Download presentation

Presentation is loading. Please wait.

1

11B Investing Basics and Evaluating Bonds #2

Recall the concept of asset allocation 11-1

2

One Effect of Asset Allocation: A Weighted Total Return

3

Ultraconservative “Investors” Are Really Just “Savers”

People who invest very conservatively They do not get ahead financially over the long term because taxes and inflation offset most of their interest earnings Remember “The Rule of 72”? 72/4% = 18 years 72/8% = 9 years (money doubles much faster)

")

4

Identify the Types of Investments You Want to Make

Do You Want to Lend Your Money or Own an Asset? Debts – “loanership” (lending) investments. Fixed Maturity – the borrower agrees to repay the principal to the investor on a specific date. Fixed Income – the borrower agrees to pay the investor a specific rate of return for use of the principal. Equities – “ownership” investments. Potential for a higher return by sharing in profits

investments. Fixed Maturity – the borrower agrees to repay the principal to the investor on a specific date. Fixed Income – the borrower agrees to pay the investor a specific rate of return for use of the principal. Equities – ownership investments. Potential for a higher return by sharing in profits.")

5

The Risk Pyramid Reveals the Trade-offs Between Investment Risk and Return

6

Inflation To beat inflation, one must invest money so that it earns a higher after-tax return than the inflation rate Real Rate of Return – the return after subtracting the effects of both inflation and income taxes. Example: 10% return, 7.5% after taxes (25% tax bracket), 4% inflation, real rate of return of 3.5% after taxes and inflation

, 4% inflation, real rate of return of 3.5% after taxes and inflation.")

7

Objective 5 Recognize Why Investors Purchase Corporate Bonds

A corporation’s written pledge to repay a specified amount of money with interest An interest-only loan Considered safer than co. stocks A “fixed-income” security A form of debt financing (bond owners repaid in future) 11-7

")

8

Corporate Bonds Face Value Coupon rate

Dollar amount bondholder receives at bond’s maturity date Usually $1,000 Coupon rate Stated interest rate Interest payments made every six months Example: $1,000 x 5.8% = $58 (in two $29 payments) Maturity Date = date on which face value repaid; generally 1 to 30 years 11-8

Maturity Date = date on which face value repaid; generally 1 to 30 years")

9

Corporate Bonds Bond Indenture Trustee

Legal document describing conditions of the bond issue Trustee Financially independent firm that acts as the bondholder’s representative Usually a commercial bank or other financial institution 11-9

10

Why Corporations Sell Bonds

To raise funds for major purchases To fund ongoing business activities When difficult or impossible to sell stock To improve financial leverage Interest paid to bondholders is tax- deductible for the firm 11-10

11

Types of Corporate Bonds

Debenture Unsecured debt Investors become “creditors” if company fails Backed only by the reputation of the issuing company; most corporate bonds are this type Mortgage Bond Secured by various assets of the issuing firm, such as real estate and property Lower interest (coupon) rate since debt is secured 11-11

rate since debt is secured")

12

Types of Corporate Bonds

Convertible Bond Can be exchanged, at the owner’s option, for a specified number of shares of the corporation’s common stock Generally, coupon rate on a convertible bond is 1% to 2% lower than the rate paid on traditional bonds Would only want to convert when stock price gets higher than the bond’s equivalent value in stock 11-12

13

Provisions For Repayment

Call Feature of Bonds Corporation can “call in” or buy back outstanding bonds before the maturity date Most corporate bonds are callable Call-protected for first 5 to 10 years after issue A firm calls a bond issue if the coupon rate they are paying is much higher than the market rate Like consumers refinancing to lower-rate mortgage What is the effect of called back bonds on investors? 11-13

14

Provisions For Repayment

Sinking Fund Corporations deposit money annually Trustee uses the money to retire the bond issue prior to maturity Serial Bonds Bonds of a single issue that mature on different dates Example: After first 10 years, over the next 10 years, 10% of bonds mature each year Bond 11-14

15

Why Investors Purchase Corporate Bonds

Interest Income - “Fixed Income” Registered Bond- tracked electronically Coupon and principal paid to registered owner (check or direct deposit) Registered Coupon Bond Registered for principal only Coupon must be presented to obtain payment Zero-Coupon Bond Pays no interest Sold at a discount from face value Redeemed at face value at maturity Bond 11-15

Registered Coupon Bond. Registered for principal only. Coupon must be presented to obtain payment. Zero-Coupon Bond. Pays no interest. Sold at a discount from face value. Redeemed at face value at maturity. Bond")

16

Why Investors Purchase Corporate Bonds

Dollar Appreciation of Bond Value Bond values change with market interest rates Bond value vs. Interest rates = inverse relationship If Market rate< Coupon rate Price > Face value If Market rate > Coupon rate ← Price < Face value Bond values change with the financial condition of the issuing company or government unit Bond Repayment at Maturity Face value repaid on maturity date (will be worth less due to inflation) Bondholders may keep till maturity or sell Portfolio diversification beyond stock and cash assets 11-16

Bondholders may keep till maturity or sell. Portfolio diversification beyond stock and cash assets")

17

Approximate Bond Value Formula

5.875% interest on ($1,000 bond) = $58.75 New issues paying 5% (decrease in coupon rate) Dollar amount of interest $58.75 Comparable interest rate = 5% (.05) = $1,175 Bond worth more than face value because it pays interest rate higher than current market rate New issues paying 6.5% (increase in coupon rate) Comparable interest rate = % (.065) = $903.85 Bond worth less than face value because it pays interest rate lower than current market rate

= $ New issues paying 5% (decrease in coupon rate) Dollar amount of interest $ Comparable interest rate = 5% (.05) = $1,175. Bond worth more than face value because it pays interest rate higher than current market rate. New issues paying 6.5% (increase in coupon rate) Comparable interest rate = 6.5% (.065) = $ Bond worth less than face value because it pays interest rate lower than current market rate.")

18

Premiums and Discounts

When a bond is first issued, it is sold in one of three ways: at its face value at a discount below its face value or at a premium above its face value.

19

Price Changes for Bonds

What does this graph tell you?

20

Objective 6 Evaluate Bonds When Making an Investment

Sources of Information – The Internet The issuing firm’s website Financial coverage of bond transactions Wall Street Journal, Barrons, Internet Other Sources of Information Business Periodicals Federal Agencies 11-20

21

Corporate Bond Quotes The first bond in the list: Matures in 2036

Current price = 93.51% of par (discount) = $935.10 Pays an annual coupon rate of 5.875% = $58.75 Yield-to-Maturity = 6.365% (considers bond maturity date) Current yield = % = 5.875/93.51 (interest/price) Or see Exhibit 11-6 11-21 21

= $ Pays an annual coupon rate of 5.875% = $ Yield-to-Maturity = 6.365% (considers bond maturity date) Current yield = 6.283% = 5.875/93.51 (interest/price) Or see Exhibit")

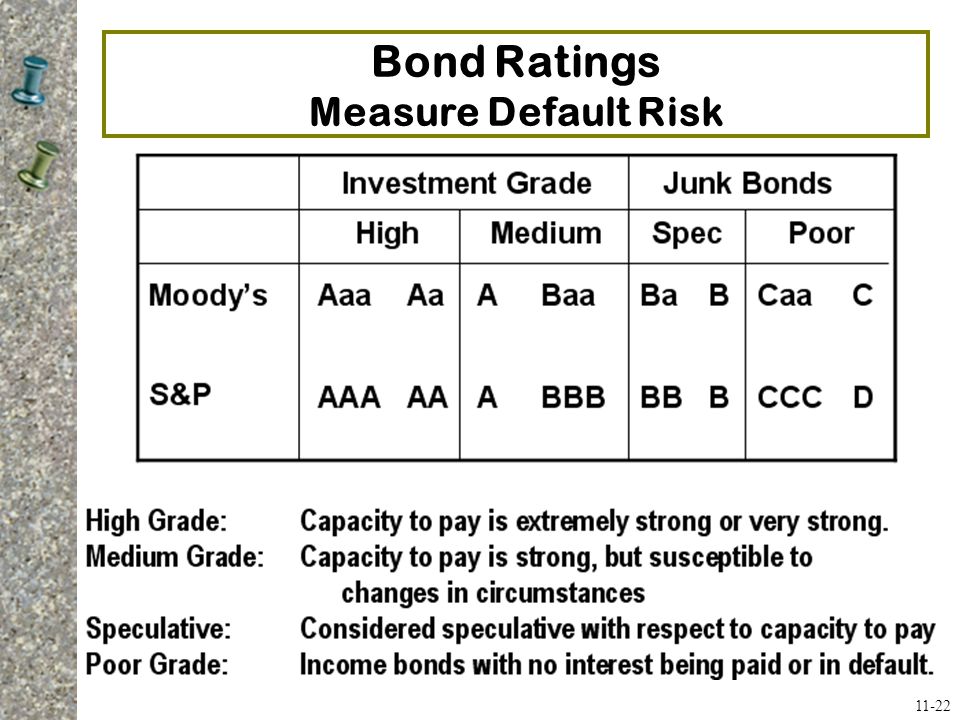

22

Bond Ratings Measure Default Risk

11-22

23

Decisions Bond Investors Must Make

Decide on risk level. Investment grade bonds: top 4 grades (BBB, A, AA, AAA) Junk bonds (a.k.a., high yield bonds): lower rated and higher risk Decide on maturity. Match to financial goals Determine the after-tax return. Taxable versus tax-exempt

Junk bonds (a.k.a., high yield bonds): lower rated and higher risk. Decide on maturity. Match to financial goals. Determine the after-tax return. Taxable versus tax-exempt.")

24

Wrap Up Chapter Quiz Concept Check Calculate Semi- annual Interest and Reasons That Investors Buy Bonds Concept Check Current Value of Bonds; Explain Bond Ratings

Similar presentations

FIN 200: Personal Finance Topic 19–Bonds Lawrence Schrenk, Instructor.>")

Assistant : Sandrine Charron 04 93 95 45 18.>")