Download presentation

Presentation is loading. Please wait.

1

Chapter 5 - Supply

2

Section 1 – What is Supply?

Supply – the willingness and ability of producers to offer goods and services for sale Producer – anyone who provides goods or services Consumer – anyone who buys goods or services

3

Law of Supply As Prices Fall… Quantity As Supplied Prices falls Rise…

Rises.

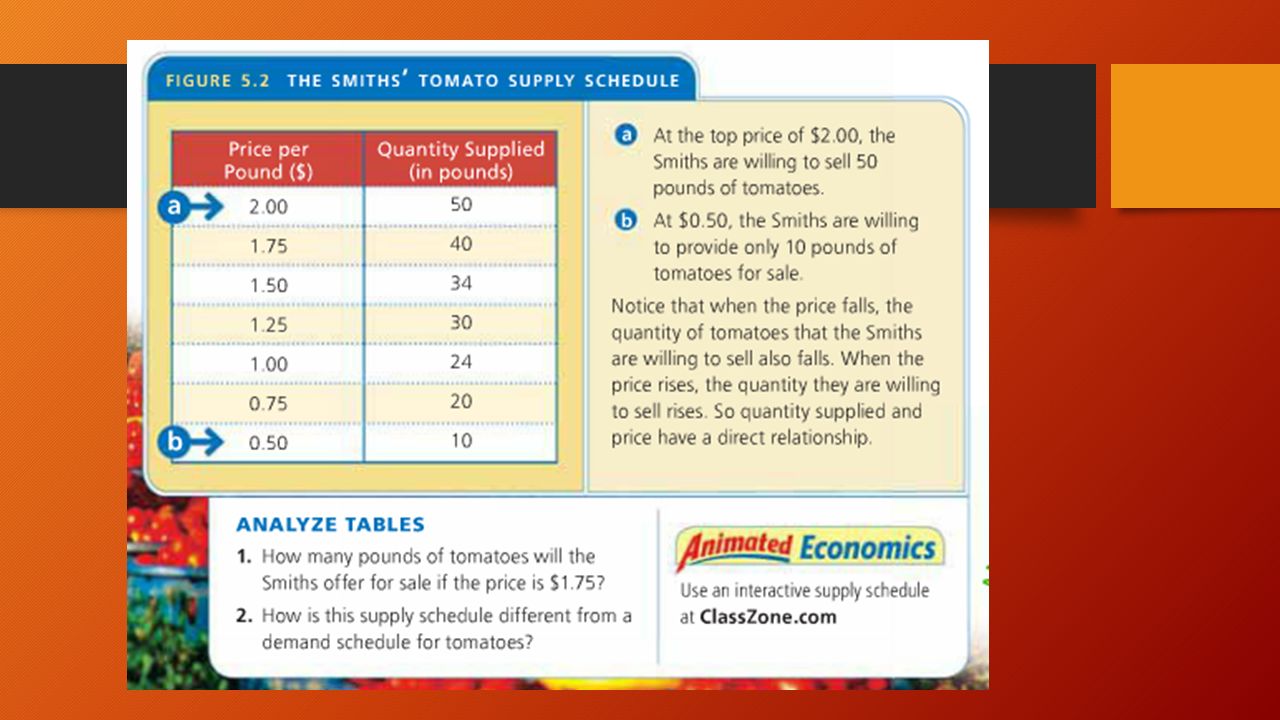

4

Supply Schedules Supply Schedule – list (table) how much of a good or service an individual producer is willing and able to offer for sale at each price Market Supply Schedule – lists (table) how much of a good or service all producers in a market are willing and able to offer for sale at each price

how much of a good or service an individual producer is willing and able to offer for sale at each price. Market Supply Schedule – lists (table) how much of a good or service all producers in a market are willing and able to offer for sale at each price.")

7

Create Your Own Supply Schedule

Imagine that you own a health food store that sells several brands of nutrition bars. Create a supply schedule showing how many bars you would be willing to sell each month at prices of $5, $4, $3, $2, and $1.

8

My Nutrition Bar Supply Schedule

Price Per Nutrition Bar Quantity Supplied $5.00 100 $4.00 80 $3.00 60 $2.00 40 $1.00 20 How does this table represent the law of supply?

9

Supply Curves Supply Curve/Market Supply Curve – shows the data from a supply schedule in a graph form

11

Create Your Own Supply Curve

Use data from your nutrition bars, now create a supply curve.

12

My Supply Curve

13

Section 2 – What are the Costs of Production?

Marginal Product – the change in total output brought about by adding one more worker Increasing Returns – occur when hiring new workers causes marginal product to increase Decreasing Returns – occur when hiring new workers causes marginal product to decrease

15

Production Costs Fixed Costs – those that business owners incur no matter how much they produce Variable Costs – depend on the level of production output Total Costs – the sum of fixed and variable costs Marginal Costs – the extra cost of producing one more unit

16

Why does it cost Janine more to produce 65 pairs of jeans with 11 workers than to produce 66 pairs of jeans with 9 workers?

17

Earning the Highest Profit

Marginal Revenue – the money made from the sale of each additional unit of output Total Revenue – a company’s income from selling its products Total Revenue = P x Q P is price of the product Q is quantity purchased at that price Profit-Maximizing Output – the level of production at which a business realizes the greatest amount of profit

19

Section 3 – What Factors Affect Supply?

Factors that Cause a Change in Supply Definition Input Costs The collective price of the resources that go into producing a good or service, affect supply directly Labor Productivity Better-trained or more-skilled workers are usually more productive. Increased productivity decreases costs and increases supply. Technology By applying scientific advances to the production process, producers have learned to generate their goods and services more efficiently. Government Action Taxes or subsidies, have a positive or negative effect on production costs Producer Expectations Amount of product producers are willing and able to supply may be influenced by whether they believe prices will go up or down Number of Producers Successful new product or service always brings out competitors who initially raise overall supply

20

What effects did BET’s success have on the supply of African-American programming?

21

Section 4 – What is Elasticity of Supply?

Elasticity of Supply – a measure of how responsive producers are to price changes in the marketplace Elastic Supply – supply could be increased as supply goes up because resources needed are neither particularly expensive nor hard to come by Inelastic Supply – supply could not be increased due to resources being expensive and hard to come by

23

What Affects Elasticity of Supply?

Changing production to respond to price change Industries that are able to respond quickly to changes in prices by either increasing or decreasing production are those that don’t require a lot of capital, skilled labor, or difficult-to-obtain resources Examples Quick Responders – Dog Walkers, craft makers Longer Responders – Automobile makers, oil refiners

Similar presentations

.>")