Download presentation

Presentation is loading. Please wait.

1

BBA, MBA (Finance), London

Topic # 04 Corporate Finance Corporate Bonds & It's Valuation Zulfiqar Hasan BBA, MBA (Finance), London Associate Professor

, London. Associate Professor.")

2

Contents Bonds-its definition and types, Value a straight bond and a zero-coupon bond using present discounted value techniques; relationship between interest rates and bond prices; Determine the yield to maturity for a straight bond; relationships between zero coupon bonds and coupon bonds; Analyze bond price dynamics and predict how bond prices respond to changes in interest rates; Explain why coupon bonds and zero coupon bonds react differently to changes in interest rates; Explain the relationship between real and nominal interest rates

3

Bonds are sometimes called fixed income securities.

What is a Bond? A bond is a legally binding agreement between a borrower and a lender A bond is a debt instrument issued for a period of more than one year with the purpose of raising capital by borrowing. A bond is a security that obligates the issuer to make specified interest and principal payments to the holder on specified dates. Bonds are sometimes called fixed income securities. A Bond is an instrument which pays fixed amounts (usually) of interest (called a coupon) on a regular basis, over its life and is redeemed at par value (usually) at maturity, by the issuer .

of interest (called a coupon) on a regular basis, over its life and is redeemed at par value (usually) at maturity, by the issuer .")

4

Corporate Bonds Corporate bonds are debt instruments because money is lent to a corporation. In taking money, the corporation issuing the bond promises interest (also called "coupon"). Corporate bonds, issued by a Corporation, are meant to raise the funds for the company’s expansion plans. In Bangladesh, we have no separate bond market. But corporate bonds are traded through Stock exchange and by other financial organization. Bond available in the stock exchange are: Islami Bank Bangladesh Limited Perpetual Mudarabah Bond ACI Zero Coupon Bond BRAC Bank Zero Coupon Bond

. Corporate bonds, issued by a Corporation, are meant to raise the funds for the company’s expansion plans. In Bangladesh, we have no separate bond market. But corporate bonds are traded through Stock exchange and by other financial organization. Bond available in the stock exchange are: Islami Bank Bangladesh Limited Perpetual Mudarabah Bond. ACI Zero Coupon Bond. BRAC Bank Zero Coupon Bond.")

5

Why Corporations issue bonds?

The basic reasons are: Raise capital for their business for investments Long-Term Financing Avoid long-term financing from banks Efficiency of management Lower interest payments No Dilution of Stockholder's Equity Call options by the company Convertibility options by the company

6

Advantages of Corporate Bond

Offer higher interest: Corporate bonds generally offer higher interest rate when compared to government bonds as investors run a huge risk in case of company issuing the bonds going default on payments. Steady income to investors Corporate bonds provide steady income to investors in the form of coupons / interest rate. Purchasing Opportunity any Time: There are many corporate bonds in the market at any point of time, giving the investors a chance to opt for bonds from different sectors. Selling Opportunity any Time Corporate bonds have a huge secondary market so investors can sell them to others at higher prices, especially if the company issuing the bond has a good credibility and credit ratings.

7

Disadvantages of Corporate Bonds

Corporate bonds, when compared to government bonds, are more risky as the corporate issuing the bond may default on payments. If a corporate issues a bond that is callable i.e. the bond that can be purchased back by the company issuing it after a particular time period, then the company might re-purchase those bonds from the investors in case the interest rates decline so that it could release new bonds which will provide low interest rate. So in case the bond investors buy is callable, the investors must ensure that they are compensated appropriately. Moreover, if the corporate issuing the bond issues more such bonds in the market, their price would decrease affecting the interests of the investors. In case of inflation, the prices of the bond may decrease again adversely affecting the investors. Changes in taxation policies also affect the benefits from the corporate bonds.

8

Basics Features of Bond…

Par or Face Value: The par or face value of a bond is the amount of money that is paid to the bondholders at maturity. Coupon Interest Rates: The stated annual rate of interest paid on a bond. Coupon Payment: The coupon payments represent the periodic interest payments from the bond issuer to the bondholder. Maturity Date: The maturity date represents the date on which the bond matures, i.e. the date on which the face value is repaid. The last coupon payment is also paid on the maturity date.

9

…… Basics Features of Bond

Original Maturity: The time remaining until the maturity date when the bond was issued. Call Provision: A provision in a bond contract that gives the issuer the right to “recall” the bond and pay it off under specified terms prior to the stated maturity date. Indenture: A legal document contains the details of the bond issue called the indenture.

10

Types of Corporate Bond

SL Basis of Types Types 01 Interest Coupon Bond Zero Coupon Bond 02 Security Secured Bond Unsecured Bond 03 Control (Ownership) Government Bond Private Bond Foreign Bond 04 Maturity Fixed Maturity Bond Perpetual Bond 05 Location Domestic Bond International Bond 06 Performance Blue Chip Bond Junk Bond 07 Convertibility Convertible Bond Non-Convertible Bond 08 Callability Callable Bond Un-callable Bond

Government Bond. Private Bond. Foreign Bond. 04. Maturity. Fixed Maturity Bond. Perpetual Bond. 05. Location. Domestic Bond. International Bond. 06. Performance. Blue Chip Bond. Junk Bond. 07. Convertibility. Convertible Bond. Non-Convertible Bond. 08. Callability. Callable Bond. Un-callable Bond.")

11

Bond Ratings Bond Rating is a grade given to bonds that indicates their credit quality. Private independent rating services such as Standard & Poor's, Moody's and Fitch provide these evaluations of a bond issuer's financial strength, or its the ability to pay a bond's principal and interest in a timely fashion. 13 13

12

How to Read Bond Tables? Column 1: Issuer - This is the company, state or country that is issuing the bond. Column 2: Coupon - The coupon refers to the fixed interest rate that the issuer pays to the lender. Column 3: Maturity Date - This is the date on which the borrower will repay the investors their principal. Typically, only the last two digits of the year are quoted: 25 means 2025, 04 is 2004, etc . Column 4: Bid Price - This is the price someone is willing to pay for the bond. It is quoted in relation to 100, no matter what the par value is. Think of the bid price as a percentage: a bond with a bid of 93 is trading at 93% of its par value. Column 5: Yield - The yield indicates annual return until the bond matures. Usually, this is the yield to maturity, not current yield. If the bond is callable it will have a "c--" where the "--" is the year the bond can be called. For example, c10 means the bond can be called as early as 2010.

13

Valuing Pure Discount or Zero-Coupon Bond

For Calculating Value of zero-Coupon Bond, please use PV formula only Example 01: Pure Discount Bond What is the present value of a 10-year, pure discount bond paying $1000 at maturity if the appropriate interest rate is: a. 5 percent b.10 percent c. 15 percent

14

Level-Coupon Bonds Formula

F = M = Face Value or Par Value of Bond C = INT = coupon payment; m = Number of periods in a year n=T = maturity period (number of Year) i = r = required or market rate of return

i = r = required or market rate of return.")

15

Example 01: Calculating the Interest Rates and Payments

A company issues a $300000, 10%, 20-year bond. The tax rate is 40%. What is the after-tax semiannual interest amount? Practice 01: A company issues a $500000, 12%, 20-year bond. The tax rate is 35%. What is the after-tax quarterly interest amount?

16

Example 02: Bond Issuance

A company issues a $300000, 16%, 10-year bond at 108. What is the maturity value? What is the annual cash interest payment? What are the proceeds the company receives upon the issuance of the bond? What is the amount of the premium? What is the annual premium amortization? A. Tk 300,000 B. C. D. E. Practice 02: A company issues a $300000, 16%, 10-year bond at 108. What is the maturity value? What is the annual cash interest payment? What are the proceeds the company receives upon the issuance of the bond? What is the amount of the premium? What is the annual premium amortization?

17

Example 02: Bond price or Current Value

A bond has a coupon interest rate of 10% per year, a $1,000 par value, and 3 years remaining until maturity. The market rate of interest for this bond is 9%. If interest is paid annually, what is the current value of the bond?

18

Example 03: Level-Coupon Bond multi periods

Find the present value (as of January 1, 2005), of a 63/8% coupon T-bond with semi-annual payments, and a maturity date of December 2010 if the YTM is 5%. C =( $1000x 63/8%) =$ 63.75

, of a 63/8% coupon T-bond with semi-annual payments, and a maturity date of December 2010 if the YTM is 5%. C =( $1000x 63/8%) =$")

19

Practice 01: Multi-period Discount Bond

A bond has a coupon interest rate of 10% per year, a $1,000 par value, and 3 years remaining until maturity. The market rate of interest for this bond is 8%. If interest is paid semi-annually, what is the current value of the bond? $1,052.41

20

Practice 02: Bond Price Movement

Miller Corporation has a premium bond making semiannual payments and 8% coupon, has a YTM of 6%, and has 13 years to maturity. The Modigliani Company has a discount bond making semiannual payments. This bond pays a 6% coupon, has a YTM of 8%, and also has 13 years to maturity. If interest rates remain unchanged what do you expect the price of these bonds to be 1 year from now? In 3 years? In 8 years? In 12 years? In 13 years? What’s going on here? Illustrate your answers by graphing bond prices versus maturity. PV0 PV1 PV2 PV3 PV4 PV5 PV6 PV7 PV8 PV9 PV10 PV11 PV12 PV13

21

Solution Practice 02: Bond Price Movement

Try to determine the maturity period (n)….. PV0 PV1 PV2 PV3 PV4 PV5 PV6 PV7 PV8 PV9 PV10 PV11 PV12 PV13 Miller Corporation bond: P0 = $40(PVIFA3%,26) + $1,000(PVIF3%,26) = $1,178.77 P1= $40(PVIFA3%,24) + $1,000(PVIF3%,24) = $1,169.36 P3 = $40(PVIFA3%,20) + $1,000(PVIF3%,20) = $1,148.77 P8 = $40(PVIFA3%,10) + $1,000(PVIF3%,10) = $1,085.30 P12 = $40(PVIFA3%,2) + $1,000(PVIF3%,2) = $1,019.13 P13 = $1,000 Modigliani Company bond: P0 = $30(PVIFA4%,26) + $1,000(PVIF4%,26) = $840.17 P1= $30(PVIFA4%,24) + $1,000(PVIF4%,24) = $847.53 P3= $30(PVIFA4%,20) + $1,000(PVIF4%,20) = $864.10 P8= $30(PVIFA4%,10) + $1,000(PVIF4%,10) = $918.89 P12 = $30(PVIFA4%,2) + $1,000(PVIF4%,2) = $981.14 P13 = $1,000

….. PV0 PV1 PV2 PV3 PV4 PV5 PV6 PV7 PV8 PV9 PV10 PV11 PV12 PV Miller Corporation bond: P0 = $40(PVIFA3%,26) + $1,000(PVIF3%,26) = $1, P1= $40(PVIFA3%,24) + $1,000(PVIF3%,24) = $1, P3 = $40(PVIFA3%,20) + $1,000(PVIF3%,20) = $1, P8 = $40(PVIFA3%,10) + $1,000(PVIF3%,10) = $1, P12 = $40(PVIFA3%,2) + $1,000(PVIF3%,2) = $1, P13 = $1,000. Modigliani Company bond: P0 = $30(PVIFA4%,26) + $1,000(PVIF4%,26) = $ P1= $30(PVIFA4%,24) + $1,000(PVIF4%,24) = $ P3= $30(PVIFA4%,20) + $1,000(PVIF4%,20) = $ P8= $30(PVIFA4%,10) + $1,000(PVIF4%,10) = $ P12 = $30(PVIFA4%,2) + $1,000(PVIF4%,2) = $ P13 = $1,000.")

22

Solution Practice 02: Graphical Presentation

23

Practice 02: Multi-period Discount Bond

Microhard has issued a bond with the following characteristics: Principal: $1000 Time to maturity: 20 years Coupon rate: 8 percent, Payments: semiannually Calculate the price of this bond if the stated annual interest rate is: a.8 percent b.10 percent c.6 percent a. $ b. $ c. $

24

Practice 03 & 04: Multi period Discount Bond Practice

What is the market price of a U.S. Treasury bond that has a coupon rate of 9%, a face value of $1,000 and matures exactly 10 years from today if the required yield to maturity is 10% compounded semiannually? $937.69 Assuming that the Mills Company Bond pays semiannually coupon interest 10%. The required stated annual return is 12% for similar-risk bonds. What is the value of this Bond if it has 10 years to maturity? $885.50

25

Example 04: Amount Change in Bond Value

A bond has a coupon interest rate of 10% per year paid annually, a $1,000 par value, and 3 years remaining until maturity. The market rate of interest for this bond is 8%. Now, suppose the market rate suddenly changes to 9%. What is the amount change in the bond's value? A. -$ B. $ C. $ D. $33.67 A. -$26.18 Amount Change = New Value – Old Value Practice 05: A bond has a coupon interest rate of 10% per year paid annually, a $1,000 par value, and 3 years remaining until maturity. The market rate of interest for this bond is 8%. Now, suppose the market rate suddenly changes to 7%. What is the amount change in the bond's value? A. $ B. -$ C. $ D. $28.33

26

Example 05: Percentage Change in the Bond's Value

A bond has a coupon interest rate of 10% per year paid annually, a $1,000 par value, and 3 years remaining until maturity. The market rate of interest for this bond is 8%. Now, suppose the market rate suddenly changes to 9%. What is the percentage change in the bond's value? A % B % C % D % C % Percentage Change = (New Value – Old Value)/Old Value Practice 06: A bond has a coupon interest rate of 10% per year paid annually, a $1,000 par value, and 3 years remaining until maturity. The market rate of interest for this bond is 8%. Now, suppose the market rate suddenly changes to 7%. What is the percentage change in the bond's value? A % B % C % D %

/Old Value. Practice 06: A bond has a coupon interest rate of 10% per year paid annually, a $1,000 par value, and 3 years remaining until maturity. The market rate of interest for this bond is 8%. Now, suppose the market rate suddenly changes to 7%. What is the percentage change in the bond s value A % B % C % D %")

27

Zero-Coupon and Coupon Bond

A bond has a coupon interest rate of 10% per year paid annually, a $1,000 par value, 30 years remaining until maturity, and a market rate of interest of 8%. Bond B is like Bond A is all respects except that Bond B does not pay interest. What is Bond B's value? A. $ B. $ C. $1, D. $1,225.18 $99.40

28

Duration: A Definition

Duration is the average time to maturity of the bond i.e. the average time after which the cash flows on the bond will be received. Duration is defined as a weighted average of the maturities of the individual payments: This definition of duration is sometimes also referred to as Macaulay Duration. The duration of a zero coupon bond is equal to its maturity. For a zero-coupon bond we have: However, the value B of a zero-coupon bond is: Substituting gives immediately the result that D=n. 26 26

29

Find out the duration of this bond.

Problem 01. Duration A bond with a YTM of 8% and a 10% coupon to be redeemed at par after 3 years. Present value: PV= 10/ (1.08) / (1.08) / (1.08) 3 = Duration: 9.26 x x x 3 105.13 = years = A bond with a YTM of 10% and a 10% coupon to be redeemed at par ($100) after 3 years. Find out the duration of this bond.

+ 10/ (1.08) / (1.08) = Duration: 9.26 x x x = 2.74 years. = A bond with a YTM of 10% and a 10% coupon to be redeemed at par ($100) after 3 years. Find out the duration of this bond.")

30

The duration of the bond with the lower coupon is higher. Why?

Calculating Duration Calculate the duration of a $1000 par value with 6% coupon 5-year bond if i = 8%: Time Payment PV(Payment) % of PV Time*%PV 1 60 55.56 6.04% 0.06 2 60 51.44 5.59% 0.11 3 60 47.63 5.18% 0.16 4 60 44.10 4.79% 0.19 5 1060 721.42 78.40% 3.92 920.15 100.00% 4.44 Calculate the duration of the 10% 5-year bond if i =8% Time Payment PV(Payment) % of PV Time*%PV 1 100 92.59 8.57% 0.09 2 85.73 7.94% 0.16 3 79.38 7.35% 0.22 4 73.50 6.81% 0.27 5 1100 748.64 69.33% 3.47 100.00% 4.20 The duration of the bond with the lower coupon is higher. Why? 27 27

% of PV. Time*%PV % % % % % % Calculate the duration of the 10% 5-year bond if i =8% Time. Payment. PV(Payment) % of PV. Time*%PV % % % % % % The duration of the bond with the lower coupon is higher. Why")

31

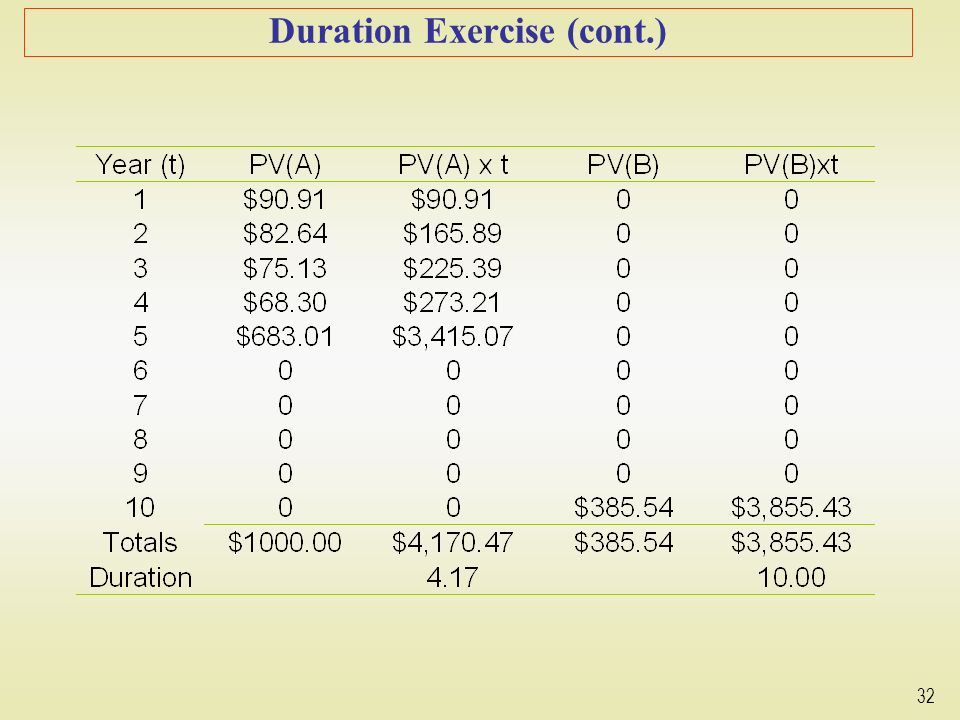

Duration: An Exercise What is the interest rate sensitivity of the following two bonds. Assume coupons are paid annually. Bond A Bond B Coupon rate % % Face value $1, $1,000 Maturity years years YTM % % Price $1, $385.54 28 28

32

Duration Exercise (cont.)

29 29

33

Duration Exercise (cont.)

Percentage change in bond price for a small increase in the interest rate: Pct. Change = - [1/(1.10)][4.17] = % Bond A Pct. Change = - [1/(1.10)][10.00] = % Bond B 30 30

][4.17] = % Bond A. Pct. Change = - [1/(1.10)][10.00] = % Bond B")

34

Current Yield It is the annual interest payment on a bond divided by its current market value. A bond has a coupon interest rate of 10% per year, a $1,000 par value, and 3 years remaining until maturity. The market rate of interest for this bond is 9%. If interest is paid annually, what is the current Yield of the bond?

35

Approximate Yield to Maturity (YTM/Kd/IRR)

It is the average rate of return earned on a bond if it is held to maturity. It is what rate of interest would you earn on your investment if you bought the bond and held it to maturity

36

Finding the YTM A bond has a coupon interest rate of 15% per year, a $1,000 par value, and 14 years remaining until maturity. The current value of this bond is $ What is the approximate YTM of the bond?

37

Solve this! The Seven Company’s bonds have four years remaining to maturity. Interest is paid annually, the bonds have a $1000 par value, and the coupon interest rate is 9 percent. Compute the Approximate yield to maturity for the bonds if the current market price is $829. YTM at $829 is 15% A bond has a coupon interest rate of 10% per year paid annually, a $1,000 par value, 20 years remaining until maturity, and a current value of $ What is the yield-to-maturity? 12%

38

Bond prices and market interest rates

Bond prices and market interest rates move in opposite directions. 2. When coupon rate = YTM, price = par value. When coupon rate > YTM, price > par value (premium bond) When coupon rate < YTM, price < par value (discount bond) A bond with longer maturity has higher relative (%) price change than one with shorter maturity when interest rate (YTM) changes. All other features are identical. A lower coupon bond has a higher relative price change than a higher coupon bond when YTM changes. All other features are identical.

When coupon rate < YTM, price < par value (discount bond) A bond with longer maturity has higher relative (%) price change than one with shorter maturity when interest rate (YTM) changes. All other features are identical. 4. A lower coupon bond has a higher relative price change than a higher coupon bond when YTM changes. All other features are identical.")

39

Practice: Selling at Discount, Premium or Par Value

Lahey Industries has outstanding a $1000 par value bond with an 8% coupon interest rate. The bond has 12 years remaining to its maturity date. If interest is paid annually, find the value of the bond when the required return is 7%, 8% and 10%. Indicate for each case in part a whether the bond is selling at a discount, at a premium, or at its par value. Using the 10% required return, find the bond’s value when interest is paid semiannually. Results: 01. $ , $1000, $863.73 02. Sells at premium, par value, Discount 03. $862.01

40

Bond Investment Strategies

A passive strategy is a strategy in which investors establish a diversified portfolio of bonds and maintain the portfolio for a long period of time. A matching strategy is a strategy in which investors estimate future cash outflows and choose bonds whose coupon or principal payments will cover the projected cash outflows. A laddered strategy is a strategy in which investors evenly allocate funds invested in bonds in each of several different maturity classes to minimize interest rate sensitivity. A barbell strategy is a strategy in which investors allocate funds into bonds with short-term and long-term, but few or no intermediate-term maturities. An interest rate strategy is a strategy in which investors allocate funds to capitalize on interest rate forecasts and revise their portfolio in response to changes in interest rate expectations.

41

The Term Structure of Interest Rates

Interest rates for bonds vary by term to maturity, among other factors The yield curve provides describes the yield differential among treasury issues of differing maturities Thus, the yield curve can be useful in determining the required rates of return for loans of varying maturity

42

Bond Risks: Price Risks

Bond Options Convertible Bond: may be exchanged for common stock in the company that issued the bond Exchangeable Bond: may be exchanged for shares in another firm Bond Risks: Price Risks Default risk: the possibility that the issuer of the bond is unable to pay rated by agencies like Moody’s and Standard & Poor’s Interest rate risk: the chance of loss due to changing interest rates Call risk - the possibility that the company will exercise a bond’s call feature Reinvestment rate risk - the chance that the interest received cannot be reinvested to earn as much as the bond’s original yield to maturity; the higher the coupon on a bond, the higher its reinvestment rate risk Marketability risk - the difficulty of selling a bond in the secondary market

43

Thank You Very Much for your Cooperations !!!

Similar presentations