Download presentation

Presentation is loading. Please wait.

1

Amortization Unit 9

2

Amortization is the process of allocating to expense the cost of a capital asset over its useful (service) life in a rational and systematic manner. Cost allocation is designed to provide for the proper matching of expenses with revenues in accordance with the matching principle. During an asset’s life, its usefulness may decline because of wear and tear or obsolescence. Land is the only capital asset that is not amortized. AMORTIZATIONAMORTIZATION

3

FACTORS IN CALCULATING AMORTIZATION Illustration 10-6

4

AMORTIZATION METHODS Three methods of recognizing amortization are: 1. Straight-line, 2. Units of activity, and 3. Declining-balance. Each method is acceptable under generally accepted accounting principles. Management selects the method that is appropriate for their company. Once a method is chosen, it should be applied consistently.

5

STRAIGHT-LINE METHOD Amortization Expense Truck2,400 Accumulated Amortization – Truck2,400 To record amortization on truck in year 1

6

STRAIGHT-LINE METHOD Amortization is constant for each year of the asset's useful life

7

STRAIGHT-LINE METHOD EXAMPLE

8

DECLINING-BALANCE METHOD The calculation of periodic amortization is based on a declining net book value (cost less accumulated amortization) of the asset. The amortization rate remains constant from year to year, but the net book value to which the rate is applied declines each year. Net Book Value (at beginning of year) Straight-line Rate (x declining balance rate multiplier, if any) Amortization Expense Rate = (100/ life of asset) * 2

Straight-line Rate (x declining balance rate multiplier, if any) Amortization Expense Rate = (100/ life of asset) * 2.")

9

DECLINING-BALANCE METHOD Accelerated methods result in more amortization in early years and less in later years

10

DECLINING-BALANCE METHOD EXAMPLE

11

UNITS-OF-ACTIVITY METHOD To use the units-of-activity method, 1) the total units of activity for the entire useful life are estimated, 2) the amount is divided into amortizable cost to calculate the amortization cost per unit, and 3) the amortization cost per unit is then applied to the units of activity during the year to calculate the annual amortization. Amortized Cost Total Units of Activity Amortizable Cost per Unit Units of Activity during the Year Amortization Expense Amortizable Cost per Unit

12

UNITS-OF-ACTIVITY METHOD Useful life is expressed in terms of total units of production or activity expected from the asset

13

UNITS-OF-ACTIVITY METHOD EXAMPLE

14

COMPARISON OF METHODS

15

If annual amortization is inadequate or excessive, a change in the periodic amount should be made. When a change is made, 1. there is no correction of previously recorded amortization expense and 2. amortization expense for current and future years is revised. REVISING PERIODIC AMORTIZATION Revised amortization expense = Net book value at time of revision – revised salvage value Remaining useful life

16

AMORTIZATIONAMORTIZATION The units-of-activity method is generally used to calculate amortization on natural resources, because periodic amortization generally is a function of the units extracted during the year. NATURAL RESOURCES

17

ILLUSTRATION 10-23 FORMULA TO CALCULATE AMORTIZATION EXPENSE Amortizable Cost = (Cost – Residual Value + Restoration Costs) Total Estimated Units Amortization Cost per Unit Amortization Cost per Unit Number of Units Extracted and Sold Amortization Expense

Total Estimated Units Amortization Cost per Unit Amortization Cost per Unit Number of Units Extracted and Sold Amortization Expense")

18

ILLUSTRATION 10-24 STATEMENT PRESENTATION OF AMORTIZATION Accumulated Amortization, a contra asset account, is deducted from the cost of the natural resource in the balance sheet as follows:

19

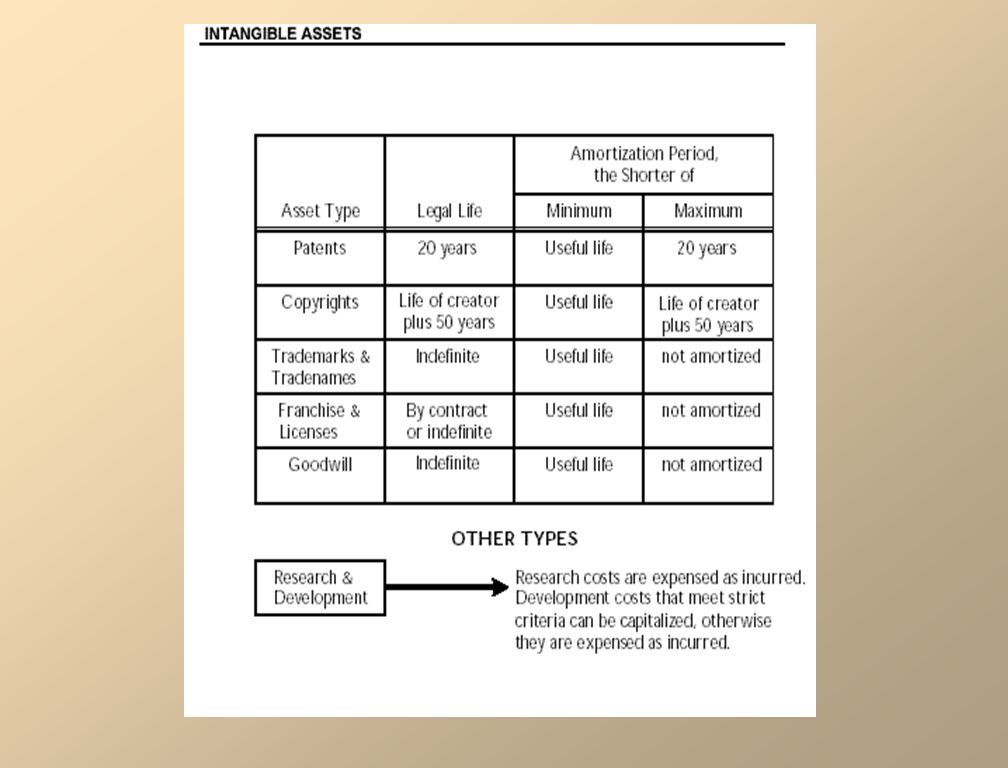

In general, accounting for intangible assets parallels the accounting for capital assets. Intangible assets are: 1. recorded at cost; 2. written off over useful life in a rational and systematic manner; 3. at disposal, net book value is eliminated and gain or loss, if any, is recorded. ACCOUNTING FOR INTANGIBLE ASSETS

20

Amortizable intangible assets Have defined lives Allocation of the cost to expense over the shorter of Useful (economic) life Legal life Straight-line method of amortization used AMORTIZATION OF INTANGIBLE ASSETS

life Legal life Straight-line method of amortization used AMORTIZATION OF INTANGIBLE ASSETS")

21

UNAMORTIZABLE INTANGIBLE ASSETS Indefinite useful lives Do not amortize Test for impairment

Similar presentations

CHAPTER 9.>")

. 7/11/02.>")