Download presentation

Presentation is loading. Please wait.

1

INTRODUCTION TO SHIPPING ECONOMICS AND FINANCE 17/10/12

2

DETERMINANTS DEMANDS IN SHIPPING ACTIVITIES 17/10/12

SUPPLY IN SHIPPING ACTIVITIES 17/10/12

3

DETERMINANTS OF SUPPLY IN SHIPPING ACTIVITIES

17/10/12

4

DETERMINANTS OF SUPPLY IN

FREIGHT MARKETS THE MERCHANT FLEET FLEET PRODUCTIVITY SHIPBUILDING PRODUCTION SCRAPPING & LOSSES FREIGHT REVENUE

5

SHIPPING SUPPLY The supply of shipping services as being slow and ponderous in its response to changes in demand. Merchant ships generally take about a year to build and delivery may take 2–3 years if the shipyards are busy. This prevents the market from responding promptly to any sudden upsurge in demand. Once built, the ships have a physical life of 15–30 years, so responding to a fall in demand is a lengthy business, particularly when there is a large surplus to be removed.

6

SUPPLY OF SHIPPING The supply of shipping is made up of the carrying capacity of ship to move the cargo. This comprise 4 main factors: The number of ships – over last century no. of vessel decline but tonnage increases (?)/ carrying capacity increase Fleet productivity The size of ships – over last century vessels has grown bigger – 1955 slow growth but from 1955 – 1975 growth was spectacular. After that growth has stabilized. Port time Efficiency – the less time in port the more cargo the ship can carry. Main reason for container vessel replacing general cargo. Speed – increase speed obviously increases the supply of ships.

/ carrying capacity increase. Fleet productivity. The size of ships – over last century vessels has grown bigger – 1955 slow growth but from 1955 – 1975 growth was spectacular. After that growth has stabilized. Port time Efficiency – the less time in port the more cargo the ship can carry. Main reason for container vessel replacing general cargo. Speed – increase speed obviously increases the supply of ships.")

7

MERCHANTS FLEET In the long run scrapping and deliveries determine the rate of fleet growth. Since the average economic life of a ship is about 25 years, only a small proportion of the fleet is scrapped each year, so the pace of adjustment to changes in the market is measured in years, not months 17/10/12

9

Further, the average speed by ship size

*Selected maximum continuous ratings

11

17/10/12

12

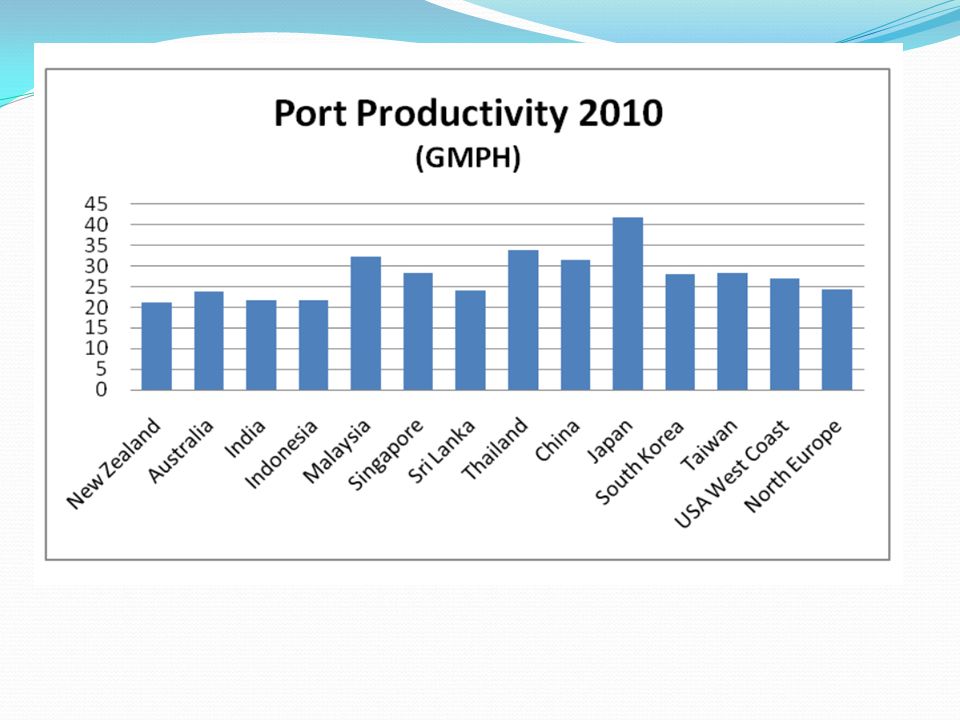

FLEET PRODUCTIVITY Productivity expressed in terms of ton miles per deadweight reached a peak of 35,000 in 1973, but by 1985 this had fallen to 22,000; in other words, productivity had fallen by over a third. The major swings in productivity in Figure 4.8 are mainly due to the deep recessions in the 1970s and 1980s when ships were very cheap and as a result were used inefficiently. In normal times the average ship carries about 7 tons of cargo per deadweight and does around 35,000 tanker ton miles. 17/10/12

13

SHIPBUILDING PRODUCTION

The shipbuilding industry plays an active part in the fleet adjustment process. In principle, the level of output adjusts to changes in demand – and over long periods this does happen. Adjustments in the level of shipbuilding output on this scale do not take place quickly or easily. Shipbuilding is a long-cycle business, and the time-lag between ordering and delivering a ship is between 1 and 4 years, depending on the size of orderbook held by the shipbuilders. Orders must be placed on the basis of an estimate of future demand and in the past these estimates have often proved to be wrong. 17/10/12

14

In January 2011, there were 103,392 commercial ships in service

In January 2011, there were 103,392 commercial ships in service with a combined tonnage of 1,396 million dwt. Looking at individual sectors, oil tankers accounted for 475 million dwt and dry bulk carriers for 532 million dwt, representing an annual increase of 5.5 % and 16.5 % respectively; The containership fleet reached 184 million dwt in January 2011(8.7% over 2010). The fleet of general cargo ships stabilised at 109 million dwt. The tonnage of liquefied gas carriers continued to grow, reaching 43 million dwt (an increase of 6.6%). (Source: UNCTAD Review of Maritime Transport 2011, p. 36)

. The fleet of general cargo ships stabilised at 109 million dwt. The tonnage of liquefied gas carriers continued to grow, reaching 43 million dwt (an increase of 6.6%). (Source: UNCTAD Review of Maritime Transport 2011, p. 36)")

15

Development of world fleet by millions of dwt*

Source: UNCTAD

16

Tanker new building dominated the period 1963–75, increasing from 5 m

Tanker new building dominated the period 1963–75, increasing from 5 m.dwt in 1963 to 45 m.dwt in 1975, when it accounted for 75% of shipbuilding output. The collapse of the tanker market after the 1973 oil crisis reversed this trend and tanker output fell to a trough of 3.6 m.dwt in 1984, accounting for only 1% of the tanker fleet. As the tanker fleet built in the 1970s needed to be replaced the trend was again reversed, and by 2006 tanker production had increased to 25.8 m. 17/10/12

17

SCRAPPING AND LOSSES The rate of growth of the merchant fleet depends on the balance between deliveries of new ships and deletions from the fleet in the form of ships scrapped or lost at sea. From Figure In 1973, only about 5 m.dwt of vessels were scrapped, compared with deliveries of over 50 m.dwt, with the result that the fleet grew rapidly. By 1982, scrapping had overtaken deliveries for the first time since the Second World War, accounting for 30 m.dwt compared with 26 m.dwt of deliveries. Thus scrapping, which appeared to be of little significance in 1973, was of major importance by the early 1980s. Whilst it is clear that scrapping has a significant part to play in removing ships from the market, explaining or predicting the age at which a ship will actually be scrapped is an extremely complex matter, and one that causes considerable difficulties in judging the development of shipping capacity. The reason is that scrapping depends on the balance of a number of factors that can interact in many different ways. The main ones are age, technical obsolescence, scrap prices, current earnings and market expectations. 17/10/12

18

During a recession, there is some chance of a freight market boom in the reasonably near future, hence it is unlikely to sell unprofitable ships for scrap because the possible earnings during a freight market boom are so great that they may justify incurring a small operating loss for a period of years up to that date. Naturally the oldest ships will be forced out by the cost of repairs but, where vessels are still serviceable, extensive scrapping to remove surplus capacity is only likely to occur when the shipping community as a whole believes that there is no prospect of profitable employment for the older vessels in the foreseeable future, or when companies need the cash so urgently that they are forced into ‘distress’ sales to ship breakers. It follows that scrapping will occur only when the industry’s reserves of cash and optimism have been run-down.

19

Baltic Exchange Dry Index (BDI) & Freight Rates

& Freight Rates")

21

As a result of orders placed prior to the 2008 crisis, new building deliveries reached a new record in the history of shipbuilding. There were 3,748 newbuildings with a gross tonnage of 96,433,000 GT. In terms of gross tonnage, 45.2 % of deliveries were of dry bulk carriers and 27.7 % were of tankers. New containerships accounted for 15.2%.

22

Gross tonnage is a volumetric measurement of the enclosed space in a ship. It has NOTHING to do with weight. The unit used is the gross TON. Deadweight tonnage is the WEIGHT in metric TONNES (1,000 kg) of cargo, fuel and stores that will put the ship down to its loadline marks. Actually, to be strictly correct, Gross tonnage is just an index and do not carry any unit. It's not really usable for anything in real life unless you hold a certificate as an officer for smaller ships, in which case 3000 GT is interesting. Other than that, it is something used by governing bodies to determine manning requirements and other boring stuff. Other than that, it is used by classification companies, P&Is, ports etc. to determine fees. It is often used to compare the size of ships, though it is as useless for comparing ships as TEUs or LOA. I.e. a 300 m VLCC will have a far larger GT than the Oasis of the Seas - despite the Oasis being both longer and wider... Same sort of goes to DWT. It isn't really a usable measure for anything that can be of interest to anyone except the shipowners and flag and port states.

23

World Tonnage on order (2000-2010) (thousands of Dwt)

(thousands of Dwt)")

24

FREIGHT REVENUE The supply of sea transport is influenced by freight rates. The ultimate regulator which the market uses to motivate decision-makers to adjust capacity in the short term, and to find ways of reducing their costs and improving their services in the long term. In the short run, supply responds to prices as ships adjust their operation speed and move to and from lay-up, while liner operators adjust their services. In the longer term, freight rates contribute to the investment decisions which result in scrapping and ordering of ships. 17/10/12

25

Freight Revenue / Transport costs

The transport cost element in the shelf price of consumer goods varies from product to product, but is ultimately marginal. For example, transport costs for a television set (typical shelf price of $700.00) amount to around $10.00 and only around $0.15 for of a kilo of coffee (typical shelf price $15.00). The typical cost to a consumer in the United States of transporting crude oil from the Middle East, in terms of the purchase price of gasoline at the pump, is less than a US cent per litre. The typical cost of transporting a tonne of iron ore from Australia to Europe by sea is about US $10. The typical cost of transporting a 20 foot container from Asia to Europe carrying over 20 tonnes of cargo is about the same as the economy airfare for a single passenger on the same journey. Table - Overview of Transport Costs Unit Shelf price Shipping costs TV set unit $ $ 10.00 DVD/CD player 1 unit $ $ 1.50 Vacuum cleaner 1 unit $ $ 1.00 Scotch Whisky Bottle $ $ 0.15 Coffee 1kg $ $ 0.15 Biscuits Tin $ $ 0.05 Beer Can $ $ 0.01

amount to around $10.00 and only around $0.15 for of a kilo of coffee (typical shelf price $15.00). The typical cost to a consumer in the United States of transporting crude oil from the Middle East, in terms of the purchase price of gasoline at the pump, is less than a US cent per litre. The typical cost of transporting a tonne of iron ore from Australia to Europe by sea is about US $10. The typical cost of transporting a 20 foot container from Asia to Europe carrying over 20 tonnes of cargo is about the same as the economy airfare for a single passenger on the same journey. Table - Overview of Transport Costs Unit. Shelf price Shipping costs. TV set 1 unit $ $ DVD/CD player 1 unit $ $ Vacuum cleaner 1 unit $ $ Scotch Whisky Bottle $ $ Coffee 1kg $ $ Biscuits Tin $ 3.00 $ Beer Can $ 1.00 $")

26

17/10/12

27

THANK YOU 17/10/12

Similar presentations