Download presentation

Presentation is loading. Please wait.

1

VALUATION OF CMOS

2

Introduction STATIC VALUATION DYNAMIC VALUATION MODELING Option-adjusted spread(OAS) Other products of the OAS models Illustration Plain vanilla structure A PAC/Supports structure A reverse pay structure

Other products of the OAS models Illustration Plain vanilla structure A PAC/Supports structure A reverse pay structure")

3

STATIC VALUATION Average life Static Spread refinancing rate fixed Zero volatility OAS

4

DYNAMIC VALUATION MODELING Option-adjusted spread(OAS) A measure of the yield spread that can be used to reconcile dollar differences between value and price using simulation to generate Monthly cash flows are path-dependent

A measure of the yield spread that can be used to reconcile dollar differences between value and price using simulation to generate Monthly cash flows are path-dependent")

5

SIMULATION Step 1 : generating many scenarios of future interest rate path

6

SIMULATION Step 2 : generating refinancing rate corresponding to the scenarios

7

SIMULATION Step 3: generating cash flow

8

SIMULATION Step 4 : generating spot rate

9

SIMULATION

10

INTERPRETATION OF OAS Be used to reconcile value with market price Be measuring the average spread over the Treasury spot rate cure , not the Treasury yield curve An average spread Option cost = Static spread – Option-adjusted spread

11

OPTION-ADJUSTED DURATION Measure the price sensitivity of a bond to a small change in interest rates. Duration= P - - P + / P 0 (y + -y - ) Effective duration Assume: parallel shift in the yield curve

Effective duration Assume: parallel shift in the yield curve.")

12

Increase in priceDecrease in price Positive convexityX%Less than X% Negative convexityX%More than X% OPTION-ADJUSTED CONVEXITY Convexity is the rate of change of the dollar duration of a security When the prevailing mortgage rate is much higher than the mortgage rate ---Positive convexity Effective convexity

13

Simulated Average Life Is the average of the average lives along the interest rate paths The greater the range and standard deviation of the average life, the more the uncertainty about the tranche ’ s average life

14

structure Plain Vanilla Structure

15

Base case (assumes 12% interest rate volatility) C is better--- high OAS but low option cost

C is better--- high OAS but low option cost")

16

Prepayment Slow--- OAS decrease, IO increase

17

Volatility Increase---longer tranches benefit more

18

PAC/Support Bond Structure Structure

19

Base case

20

prepayment

21

volatility

22

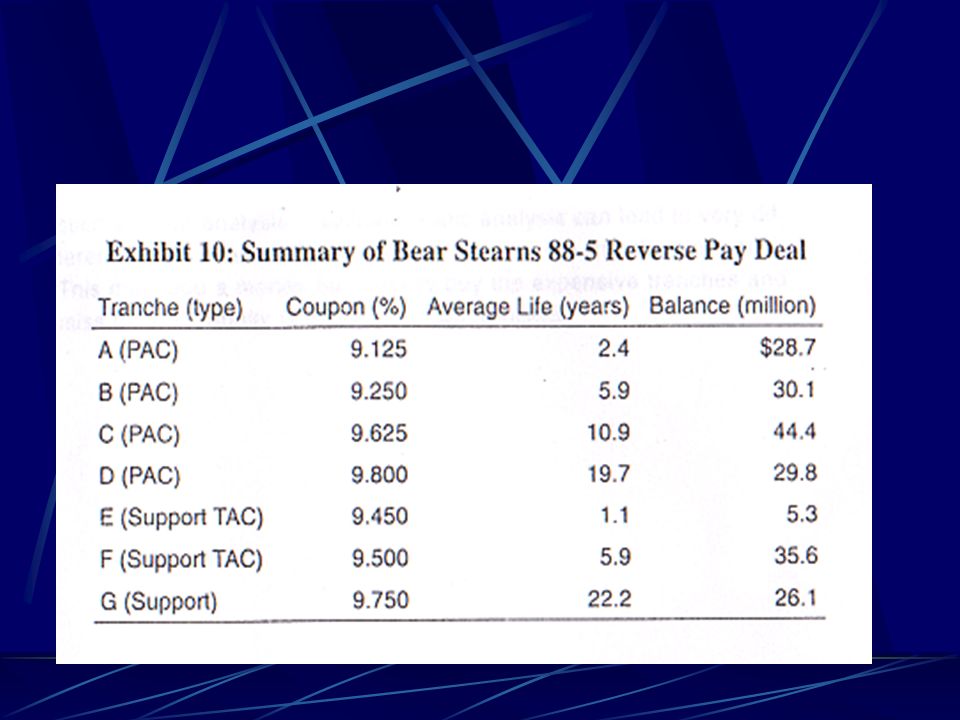

Reverse PAC Deal structure After support goes,can move prepayments down to last tranche, protect higher classes from contract risk

24

Average Life OA- Duration OA- Convexity PAC C10.96.3-0.22 PAC D19.75.90.04

25

THE END

Similar presentations

slope increases (long term R increases more than short term or short term even decreases) buy notes sell bonds.>")

Factors Prepayment Weighted average coupon (WAC) ◦ The monthly payment derived from.>")