Download presentation

Presentation is loading. Please wait.

1

AIM:WHAT ARE THE ECONOMIC DECISIONS ASSOCIATED WITH GOING TO COLLEGE? DO NOW: HTTP://WWW.NPR.ORG/2014/02/11/275297408/GOING- TO-COLLEGE-MAY-COST-YOU-BUT-SO-WILL-SKIPPING- IT IS COLLEGE WORTH IT?

2

TED TALK ACTIVITY http://www.ted.com/talks/shai_reshef_a_tuition_free_college_ degree

3

AIM: WHAT ARE THE ECONOMIC DECISIONS AND RESPONSIBILITIES ASSOCIATED WITH BUYING A HOUSE? DO NOW: DO YOU EVENTUALLY WANT TO BUY A HOUSE? WHY IS THIS A GOAL?

4

INTRODUCTION Housing is the largest personal expenditure. About 1/3 of a person’s income. Choosing where to live is based upon a person’s goals, values, needs, and wants. Places to live include: House, apartment, condo, mobile home, etc.

5

REASONS FOR MAKING A HOUSING CHOICE Personal and financial goals Personal values, needs, and wants Amount of money available for housing costs Financial resources and readiness Credit history Real estate prices Location preference Expected length of stay in particular place

6

COSTS OF RENTING Monthly rent Security deposit Utilities – electricity, water, garbage, etc. Renter’s insurance

7

RENTING A lease is a legal contract between the tenant and the landlord, specifying the responsibilities and rights of both parties. Identifies the rent amount, security deposit amount and specifications, payment for utility bills, late payment penalties, length of lease, eviction terms, etc. This is between the landlord and the tenant Landlord Owner of the rental property. May perform management duties or hire a property manager. Property manager - may charge a fee to the landlord to perform the management task Duties may include: May collect rent and deposits, pay utility bills, complete repairs and maintenance, watch over the property, respond to tenant complaints, assign new tenants, etc.

8

RENTING CONTINUED Tenant (renter) The person who rents the property. Renters are generally People who choose not to own a home. People who cannot afford to own a home. The tenant pays rent to the landlord which allows them to live in the rental property. Rent The cost of using someone else’s property.

9

MOVING INTO A RENTAL Upon moving into a new place, people are usually required to pay a security deposit and sign a lease. Security deposit An advance payment to cover anything beyond normal wear and tear on the unit.

10

ADVANTAGES OF RENTING Low move-in costs Fixed monthly expenses Easy to move Location choices (may be close to work or school) Less maintenance and repair work Fewer responsibilities May offer extra amenities such as a tennis court or pool Typically less expensive than home ownership May be able to save for other wants or needs if renting a less expensive apartment Other expenses may be included in rent payment such as electricity, water, sewer, and/or garbage

Less maintenance and repair work Fewer responsibilities May offer extra amenities such as a tennis court or pool Typically less expensive than home ownership May be able to save for other wants or needs if renting a less expensive apartment Other expenses may be included in rent payment such as electricity, water, sewer, and/or garbage")

11

DISADVANTAGES OF RENTING Subject to terms of a lease Rent may change with little notice Less privacy and transient neighbors. Restrictions on noise level, pets, etc. Fewer opportunities to upgrade apartment such as new carpet, paint, or wallpaper. When leaving a property, no equity is returned as it would be if selling a home. No tax deductions May lose rental if the property is sold.

12

COSTS OF OWNERSHIP Monthly mortgage payments Down payment (one time cost) Closing costs (one time cost) Utilities – electricity, water, garbage, etc. Homeowner’s insurance Real estate property taxes Maintenance

13

HOME OWNERSHIP Home ownership - the buyer has purchased a housing unit as property Goal of many Americans A large financial decision Owning a home is an investment because if a person sells a home for more than what it was bought for, the person makes money. This is called equity. Financial planning and savings can assist a person in planning for the benefits of home ownership later in life.

14

PURCHASING A HOME 90% of buyers take out a mortgage A home loan in which the real estate is the collateral Collateral is an item promised to the lender if the borrower does not pay back the loan, usually the home. Down payment Amount of money paid on the home at time of purchase Typically 10 – 20% of the purchase price of the home Recommended purchase price amount an individual should pay for a home 2 ½ times their annual household income

15

ADVANTAGES OF OWNERSHIP Build equity which can be borrowed against if necessary Pride of ownership Feel more comfortable and have more privacy Stable mortgage payments More room and storage Improvement of buyer’s credit rating Income tax deductions for property taxes and mortgage interest Potential for property to increase in value Free to make home improvements and have pets (items typically not allowed in rentals)

")

16

DISADVANTAGES OF OWNERSHIP Large down payment Move-in costs Insurance costs Possible for property to decrease in value Time, money, and energy commitment Repair and maintenance costs Property taxes can raise substantially Money is tied up in the home May take several months to sell a home if trying to relocate

17

KEEP IN MIND... People are always paying for a home. It’s just a matter of whether it is for themselves or their landlord.

18

MONOPOLY VALUE – WHO MADE THE RIGHT CHOICES? 1. Split into eight groups within your team. 2. Research the property values of each “section”. 3. Decide whether it would be a smarter financial decision to RENT or BUY those properties. 4. Prove and defend your claim. 5. Think like an investor and DO THE MATH. How much could you earn/save?

19

AIM: WHAT ARE THE ECONOMIC DECISIONS AND RESPONSIBILITIES ASSOCIATED WITH GETTING MARRIED OR HAVING CHILDREN? DO NOW: ESTIMATE THE AVERAGE COST OF A WEDDING. (ACTIVITY #1 ON HANDOUT)

.")

20

WEDDINGS

21

FILING TAXES Generally, there are two common filing statuses: married filing jointly and single. But there’s a third, less common status: married filing separately. Married filing separately is not the same as filing as a single person—it means that you’re married, but you each file your own return, so you don’t take legal responsibility for your spouse’s return, and your incomes and expenses are considered separately. The federal government now recognizes same sex marriages, which gives married same-sex couples this same choice between filing statuses.

22

INSURANCES AND RETIREMENT Besides renter’s or homeowners insurance, expenses are broken into two other expenditures: Health Insurance Ms. R’s “rule of thumb” – if debating between taking two different jobs with a difference in salaries, go with the company that offers you greater health benefits Auto Insurance Retirement: Matched by employers: 401K 403b – tax deferred retirement account Personal Retirement Account: Roth IRA

23

DIVORCE In Western cultures, 90% of the population marries by age 50. Current divorce rate in America: 50% Average cost of divorce in NY: $15,000- $20,000 Three costs associated with divorce: Assets Alimony Child Support

24

KIDS http://gothamist.com/2014/08/19/condoms_4life.php http://www.cnpp.usda.gov/sites/default/files/expenditures_on_children_by_fam ilies/CRC2013InfoGraphic.pdf Class Articles

25

AIM: HOW DO THE GOALS OF THE NATIONAL ECONOMY IMPACT THE INDIVIDUAL? DO NOW: WHAT ARE TAXES?

26

Economic Impact of Taxes Incidence of a Tax Resource Allocation Behavior Adjustment Income Redistribution Productivity and Growth

27

THREE CATEGORIES OF TAXES Proportional (City Income Tax) Progressive (Federal Income Tax) Regressive (State Sales Tax) Percentage of income paid in taxes stays the same regardless of income Example: Medicare Percentage of income paid in taxes goes up as income goes up Example: Individual Income Tax Percentage of income paid in taxes does down as income goes up Example: Sales Tax

Progressive (Federal Income Tax) Regressive (State Sales Tax) Percentage of income paid in taxes stays the same regardless of income Example: Medicare Percentage of income paid in taxes goes up as income goes up Example: Individual Income Tax Percentage of income paid in taxes does down as income goes up Example: Sales Tax")

28

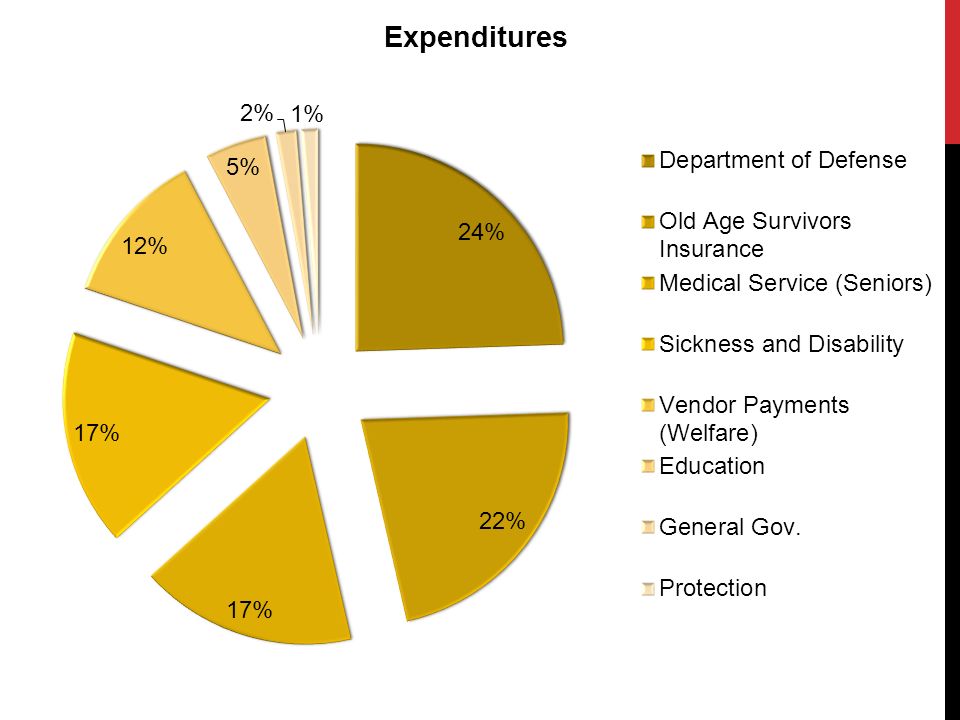

State Revenue -Intergovernmental Revenue (from federal government) -Sales Tax -Individual Income Tax State Expenditures -Intergovernmental Revenue (transferred to local government) -Higher Education

-Sales Tax -Individual Income Tax State Expenditures -Intergovernmental Revenue (transferred to local government) -Higher Education")

29

Individual Income Tax 1,121.3 Individual Income Tax 1,121.3 Old Age Survivors Insurance Tax 576.2 Old Age Survivors Insurance Tax 576.2 Corporate Income Tax 296.9 Corporate Income Tax 296.9 Hospital Insurance Tax 192.4 Hospital Insurance Tax 192.4 Disability Insurance Tax 97.8 Disability Insurance Tax 97.8 Federal Reserve Deposits 79.3 Federal Reserve Deposits 79.3 Unemployment Insurance Taxes 60.1 Unemployment Insurance Taxes 60.1 Transportati on Tax 49.6 Transportati on Tax 49.6 Customs Duties & Fees 27.4 Excise Tax 24.7 Excise Tax 24.7 Estate Tax 25 Estate Tax 25 4.3 4.2 Other 16 Other 16 Employee Retirement Insurance TaxRailroad Retirement Insurance Tax

31

IS THE AMERICAN TAX SYSTEM EFFICIENT AND FAIR? Please answer the above question in a one paragraph response on the class blog. Please respond to at least one other response. If you finish early, switch over to stock market game.

Similar presentations