Download presentation

Presentation is loading. Please wait.

1

Information Technology Finance 724/824 SIM Class Summer 2009 Russell Kolmin Zachary McAllister Paul Melko Mahavir Sanghavi Daniel Schuerman

2

Agenda Sector Overview Business Analysis Economic Analysis Financial Evaluation Valuation Recommendation Agenda

3

SIM Portfolio Composition S&P 500 Weight SIM Weight+/- Consumer Discretionary 8.97%7.50%-1.46% Consumer Staples 12.32%12.36%0.04% Energy 12.05%10.68%-1.37% Financials 13.70%9.33%-4.37% Health Care 14.06%13.58%-0.49% Industrials 9.79%11.57%1.78% Information Technology 18.43%20.19%1.76% Materials 3.20%4.12%0.92% Telecommunication Services 3.39%3.28%-0.11% Utilities 4.10%3.87%-0.23% Cash 0.00%3.53%

4

SIM Weightings Relative S&P 500 SIM Weighting Relative S&P

5

Sector Overview Description Total number of Companies Adj MktCap (in Miilions) QTDYTD S&P 500500 8,587,679 6.52%8.42% Energy40 1,059,652 5.98%2.55% Materials28 290,442 11.80%25.52% Industrials58 841,227 6.35%-1.82% Consumer Discretionary81 779,409 8.03%16.16% Consumer Staples41 1,019,872 5.88%2.24% Health Care53 1,188,645 5.71%4.70% Financials79 1,149,074 4.16%-0.80% Information Technology76 1,621,022 9.14%35.42% Telecommunications Services 9 289,992 1.86%-4.99% Utilities35 348,343 5.78%1.47%

QTDYTD S&P ,587, %8.42% Energy40 1,059, %2.55% Materials28 290, %25.52% Industrials58 841, %-1.82% Consumer Discretionary81 779, %16.16% Consumer Staples41 1,019, %2.24% Health Care53 1,188, %4.70% Financials79 1,149, %-0.80% Information Technology76 1,621, %35.42% Telecommunications Services 9 289, %-4.99% Utilities35 348, %1.47%")

6

Sector Overview Sector Industry% of S&P500SIM Holdings Information Technology Application Software0.52% Communications Equipment2.82% Computer Storage/Peripherals0.60% Computer Hardware5.04% AAPL HPQ Electronic Components0.38% Electronic Equipment0.13% Electronic Manufacturing Services0.05% Home Entertainment Software0.08% Internet Software and Services1.89% IT Consulting and Services0.10%(NCR) Office Electronics0.80% Semiconductor Equipment0.35% Semiconductors2.35%INTC Services - Data Processing0.94% Systems Software3.51% ORCL MSFT

Office Electronics0.80% Semiconductor Equipment0.35% Semiconductors2.35%INTC Services - Data Processing0.94% Systems Software3.51% ORCL MSFT")

7

Sector Overview TickerCompanyMarket Cap% of S&P 500 % of Info Tech Sector MSFTMicrosoft208.72.43%12.87% IBM 154.111.79%9.51% AAPLApple143.311.67%8.84% GOOGGoogle141.121.64%8.71% CSCOCisco126.21.47%7.79% ORCLOracle111.811.30%6.90% INTCIntel108.321.26%6.68% HPQHewlett Packard99.551.16%6.14% QCOMQualcomm78.710.92%4.86% TXNTexas Instruments30.390.35%1.87%

8

Business Analysis-Info Technology Largest sector with a focus primarily on computer hardware and software. Sector growth depends primarily on technological advancement and innovation. –Unpredictable: what is hot now may be obsolete in 6 months Dependence on cutting edge technology leads to enormous R&D costs. –These R&D costs are the largest barrier to entry

9

Business Analysis (cont.) Cyclical Sector with large impact on S&P500 –Tends to follow market cycles, can be highly volatile –A leading indicator during recovery, growth periods Largely impacted by Corporate and Consumer Spending –Current Corporate/Consumer spending is down, however with ongoing technological advancements, corporations will be upgrading IT as recovery begins Primary indicator is Personal Computer demand –PC Demand tends to create “pin-action” on all other IT components (i.e. Software, Peripherals, Storage, Services) New Trend – Cell phones becoming handheld PCs –Leads to need for PC style software, hardware, storage, etc.

New Trend – Cell phones becoming handheld PCs –Leads to need for PC style software, hardware, storage, etc..")

10

Business Analysis (cont.) Information Technology Life Cycle – primarily impacted by the life cycle of PCs –PCs’ typical life-span = 3-5 yrs (physically longer, however obsolete) Demand – largely affected by developed countries, growth potential in under-developed –60% of all PCs owned by 15% of the world-wide population 1 LOTS of untapped demand –Increasing handheld device demand/infrastructure Tel-com sector expanding infrastructure and increased cell phone capabilities desired 1: www.garnter.com (June 23, 2008)www.garnter.com

Information Technology Life Cycle – primarily impacted by the life cycle of PCs –PCs’ typical life-span = 3-5 yrs (physically longer, however obsolete) Demand – largely affected by developed countries, growth potential in under-developed –60% of all PCs owned by 15% of the world-wide population 1 LOTS of untapped demand –Increasing handheld device demand/infrastructure Tel-com sector expanding infrastructure and increased cell phone capabilities desired 1: (June 23, 2008)")

11

Business Analysis (cont.) OpportunitiesGrowth Opportunities –US Healthcare reform (Electronic Patient records) –Windows 7 (How will it be received?) Office 2010 –Increased Corporate Spending/ Consumer Saving Rate (following recovery, where will money be spent?) –Stimulus Package (how will broadband infrastructure expansion impact demand?) –Asia Growth/Savings Rates (exploding demand?) RisksGrowth Risks –Regulations (China, Iran, North Korea, etc) –Double-dip recession or unstable recovery

OpportunitiesGrowth Opportunities –US Healthcare reform (Electronic Patient records) –Windows 7 (How will it be received ) Office 2010 –Increased Corporate Spending/ Consumer Saving Rate (following recovery, where will money be spent ) –Stimulus Package (how will broadband infrastructure expansion impact demand ) –Asia Growth/Savings Rates (exploding demand ) RisksGrowth Risks –Regulations (China, Iran, North Korea, etc) –Double-dip recession or unstable recovery")

12

Business Cycle Analysis Investopedia.com

13

Business Analysis Summary IT Growth Opportunities outweigh risks –However double-dip still possible Demand is Strong Long Term –IT becoming a business staple with massive growth potential innovation Short-term…what happens with Windows7 and Corporate Spending? –It appears IT spending is going to increase

14

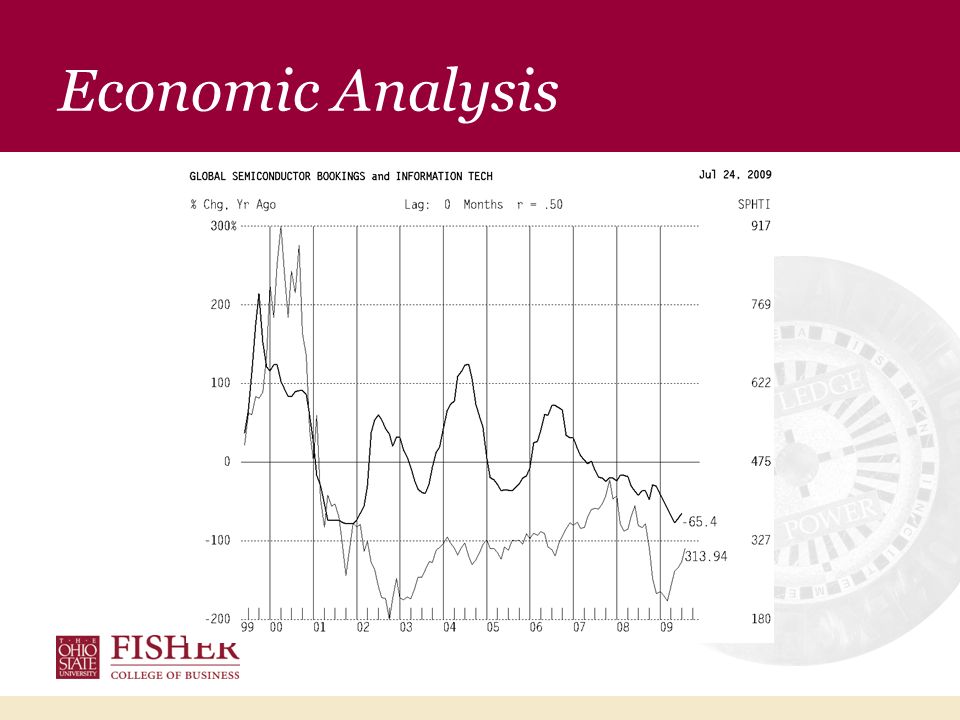

Economic Analysis Key facts about Info Tech sector –Over 75% of sales outside the U.S. for almost all major companies. –Leading Indicators Global Semiconductor Bookings Corporate IT Spending Index Change in Real Consumption (U.S.) –Consumer Confidence Index is a good gut check. –Data on leading indicators was available only up to June 09, which limited the predictive power of the analysis in the short term.

–Consumer Confidence Index is a good gut check. –Data on leading indicators was available only up to June 09, which limited the predictive power of the analysis in the short term..")

15

Economic Analysis -2.1 Is the rest of the World GDP lagging US GDP?

16

Economic Analysis 323.4

17

Economic Analysis

18

-73.7

19

Economic Analysis 49.3

20

Economic Analysis Summary Leading Indicators show that the sector may be overvalued based on the comparative analysis. If the assumption that ROW is going into a recession holds true then IT sector will be hurt. In the short term, –With a slowly recovering global economy, this sector may be a drag with no significant upside. –With the possibility of a double dip recession in the U.S. and slowing global economy, the sector has a significant downside. In the long run, –The sector is more attractive at a reasonable valuation.

21

Financial Analysis IT Sector Index over the past five years

22

Index price relative to S&P 500 The IT Index has been lagging relative to the S&P 500 the past couple years – recovering from tech bubble However this has changed so far this year, with the Index well outpacing the S&P 500 – will it continue? High: 12.3 Low: -19.4 Current: 12.3

23

EPS Analysis Year to year EPS increased until 2009 This latest year is the first one that saw a decrease in EPS for the last five year. High: 20.46 Low: 10.24 Median:16.41 Current: 17.71

24

Net Profit Relative to S&P 500 Profit has consistently been higher than the S&P 500 average Over the past couple of years this difference has jumped even higher

25

IT Sector Return on Equity High: 22.5% Low: 16.7% Median: 19.5% Current: 21.7% Has risen rather consistently over the past 5 year, with only a slight decrease this year

26

ROE Relative to S&P 500 The IT sector ROE has been relatively close to S&P 500 average, however this has changed since 2007

27

Financial Evaluation Summary Even though the IT sector has gone down in EPS, ROE and Net Profit Margins, it has still out performed the S&P 500 in these areas This outperformance is probably why the IT sector has gone up in price more than any other sector in the S&P 500 this year Have prices caught up with this performance, or will they continue to outpace the S&P 500?

28

High1.4 Low.98 Median1.3 Current1.1 Relative Price/Earnings

29

High1.7 Low1.2 Median1.4 Current1.7 Relative Price/Book

30

High2.1 Low1.5 Median1.7 Current2.1 Relative Price/Sales

31

Relative Price/Cash Flows High1.6 Low1.1 Median1.4 Current1.3

32

Absolute BasisHighLowMedianCurrent P/Trailing E31.511.122.317.2 P/Forward E23.912.120.317.5 P/B4.82.33.93.5 P/S3.01.32.51.9 P/CF17.78.014.511.3 Relative to SP500 HighLowMedianCurrent P/Trailing E1.6.911.31.1 P/Forward E1.4.981.31.1 P/B1.71.21.41.7 P/S2.11.51.72.1 P/CF1.61.11.41.3 Sector Valuation Summary

33

Valuation Summary On an absolute basis, the sector is inexpensive. Relative to the S&P500, the sector is a little expensive. The direction of the market will determine the sector’s future.

34

Recommendation Currently over-weighted in the SIM (1.76%) –Almost same as Industrials Best performing sector in the S&P for the year Will performance continue? Yes, world-wide growth will drive IT growth Yes, recovery will drive IT spending Yes, long-term growth of IT seems inevitable Yes, IT is becoming a business staple Yes, near-term IT spending is trending up No, economic analysis reveals that the sector may be overvalued. No, short-term run is ending based on P/S (which is above its median) Recommend weighting stands where it is.

Recommend weighting stands where it is..")

35

Appendix

36

EPS Growth Relative to S&P 500 IT Sector can have widely fluctuating EPS growth relative to the S&P 500

37

Net Profit Margin in IT Sector Saw large increase in 2007, however fell back down in 2008 and into 2009 High: 12.2% Low: 11.0% Median: 11.3% Current: 11.3%

38

Holdings Valuation Analysis StockAAPLHPQINTCMSFTNCRORCL P/Forward E Median 28.5 30.1 10.7 14.4 20.3 18.8 15.3 18.0 21.5 10.2 14.5 16.3 P/S Median 3.7 5.2 0.8 1.0 3.2 3.4 5.1 6.4 0.5 0.6 4.7 5.6 P/B Median 5.8 6.5 2.5 2.4 2.8 3.4 6.2 6.0 4.9 1.9 4.4 5.9 P/EBITDA Median 19.33 27.52 6.71 11.2 10.45 9.54 9.12 15.21 4.37 5.61 8.74 14.03 P/CF Median 26.1 34.6 7.6 11.2 12.8 11.6 11.8 18.0 5.4 6.7 12.1 16.3

39

Holdings Valuation Analysis StockAAPLHPQINTCMSFTNCRORCL P/Forward E Median 28.5 30.1 10.7 14.4 20.3 18.8 15.3 18.0 21.5 10.2 14.5 16.3 P/S Median 3.7 5.2 0.8 1.0 3.2 3.4 5.1 6.4 0.5 0.6 4.7 5.6 P/B Median 5.8 6.5 2.5 2.4 2.8 3.4 6.2 6.0 4.9 1.9 4.4 5.9 P/EBITDA Median 19.33 27.52 6.71 11.2 10.45 9.54 9.12 15.21 4.37 5.61 8.74 14.03 P/CF Median 26.1 34.6 7.6 11.2 12.8 11.6 11.8 18.0 5.4 6.7 12.1 16.3

40

Economic Analysis

43

-1.8

44

Absolute Forward Price/Earnings High23.9 Low12.1 Median20.3 Current18.0

45

Absolute Price/Book High4.8 Low2.3 Median3.9 Current3.6

46

Absolute Price/Sales High3.0 Low1.3 Median2.5 Current2.0

47

Absolute Price/Cash Flow High17.7 Low8.0 Median14.5 Current11.7

Similar presentations

Marc Reitter Siddhesh Sankulkar T E L E C O M S E C.>")