Download presentation

Presentation is loading. Please wait.

1

Petroleum Outlook 2002: On the Road to Pamplona John Cook Energy Information Administration NPRA Annual Meeting San Antonio, Texas March 18, 2002

2

Introduction Global Demand (How Much Oil Are We Using?) Global Supply –OPEC 10 vs. Iraq vs. non-OPEC Inventories: The Intersection of Demand and Supply –Implied Global Inventory Change –Observed OECD Inventories –U.S. Inventories WTI Price Outlook U.S. Gasoline Outlook U.S. Distillate Fuel Outlook U.S. Jet Fuel Outlook

3

Crude Price Cycles: Where is the Next Turn? Sources: History: EIA; Projections: Short-Term Energy Outlook, March 2002.

4

Crude Oil Prices Expected to Rise Through 2002 Sources: History: EIA; Projections: Short-Term Energy Outlook, March 2002.

5

Supply –Non-OPEC Supply –OPEC 10 Crude Oil Production Volumes –Iraq Retroactive Pricing UN Revisions to Oil-for-Food Program Upcoming Confrontation? –Nigeria –Venezuela Demand –Weather –Global Economic Recovery –Lingering Impacts from 9/11 When, Not If, Crude Oil Prices Will Reach $25 per barrel and higher Uncertainties

6

What Is Global Demand or Supply? Demand200020012002 PEL76.276.176.2 PIRA76.676.877.6 Argus76.3 76.6 Deutsche Bank76.075.976.5 Supply200020012002 PEL76.876.776.4 PIRA77.477.2 Argus76.676.474.9* Deutsche Bank76.8 77.2 * Assumes OPEC 10 production remains 1 MMBD below Dec. 2001 for all 2002.

7

WTI Crude Oil Price: Potential for Volatility Around Base Case Sources: History: EIA; Projections: Short-Term Energy Outlook, March 2002.

8

Annual World Oil Demand Growth 1991-2002 Sources: History: EIA; Projections: Short-Term Energy Outlook, March 2002.

9

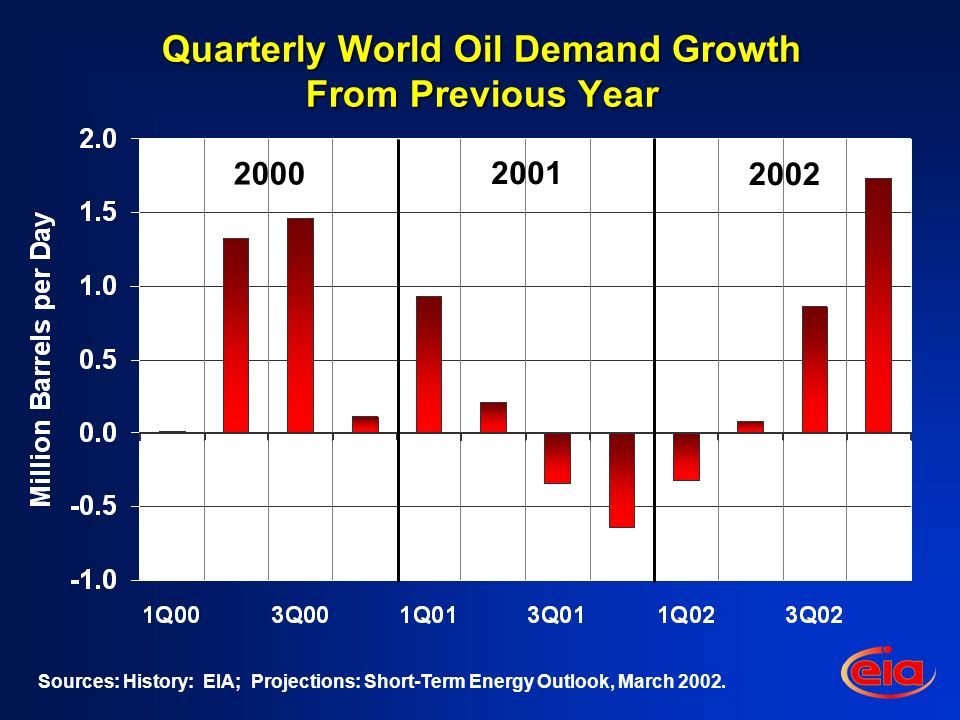

Quarterly World Oil Demand Growth From Previous Year Sources: History: EIA; Projections: Short-Term Energy Outlook, March 2002. 2000 2001 2002

10

Annual World Oil Demand Growth by Region, 1991-2002 * Other includes Australia, New Zealand, the Middle East, and Africa. Sources: History: EIA; Projections: Short-Term Energy Outlook, March 2002.

11

U.S. Petroleum Demand in 2 nd Half of 2002 Expected to be Higher than in 2001 Sources: History: EIA; Projections: Short-Term Energy Outlook, March 2002.

12

Distillate Fuel and Residual Fuel Demand vs. Spot Natural Gas Wellhead Price Sources: History: EIA; Projections: Short-Term Energy Outlook, March 2002.

13

Will OPEC Keep Production Down in 2002? History Projections Sources: History: EIA; Projections: Short-Term Energy Outlook, March 2002.

14

Changes in Demand and Supply from 1992 to 2002 * Other includes all non-OPEC supply and OPEC non-crude production. Sources: History: EIA; Projections: Short-Term Energy Outlook, March 2002. OPEC 10 Iraq Other Demand

15

EIA’s World Petroleum Balance Source: Energy Information Administration, March 2002.

16

Implied Global Stock Change From End-1999 Through End-2002 Source: Energy Information Administration, March 2002.

17

OPEC Discipline & Economic Recovery Tighten World Balance in 2002 *Total includes commercial and government stocks. Source: Energy Information Administration, March 2002.

18

Fundamentals Support Cycle Turning in 2002 Source: Energy Information Administration, March 2002; International Energy Agency.

19

U.S. Commercial Petroleum Inventories Built More Than In Other Regions in 2001 Source: International Energy Agency, Oil Market Report database, February 2002.

20

U.S. Crude Oil and Gasoline Market Cycles Sources: History: EIA; Projections: Short-Term Energy Outlook, March 2002.

21

The Cycle of Refinery Inputs, Inventory Balance, and Margins Crude Inputs High Stocks Low (Summer 2001) Crude Inputs Decreasing (Late Winter 2001/02) Product Stocks Increasing (Fall 2001) Refinery Margins Weakening (Early Winter 2001/02) Refinery Margins Increasing (Late Summer 2002) Excess Stocks Diminishing (Spring 2002)

Crude Inputs Decreasing (Late Winter 2001/02) Product Stocks Increasing (Fall 2001) Refinery Margins Weakening (Early Winter 2001/02) Refinery Margins Increasing (Late Summer 2002) Excess Stocks Diminishing (Spring 2002)")

22

Margins Have Begun Their Seasonal Climb Source: Reuters, EIA

23

Crude Oil Inputs Ended 2001 at “Normal” Levels; Dec. 2000 Was Unusually High Sources: History: EIA; Projections: Short-Term Energy Outlook, March 2002.

24

Gasoline Yields Much Higher Than Usual in 2002 Source: Reuters

25

Record Gasoline Production Likely Throughout 2002 Sources: History: EIA; Projections: Short-Term Energy Outlook, March 2002.

26

Finished Gasoline Net Imports This Spring/Summer Less Than 1 Year Ago Sources: History: EIA; Projections: Short-Term Energy Outlook, March 2002.

27

Gasoline Demand Growth Continues Sources: History: EIA; Projections: Short-Term Energy Outlook, March 2002.

28

With Precarious Balance, Higher Demand Would Rapidly Draw Stocks Sources: History: EIA; Projections: Short-Term Energy Outlook, March 2002.

29

Retail Motor Gasoline Prices Will Rise, But Should Remain Below Recent Summers * Regular self-service Sources: History: EIA; Projections: Short-Term Energy Outlook, March 2002.

30

U.S. Distillate Inventories Will Remain High Sources: History: EIA; Projections: Short-Term Energy Outlook, March 2002.

31

Jet Fuel Demand Recovering Slowly Sources: History: EIA; Projections: Short-Term Energy Outlook, March 2002, and September 2001.

32

Conclusions World oil prices are expected to continue upward through 2002 –Global economic recovery –OPEC output cuts –Declining inventories U.S. market conditions likely to vary by product –Gasoline supply balance will be tight, prices strong –Distillate and jet fuel supplies will be adequate However, there are a number of uncertainties –Speed of demand recovery –OPEC response to rising prices

Similar presentations