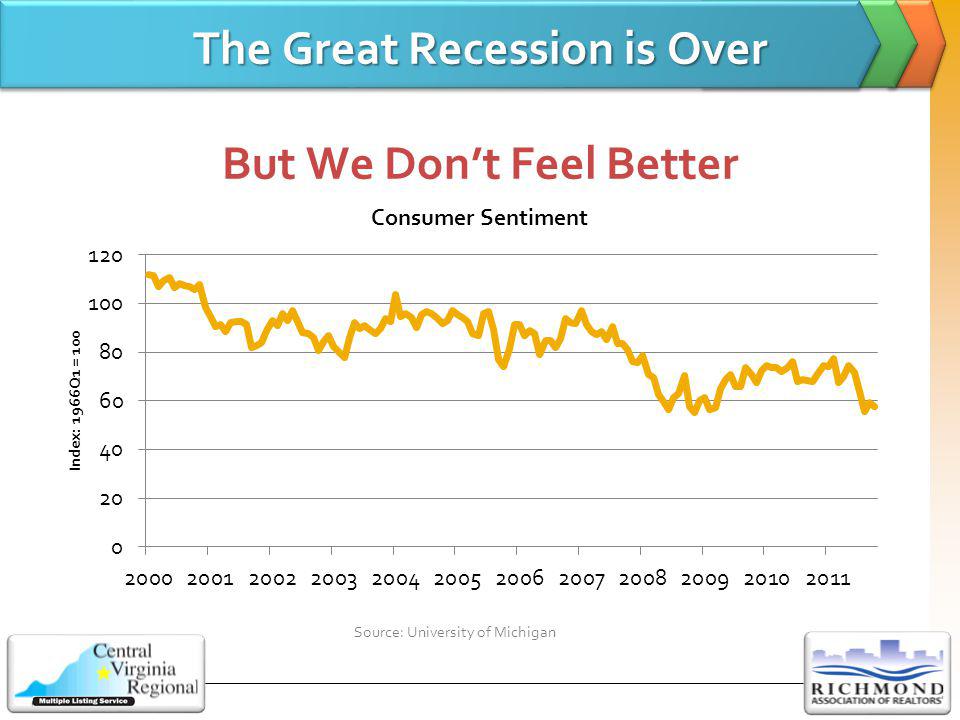

The Great Recession is Over The Great Recession is Over But We Dont Feel Better Source: University of Michigan

5

Why Dont we Feel Better? Why Dont we Feel Better? 14 million Unemployed Source: Bureau of Labor Statistics

6

Distressed Property Sales Still High Source: NATIONAL ASSOCIATION OF REALTORS ®

7

Price Declines Typical Across the State Source: Virginia Association of REALTORS ®

8

YearUnits SoldAvg List Price Avg Sold Price 2004:18,944$208,186$206,720 2005:20,043$241,420$240,041 2006:18,543$268,591$265,809 2007:15,794$280,034$274,776 2008:11,005$277,171$268,008 2009: 11,316 $268,806 $232,830 2010:10,750$245,388$228,056 2011 (YTD – September 30, 2011): 8,371$244,638$218,119 Central Virginia Regional MLS Central Virginia Regional MLS Single Family Residential Market

: 8,371$244,638$218,119 Central Virginia Regional MLS Central Virginia Regional MLS Single Family Residential Market")

9

A Metro Richmond Comparison A Metro Richmond Comparison Single Family Residential Market - 2011 AreaUnits SoldAvg LP Avg SP (%Chng) Chesterfield2,518$244,619$227,404 (-5.31%) Hanover: 665$291,098$256,129 (-4.50%) Henrico:1,978$245,735$231,412 ( -8.63%) Richmond:1,396$203,144$202,066 (-0.83%) 2011 Year-to-Date: September 30, 2011 (%Chng) compared to same period 2010 Data Collected October 20, 2011

Chesterfield2,518$244,619$227,404 (-5.31%) Hanover: 665$291,098$256,129 (-4.50%) Henrico:1,978$245,735$231,412 ( -8.63%) Richmond:1,396$203,144$202,066 (-0.83%) 2011 Year-to-Date: September 30, 2011 (%Chng) compared to same period 2010 Data Collected October 20, 2011")

10

Whats Selling… Whats Selling… …in 2011? Area ( % Sold under): $200,000$300,000$400,000 Chesterfield52.78%78.16%90.59% Hanover: 36.98%71.11%91.32% Henrico:55.46%77.40%87.56% Richmond:62.89%80.23%88.19% CVR MLS Region:57.45%79.69%89.91% Cumulative 2011 Year-to-Date: September 30, 2011 Data Collected October 20, 2011

: $200,000$300,000$400,000 Chesterfield52.78%78.16%90.59% Hanover: 36.98%71.11%91.32% Henrico:55.46%77.40%87.56% Richmond:62.89%80.23%88.19% CVR MLS Region:57.45%79.69%89.91% Cumulative 2011 Year-to-Date: September 30, 2011 Data Collected October 20,")

11

Residential Condominium Market Changes: 2010-2011 - YTD CVR MLS Region: Sold Units YTD: +4.36%Avg Sold Price YTD: +4.00% Chesterfield: Sold Units YTD: +8.37%Avg Sold Price YTD: -13.74% Henrico: Sold Units YTD: +5.47%Avg Sold Price YTD: -0.50% Richmond City: Sold Units YTD: -12.75%Avg Sold Price YTD: -3.86% Hanover: (Limited # units) Sold Units YTD: +80%(30 units to 54 units) Avg Sold Price YTD: +0.71% 2011 Year-to-Date: September 30, 2011 (%Chng) compared to same period 2010 Data Collected October 21, 2011

Sold Units YTD: +80%(30 units to 54 units) Avg Sold Price YTD: +0.71% 2011 Year-to-Date: September 30, 2011 (%Chng) compared to same period 2010 Data Collected October 21, 2011")

12

County of Chesterfield – City of Richmond October 2010 through September 2011 R E Stats Inc. - *Active Inventory as of October 25, 2011 Inventory and Absorption Single-Family Residential Data Collected October 25, 2011

13

County of Henrico – County of Hanover October 2010 through September 2011 R E Stats Inc. - *Active Inventory as of October 25, 2011 Inventory and Absorption Single-Family Residential Data Collected October 25, 2011

14

2010-2011: YTD 2010-2011: YTD The Direction Were Heading 1 st Quarter2 nd Quarter3 rd Quarter Pending Units -5.122%+0.971%+2.30% Sold Units+11.789%-4.358%+3.40% Average Sold Price-8.33%-5.13%-4.80% CVR MLS Region – Single Family 2011 Year-to-Date: September 30, 2011 (%Chng) compared to same period 2010 Thru

compared to same period 2010 Thru")

15

Economic Outlook Economic Outlook Tomorrow will Look A lot Like Today Paying down debt takes time No quick fix Recoveries after financial crises take much longer Consumers are saving more, but thats not good in the short-run Firms reluctant to hire No need for more workers Cant find workers with the right skills In the next 12-24 months, expect Moderate growth and a stubbornly high unemployment rates Volatile financial markets Little threat of inflation or rising interest rates

16

The Forecast Source: NATIONAL ASSOCIATION OF REALTORS ® October 2011 Forecast

17

The Future…Continued Uncertainty Shadow Inventory… How Much is Still Out There? When Will Prices Hit Bottom and Bounce? Whats Up in Washington? Too tight financing requirements, especially for Condo Market, Investors. GSE Reform. MID… Eliminated or Revised come 2013. QRM… The End for 30 Year Mortgages? Jobs, Jobs, Jobs… and Consumer Confidence. Recovery… It Needs to FEEL Like Recovery.

Similar presentations

Shall Rise Again – Just you Wait! 48 th ASU/Chase Economic Forecast>")

YOU 1 x 1 = 1 x 10 =10 1 x 1 = 1 x 3 =3 1 x 1 = 1 x 2.75 =2.75 1 x 1 = 1 x 2.50 =2.5 1 x 1 = 1 x 2 =2 1 x 1 = 1.>")