Download presentation

Presentation is loading. Please wait.

1

Essex Mortgage Brings CALHFA to you!

2

How do you know what program you want?

Do you want to work with an FHA or Conventional loan? Do you want a 1st, 2nd, and 3rd or just a 1st and 2nd? Is your borrower a FTHB or not? You have 10 product options, but they all surround these 3 basic descriptions! CalHFA 1st (Conventional or FHA) and a 2 ½% rate My Home Assistance 2nd ; loan based on 3 ½ % of sales price or appraised value, whichever is less; FTHB always required when using My Home Assistance. Cal Plus 1st (Conventional or FHA) and a ZIP 2nd 0% rate(2nd loan amount based on 3 or 4% of 1st loan amount – FTHB not required when using ZIP only. Cal Plus 1st (Conventional or FHA) with a My Home Assistance 2nd and ZIP 3rd ; FTHB require because you are adding this with a My Home. NOTE: THE ZIP and My Home can only be used for down payment and/or closing cost assistance. This is not to be used to pay the difference in sales price and appraised value if the sale price is higher. It also can not be used for paying off borrower debt.

and a 2 ½% rate My Home Assistance 2nd ; loan based on 3 ½ % of sales price or appraised value, whichever is less; FTHB always required when using My Home Assistance. Cal Plus 1st (Conventional or FHA) and a ZIP 2nd 0% rate(2nd loan amount based on 3 or 4% of 1st loan amount – FTHB not required when using ZIP only. Cal Plus 1st (Conventional or FHA) with a My Home Assistance 2nd and ZIP 3rd ; FTHB require because you are adding this with a My Home. NOTE: THE ZIP and My Home can only be used for down payment and/or closing cost assistance. This is not to be used to pay the difference in sales price and appraised value if the sale price is higher. It also can not be used for paying off borrower debt")

3

Comparing Programs Can only add an MHA 2nd 11 01 2016 $417,000 Max 1st

CalHFA Con CalHFA FHA CalPlus Con CalPlus FHA MHA 2nd ZIP (2nd or 3rd) $417,000 Max 1st Can only add an MHA 2nd $417,000+MIP Max 1st Can only add a MHA 2nd Two Options: Can add ZIP only; or can add a MHA and ZIP $417,000 + MIP Max 1st Can add ZIP only or can add a HMA and ZIP 2 ½% rate 2nd’ ; 3 ½% of loan amount or s/p can only be used with CalHFA or Cal Plus Conventional or FHA – Must always be in 2nd position 3% or 4% of 1st loan amount; 0% interest rate can be used only with Cal Plus Conventional or FHA Requires FTHB Not required if only ZIP only; FTHB if using MHA Requires FTHB Home Education required for one occupying FTHB Home Education only required if borrower is a FTHB; not required for non FTHB’s unless adding MHA, then FTHB rules apply Home Education always required

$417,000 Max 1st. Can only add an MHA 2nd. $417,000+MIP Max 1st. Can only add a MHA 2nd. Two Options: Can add ZIP only; or can add a MHA and ZIP. $417,000 + MIP Max 1st. Can add ZIP only or can add a HMA and ZIP. 2 ½% rate 2nd’ ; 3 ½% of loan amount or s/p. can only be used with CalHFA or Cal Plus Conventional or FHA – Must always be in 2nd position. 3% or 4% of 1st loan amount; 0% interest rate can be used only with Cal Plus Conventional or FHA. Requires FTHB. Not required if only ZIP only; FTHB if using MHA. Requires FTHB. Home Education required for one occupying FTHB. Home Education only required if borrower is a FTHB; not required for non FTHB’s unless adding MHA, then FTHB rules apply. Home Education always required")

4

Comparing Programs (cont.)

CalHFA Con CalHFA FHA Cal Plus Con Cal Plus FHA MHA 2ND ZIP (2nd or 3nd) 640 Minimum FICO No manual underwrite 660 FICO if manual underwrite Depending on 1st TD SFR, Condos and PUD’s Same same N/O co borrower are not allowed Co Signers are NOT allowed Co Signers ARE allowed Same as 1st TD Not subject to recapture 3 Years Tax Returns required for all FTHB 3 Years Tax Returns required for all FTHB (If only using ZIP and borrower is not a FTHB, only 1 year tax returns required 45% Max DTI 43% if Manual underwrite

640 Minimum FICO. No manual underwrite. 660 FICO if manual underwrite. Depending on 1st TD. SFR, Condos and PUD’s. Same. same. N/O co borrower are not allowed. Co Signers are NOT allowed. Co Signers ARE allowed. Same as 1st TD. Not subject to recapture. 3 Years Tax Returns required for all FTHB. 3 Years Tax Returns required for all FTHB (If only using ZIP and borrower is not a FTHB, only 1 year tax returns required. 45% Max DTI. 43% if Manual underwrite")

5

Comparing Programs (cont)

CalHFA Con CalHFA FHA CalPlus Con Cal Plus FHA MHA 2ND ZIP (2nd or 3nd) When using MCC, MCC guidelines apply FHA deduct from PITI Conventional add to income MI – Genworth 18% on 97% LTV 16% on 95% LTV FHA MIP MI 18% on 97% LTV Genworth n/a Home Warranty must include water heater(s), air conditioning and heating Home Warranty same as Conventional, but FHA also required oven stove and range

When using MCC, MCC guidelines apply. FHA deduct from PITI. Conventional add to income. MI – Genworth. 18% on 97% LTV. 16% on 95% LTV. FHA MIP. MI 18% on 97% LTV. Genworth. n/a. Home Warranty must include water heater(s), air conditioning and heating. Home Warranty same as Conventional, but FHA also required oven stove and range")

6

Compare: My Home Assistance to ZIP

Can only be used as a 2nd with a CalHFA 1st or CalPlus 1st Can only be used as 2nd or 3rd with a CalPLUS 1st. (Must be in third position if used with My Home Assistance 2 ½% Interest Rate – Simple Interest 0% Interest Rate Loan amount: 3 1/2 % of Sales Price or appraised value, whichever is less Loan amount can be 3% or 4% of 1st loan amount (including MIP) (see options) Must be a FTHB Do not need to be a FTHB Home education always required Home Education required only if FTHB 1 Year HOW Warranty required to cover water heater(s), air conditioning and heating – if placed with an FHA you must also include oven/stove/range 1 Year HOW Warranty required only if a FTHB. Must cover water heater(s), air conditioning, heating and if with an FHA, must include oven stove and range.

(see options) Must be a FTHB. Do not need to be a FTHB. Home education always required. Home Education required only if FTHB. 1 Year HOW Warranty required to cover water heater(s), air conditioning and heating – if placed with an FHA you must also include oven/stove/range. 1 Year HOW Warranty required only if a FTHB. Must cover water heater(s), air conditioning, heating and if with an FHA, must include oven stove and range")

7

First Time Homebuyers and Education Requirements Required: Always required on My Home, MCC and if using ZIP and borrower is a FTHB First Time Homebuyer (FTHB) Home Education For CalHFA purposes, a FTHB is defined as a borrower who has not had any ownership interest in any principal residence during the previous 3 years. If currently owns a non owner residence, 3 years of cancelled checks would have to be provided to show paying rent elsewhere; living with parents would not suffice. This would only be require if DU calls for a VOR. If no VOR is called for, then no cancelled checks would be required. Home Education is required for “one” occupying first-time homebuyer

Home Education. For CalHFA purposes, a FTHB is defined as a borrower who has not had any ownership interest in any principal residence during the previous 3 years. If currently owns a non owner residence, 3 years of cancelled checks would have to be provided to show paying rent elsewhere; living with parents would not suffice. This would only be require if DU calls for a VOR. If no VOR is called for, then no cancelled checks would be required. Home Education is required for one occupying first-time homebuyer")

8

Fees and Lock Periods FEES FOR THE PROGRAM LOCK PERIODS

BORROWER PAID ONLY Broker Compensation 2.375% or $3000 whichever is more (must pass 3% points and fees test) 1st TD: $1350 Essex Admin Fee 2nd TD: If using My Home Assistance: $250 Essex Processing Fee 2nd TD: If using ZIP for a 2nd or 3rd: $11.95 MERS Fee MCC $450 Actual Fee – ALWAYS DISCLOSE $750Thursday, August 25, 2016 IN CASE PROGRAM CHANGES. Home Warranty fee Third Party Contractors must obtain their fee directly from broker. Essex will not reimburse. LOCK WHEN ALL PTD’S ARE CLEAR Lock Period is for 30 days CalHFA turn times can be found at: 8/24/20168/24/2016

1st TD: $1350 Essex Admin Fee. 2nd TD: If using My Home Assistance: $250 Essex Processing Fee. 2nd TD: If using ZIP for a 2nd or 3rd: $11.95 MERS Fee. MCC $450 Actual Fee – ALWAYS DISCLOSE $750Thursday, August 25, 2016 IN CASE PROGRAM CHANGES. Home Warranty fee. Third Party Contractors must obtain their fee directly from broker. Essex will not reimburse. LOCK WHEN ALL PTD’S ARE CLEAR. Lock Period is for 30 days. CalHFA turn times can be found at: 8/24/20168/24/")

9

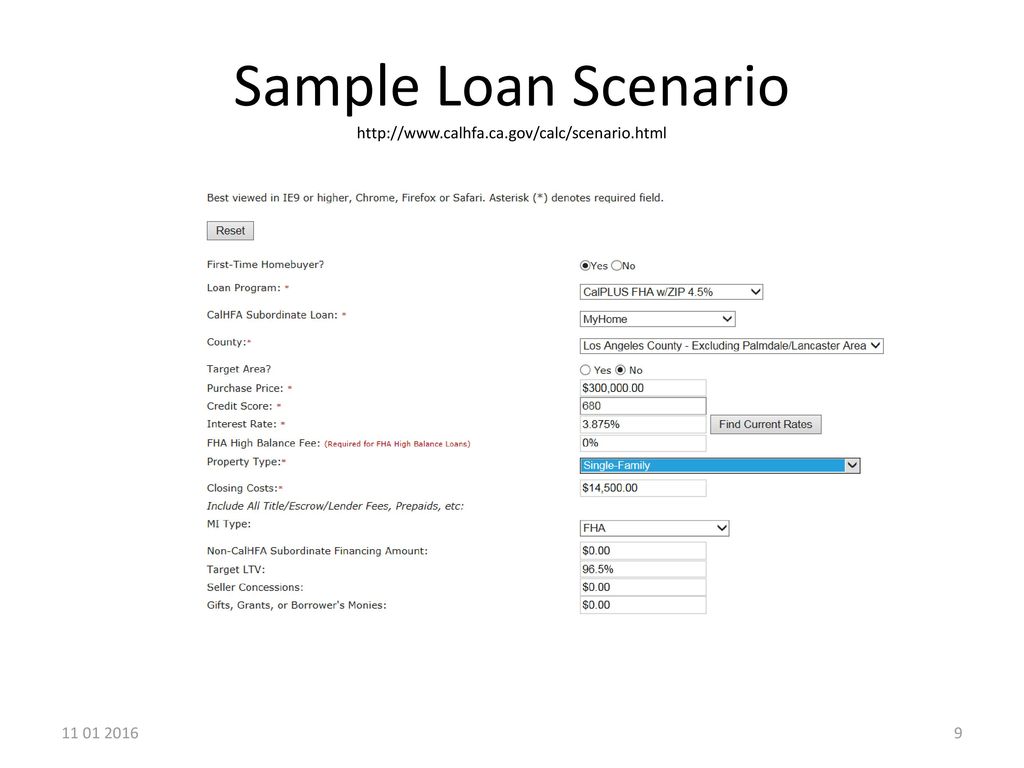

Sample Loan Scenario http://www.calhfa.ca.gov/calc/scenario.html

10

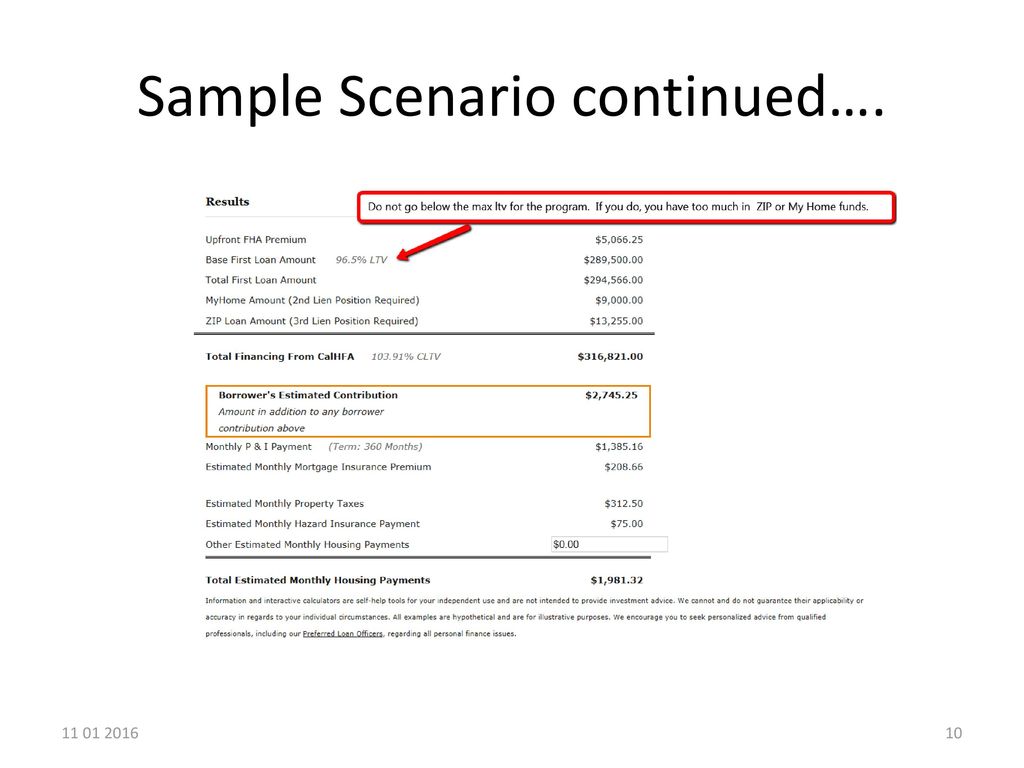

Sample Scenario continued….

11

Property Guest Houses (granny units) are eligible, can not be income producing Zoned SFR Cannot be zoned for 2-4 No income producing; personal use only No Manufactured housing (Essex requirement) No Leasehold Non permitted additions/alterations per FNMA or FHA guidelines Lot size – max 5 acres

No Leasehold. Non permitted additions/alterations per FNMA or FHA guidelines. Lot size – max 5 acres")

12

Income Calculations - Differences

Lender –Qualifying Income CalHFA – Eligibility In come Same standard calculations per guidelines Average 2 years Plus YTD Exclude variable income that does not have a 2 year history Exclude child support that has less than 3 years continuance Gross up the non-taxable income Include all borrower’s income Average last year and YTD – max 24 months Include variable income, even if no history Include child support even if it does not continue Do not gross up non-taxable income

13

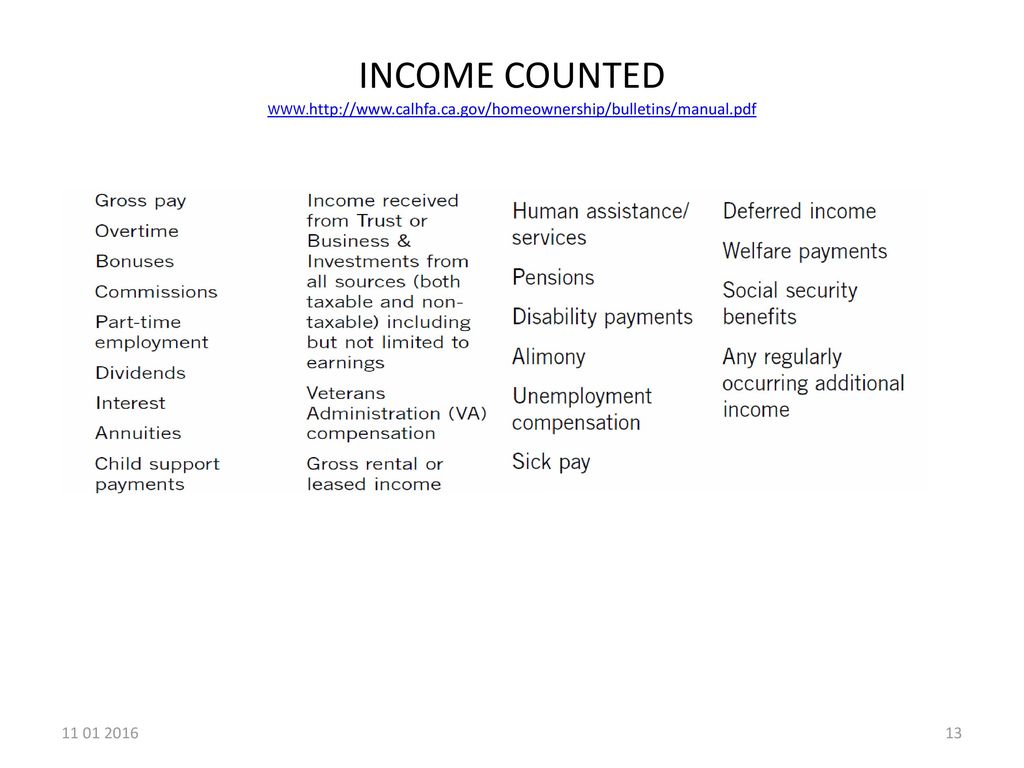

INCOME COUNTED WWW. http://www. calhfa. ca

14

How to Submit 1st TD 2nd TD 3rd TD (if there is a 3rd)

Broker to use additional Addendum Submission Sheet for CalHFA in addition to regular Submission Sheet. Choose the Option Plan. Broker to register and create a loan number for each loan submitted Broker to register and create a loan number Essex will disclose Submit submission sheet & addendum, fees worksheet, wet signed 4506T, and complete credit package 1003 for the 2nd (3.2) 1003 for the 3rd (3.2) Additional Forms for the program: CALHFA Borrower Affidavit and Tax Affidavit if applicable (forms on Essex website) N/A 3 years 1040’s for all 1st time homebuyers and 1 year for Non FTHB (NOTE: MHA requires you to be a FTHB)

1003 for the 3rd (3.2) Additional Forms for the program: CALHFA Borrower Affidavit. and Tax Affidavit if applicable (forms on Essex website) N/A. 3 years 1040’s for all 1st time homebuyers and 1 year for Non FTHB (NOTE: MHA requires you to be a FTHB)")

15

CALHFA Addendum Submission Sheet http://www. essexwholesale

16

You have one chance to get this form right

You have one chance to get this form right! So please pay careful attention! The amount of people who will be living in the house will determine your income limitation

17

Additional CALHFA Forms at submission:

CalHFA Addendum Submission Sheet CALHFA Borrower Affidavit Tax Return Affidavit (only required if not required to file 1040’s) These forms can be found at Click on Products – CALFHA Home Buyer Education: (required for one occupying 1st time buyer – not required for non-1st time homebuyers if using ZIP only – it is required for all My Home Assistance products) On line:

These forms can be found at Click on Products – CALFHA. Home Buyer Education: (required for one occupying 1st time buyer – not required for non-1st time homebuyers if using ZIP only – it is required for all My Home Assistance products) On line:")

18

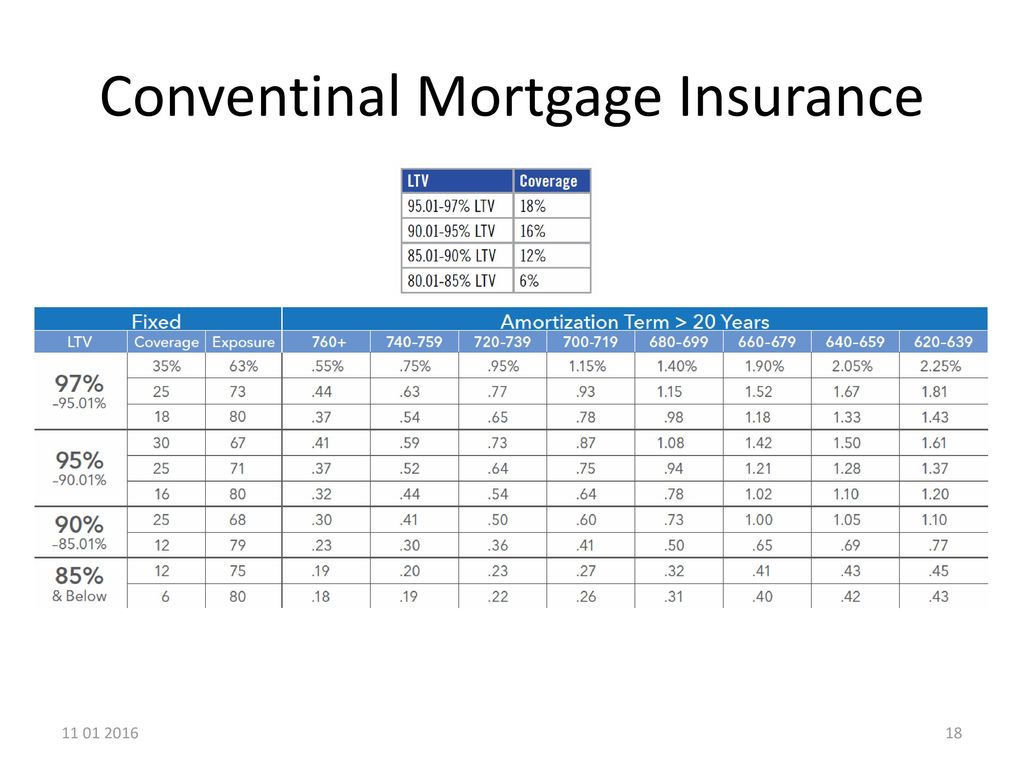

Conventinal Mortgage Insurance

19

CALHFA Handbooks (for income) (for scenarios)

(for scenarios)")

20

Repayment Repayment of the principal and interest on the subordinate loan shall be due and payable at the earliest of the following events: • Transfer of title • Sale of the property* • Payoff of the first loan • Refinance of the first loan, unless the My Home is subordinated • The formal filing and recording of a Notice of Default (unless rescinded) *My Home loans behind an FHA first mortgage may be assumed or paid off when the first mortgage is assumed

*My Home loans behind an FHA first mortgage may be assumed or paid off when the first mortgage is assumed")

21

Conventional Income Limits, effective July 18, 2016

22

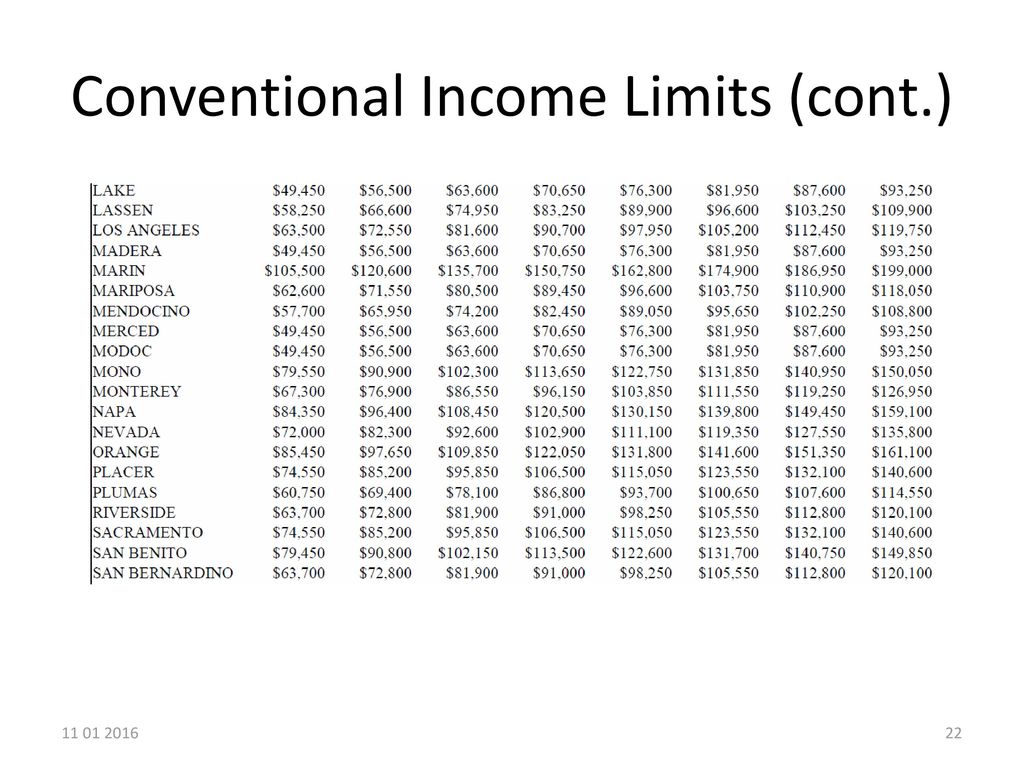

Conventional Income Limits (cont.)

23

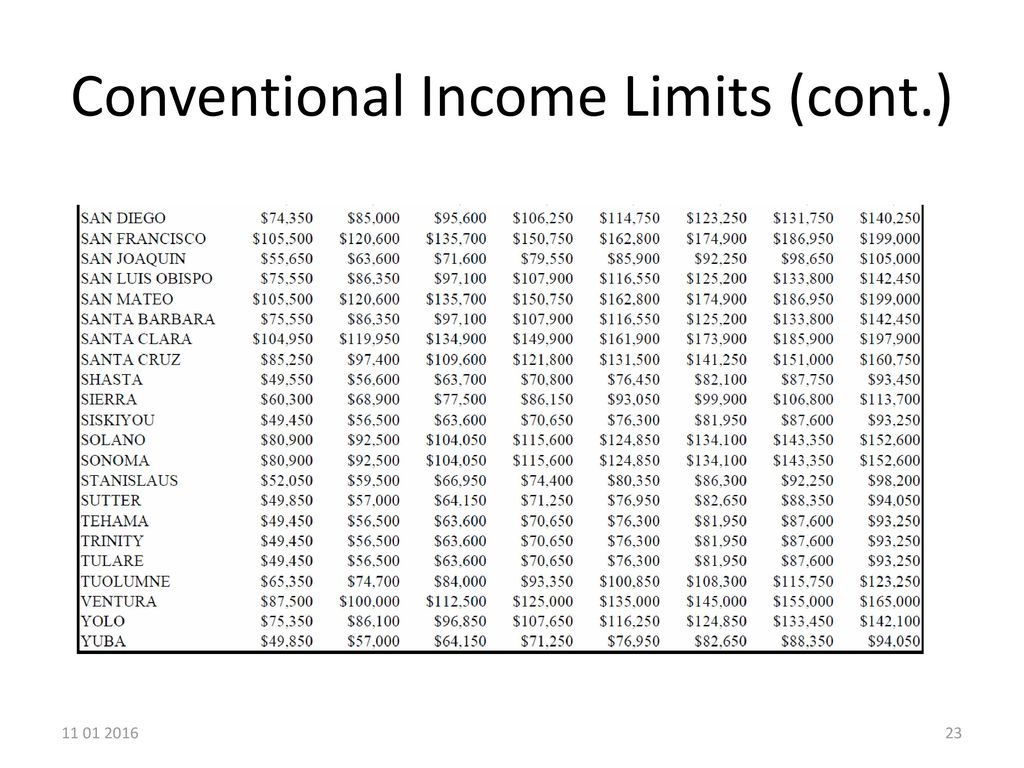

Conventional Income Limits (cont.)

24

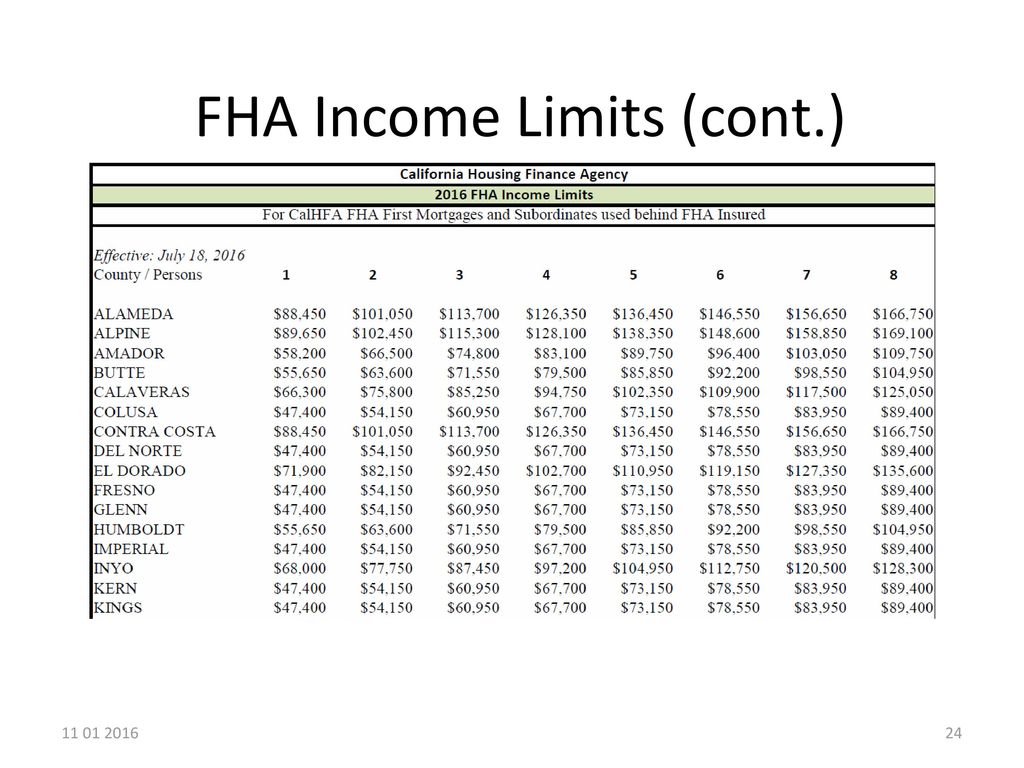

FHA Income Limits (cont.)

25

FHA Income Limits

26

Income Limits cont.

27

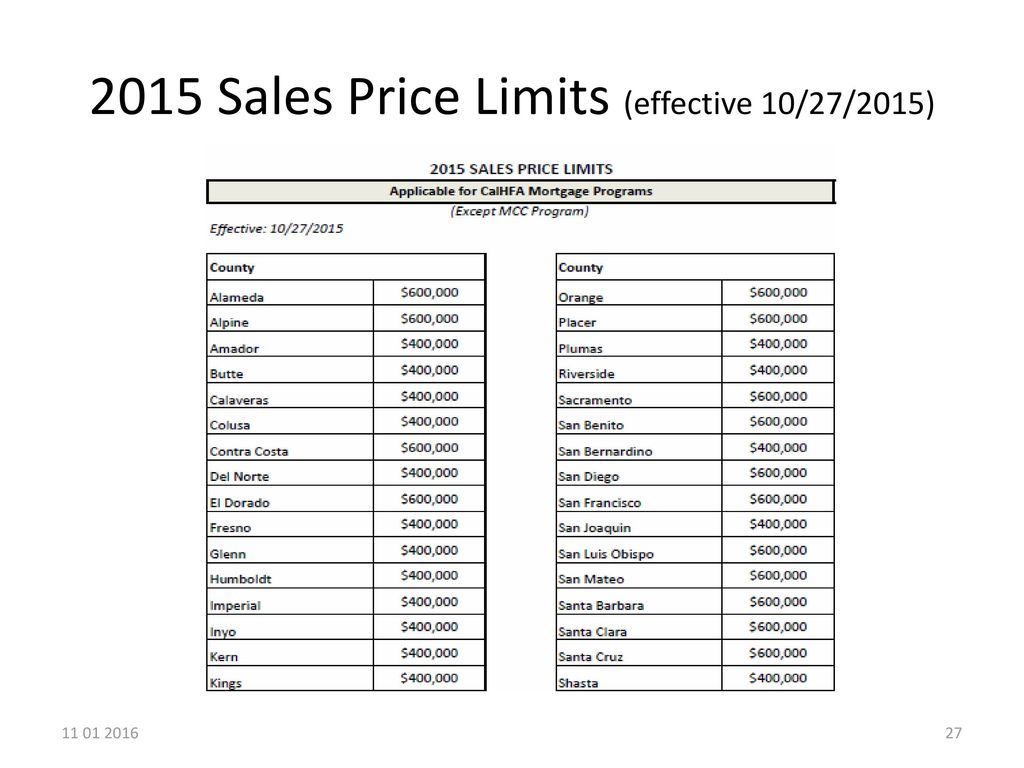

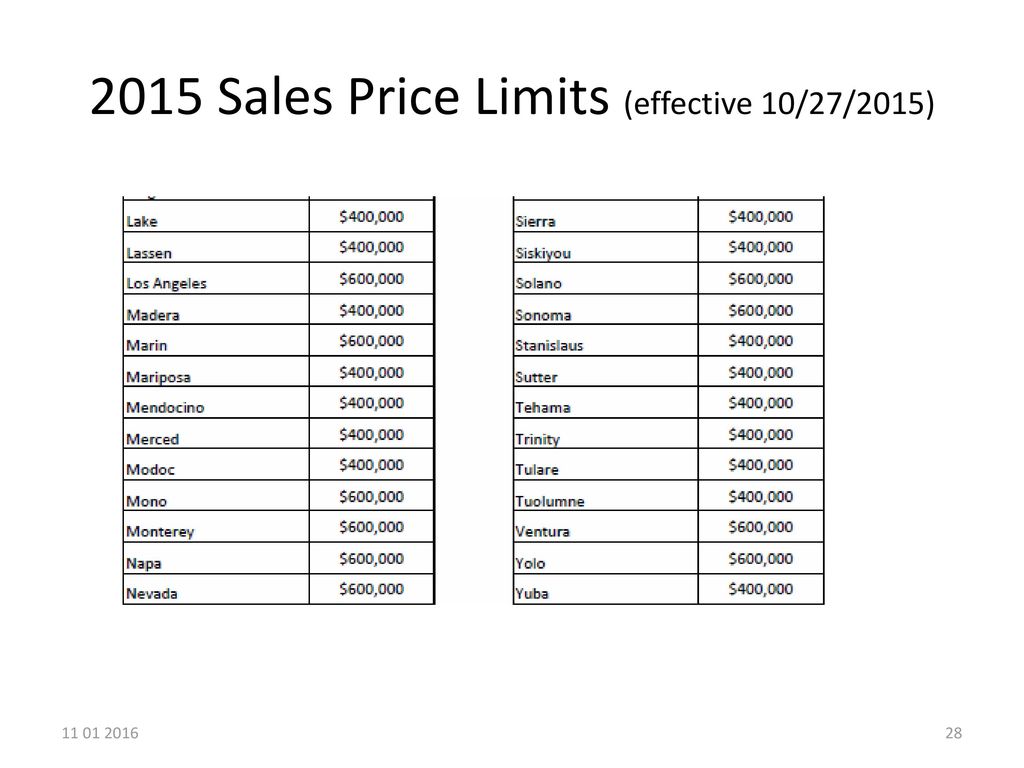

2015 Sales Price Limits (effective 10/27/2015)

28

2015 Sales Price Limits (effective 10/27/2015)

29

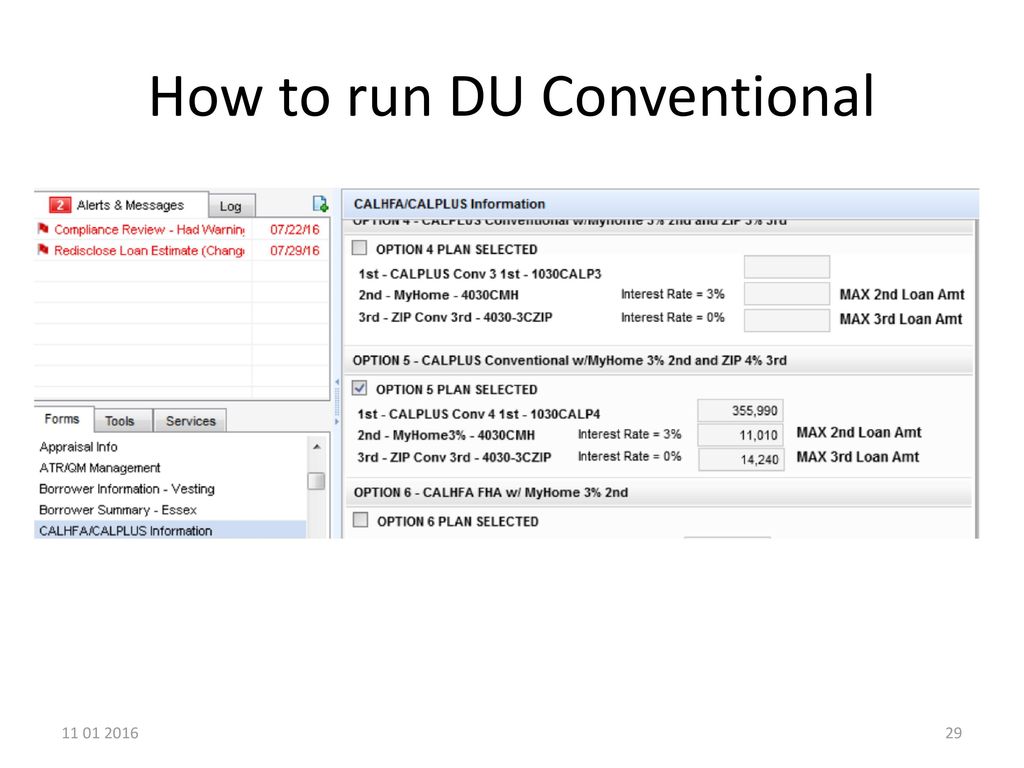

How to run DU Conventional

30

Conventional DU cont.

31

Conventional DU cont.

32

How to run DU FHA

33

DU FHA cont.

Similar presentations

Increase your disposable income. Increase your buying power. Decrease your tax liability 1 1/29/2015.>")

MORTGAGE CREDIT CERTIFICATE Increase your disposable income. Increase your buying power. Decrease your tax liability 1 6/12/2016.>")

>")